You might also like

- Amazon and Walmart On Collision CourseDocument27 pagesAmazon and Walmart On Collision Coursekaushal gupta100% (1)

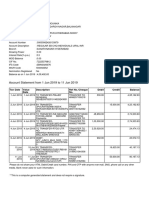

- Account Summary Payment Information: New Balance - $78.87Document6 pagesAccount Summary Payment Information: New Balance - $78.87AriadnaUrsachi100% (1)

- Case #12 - Growing A Global Forest - Ant Financial, Alipay, and Ant ForestDocument5 pagesCase #12 - Growing A Global Forest - Ant Financial, Alipay, and Ant ForestHaoyang Wei100% (1)

- Competing On Customer JourneysDocument10 pagesCompeting On Customer JourneysBhupesh NegiNo ratings yet

- Metro AgDocument48 pagesMetro AgSowjanya Kunareddy100% (2)

- Setup and Use The AP AR Netting & Intercompany Netting FeatureDocument13 pagesSetup and Use The AP AR Netting & Intercompany Netting FeatureSathya Moorthy0% (1)

- The Worlds Largest B2B MarketPlace-Alibaba - Com Case PDFDocument3 pagesThe Worlds Largest B2B MarketPlace-Alibaba - Com Case PDFsamar1976No ratings yet

- Amazon in Emerging MarketsDocument36 pagesAmazon in Emerging MarketsTwain Clyde FernandesNo ratings yet

- RBC Case StudyDocument20 pagesRBC Case StudyIshmeet SinghNo ratings yet

- Group Assignment - Alibaba Case StudyDocument10 pagesGroup Assignment - Alibaba Case StudyKleinNo ratings yet

- Case Study: Perfect Competition in Credit Card IndustryDocument1 pageCase Study: Perfect Competition in Credit Card IndustryMansi Dewan SrivastavaNo ratings yet

- Alibaba Brand AuditDocument19 pagesAlibaba Brand AuditTiviz Rooban100% (1)

- Inteli ChildDocument41 pagesInteli ChildSILANo ratings yet

- Taobao ReportDocument3 pagesTaobao ReportAmy Lin ChenNo ratings yet

- Boston Lyric Opera PrintDocument11 pagesBoston Lyric Opera PrintIvan GiovanniNo ratings yet

- CEMEX's Globalization Strategy and Industry AnalysisDocument10 pagesCEMEX's Globalization Strategy and Industry AnalysisPoonam GroverNo ratings yet

- A Case Study On International Expansion: When Amazon Went To ChinaDocument3 pagesA Case Study On International Expansion: When Amazon Went To ChinaitsarNo ratings yet

- Alibaba, A Trailblazing Chinese Internet Giant, Will Soon Go PublicDocument24 pagesAlibaba, A Trailblazing Chinese Internet Giant, Will Soon Go PublicHui XiuNo ratings yet

- Chap 12Document74 pagesChap 12NgơTiênSinhNo ratings yet

- E-Commerce IndustryDocument16 pagesE-Commerce IndustryTUSHARNo ratings yet

- Ant Financial Analysis and ObservationsDocument3 pagesAnt Financial Analysis and ObservationsGrimoire HeartsNo ratings yet

- Marketing ServicesDocument11 pagesMarketing ServicesKrishanth Ppt100% (1)

- Maru Betting Center Excel SheetDocument16 pagesMaru Betting Center Excel SheetRohan ShahNo ratings yet

- Detailed Writeup - Jaguar Land RoverDocument5 pagesDetailed Writeup - Jaguar Land RoverAkash GhoshNo ratings yet

- Case Study PDFDocument15 pagesCase Study PDFEr Ajay SharmaNo ratings yet

- John Mahoney Slides On China FintechDocument22 pagesJohn Mahoney Slides On China FintechAlex YisnNo ratings yet

- Fintech 100Document112 pagesFintech 100Meghana VyasNo ratings yet

- By Allen Zhang (Zhang Xiaolong) August 2012: Translated by Gustavo MadicoDocument136 pagesBy Allen Zhang (Zhang Xiaolong) August 2012: Translated by Gustavo MadicoAayush AgarwalNo ratings yet

- ZyngaDocument54 pagesZyngaJoyce KwokNo ratings yet

- Wal Mart CaseDocument159 pagesWal Mart CaseMohammadSaeed Aghajani100% (1)

- Learn) .: CRM Case Study EMBA 2015-2016 Soham Pradhan (Uemf15027)Document2 pagesLearn) .: CRM Case Study EMBA 2015-2016 Soham Pradhan (Uemf15027)ashishNo ratings yet

- LazadaDocument2 pagesLazadaWilliam LimNo ratings yet

- Aditya Birla SummaryDocument10 pagesAditya Birla SummaryChris NgoNo ratings yet

- Ali Case 1Document6 pagesAli Case 1eric100% (2)

- Wechat Marketing Strategy Brief ReportDocument21 pagesWechat Marketing Strategy Brief Reportsidgupta1230% (3)

- Shopkirana Pitch ExpansionDocument1 pageShopkirana Pitch ExpansionSusrut ChowdhuryNo ratings yet

- Kshitij Negi Semester 4 (Csit)Document10 pagesKshitij Negi Semester 4 (Csit)Kshitij NegiNo ratings yet

- Alibaba GroupDocument3 pagesAlibaba GroupLynn Nguyen100% (1)

- UnMe Jeans Social Media CaseDocument7 pagesUnMe Jeans Social Media CasejeremightNo ratings yet

- Case Study Analysis-Alibaba Competing in China & Beyond-21!6!10Document61 pagesCase Study Analysis-Alibaba Competing in China & Beyond-21!6!10Gaurav GuptaNo ratings yet

- Group Presents Mekanism's Viral Marketing StrategiesDocument15 pagesGroup Presents Mekanism's Viral Marketing StrategiesShaan RoyNo ratings yet

- Customer Relationship Management in Banking SectorDocument7 pagesCustomer Relationship Management in Banking SectorAmol WarseNo ratings yet

- The Failure of Amazon in Chinese Market and Prediction For Emerging MarketDocument11 pagesThe Failure of Amazon in Chinese Market and Prediction For Emerging MarketDo Thu Huong50% (2)

- CRM of TowngasDocument6 pagesCRM of TowngasBrijesh PandeyNo ratings yet

- Car InovationDocument3 pagesCar InovationClaudiu KLodNo ratings yet

- Credit Risk Analyst Interview Questions and Answers 1904Document13 pagesCredit Risk Analyst Interview Questions and Answers 1904MD ABDULLAH AL BAQUINo ratings yet

- Cyworld CRM Case1Document13 pagesCyworld CRM Case1Sareetha KanchanNo ratings yet

- Crown Cork and Seal CompanyDocument5 pagesCrown Cork and Seal CompanyShijin Mathew EipeNo ratings yet

- Case Study on Walmart's International Expansion and FailuresDocument17 pagesCase Study on Walmart's International Expansion and Failuresmanish14589No ratings yet

- Monitor Growth in Retail Services 02-24-11Document11 pagesMonitor Growth in Retail Services 02-24-11Svilen SabotinovNo ratings yet

- Apple in China Case Study AnalysisDocument8 pagesApple in China Case Study Analysisaeldra aeldraNo ratings yet

- Capital One Case Study On CRMDocument2 pagesCapital One Case Study On CRMashish100% (1)

- Wal-Mart Stores, IncDocument11 pagesWal-Mart Stores, IncMohit ManaktalaNo ratings yet

- BCG MatrixDocument3 pagesBCG MatrixHARSHIT360100% (2)

- Amelia Rogers at Tassani Communications: Group C5Document6 pagesAmelia Rogers at Tassani Communications: Group C5AmitabhNo ratings yet

- Matching DellDocument10 pagesMatching DellOng Wei KiongNo ratings yet

- Wal-Mart Case Analysis: Lessons for Future International ExpansionDocument8 pagesWal-Mart Case Analysis: Lessons for Future International ExpansionAtabur RahmanNo ratings yet

- Isme MM - Airtel Data AmbitionsDocument6 pagesIsme MM - Airtel Data AmbitionsAkhilesh desaiNo ratings yet

- Parentune CaseDocument13 pagesParentune CaseHimadri GuptaNo ratings yet

- Alibaba-Taobao Final 2Document26 pagesAlibaba-Taobao Final 2Rahul GuptaNo ratings yet

- RVU E-commerce Assignment on Alibaba's Business ModelDocument13 pagesRVU E-commerce Assignment on Alibaba's Business ModelAyele MitkuNo ratings yet

- Alibaba Case StudyDocument17 pagesAlibaba Case StudyDeshna KocharNo ratings yet

- Keywords: E-Commerce, Alibaba, Jack Ma, Cloud Computing, Artificial IntelligenceDocument9 pagesKeywords: E-Commerce, Alibaba, Jack Ma, Cloud Computing, Artificial IntelligenceHack MeNo ratings yet

- Financial Analysis: Sila Savaş 21058Document25 pagesFinancial Analysis: Sila Savaş 21058SILANo ratings yet

- Else Wares ProductsDocument39 pagesElse Wares ProductsMourad IsmailNo ratings yet

- Acme ConsultingDocument36 pagesAcme Consultingscorpion999No ratings yet

- Acme ConsultingDocument40 pagesAcme ConsultingSILANo ratings yet

- FayazDocument15 pagesFayazamiramir9086003904No ratings yet

- Activity Working Capital ManagementDocument2 pagesActivity Working Capital ManagementJoshua BrazalNo ratings yet

- Current Account: Bank Al-HabibDocument5 pagesCurrent Account: Bank Al-HabibMaazNo ratings yet

- InsuranceDocument12 pagesInsuranceRupa MohalanobishNo ratings yet

- Gard Rules 2023Document114 pagesGard Rules 2023TravisNo ratings yet

- Health System Model of VietnamDocument20 pagesHealth System Model of Vietnamsneha khuranaNo ratings yet

- American Express Credit Cart ActivitysDocument1 pageAmerican Express Credit Cart ActivitysAbhijit RathiNo ratings yet

- Investment Fund Types and CostsDocument15 pagesInvestment Fund Types and Costsraqi148No ratings yet

- Bank Account FormDocument1 pageBank Account FormAndo Matondang0% (1)

- Theories and Problem Solving AKDocument19 pagesTheories and Problem Solving AKJob CastonesNo ratings yet

- eLife Application Form for Home ServicesDocument3 pageseLife Application Form for Home Servicesashokj1984No ratings yet

- Mr. SHRIYANS DAFTARI bank account statement from 19 Dec 2022 to 20 Mar 2023Document12 pagesMr. SHRIYANS DAFTARI bank account statement from 19 Dec 2022 to 20 Mar 2023Shriyans DaftariNo ratings yet

- Chapter 1 - Basic Insurance Concepts and PrinciplesDocument9 pagesChapter 1 - Basic Insurance Concepts and Principlesale802No ratings yet

- Tally Spss PDFDocument42 pagesTally Spss PDFAkshay PoplyNo ratings yet

- 2022 Gr11 Mathematical Literacy WRKBK ENGDocument20 pages2022 Gr11 Mathematical Literacy WRKBK ENGmanganyeNo ratings yet

- Mgt101 Collection of Old PapersDocument86 pagesMgt101 Collection of Old Paperscs619finalproject.com100% (3)

- Kanban AbbDocument33 pagesKanban AbbHiralal SenapatiNo ratings yet

- E.ON BIll Dec-Feb 2023Document2 pagesE.ON BIll Dec-Feb 2023Eric CartmanNo ratings yet

- 1560239588575vK2jT68bxZZnz5kd PDFDocument1 page1560239588575vK2jT68bxZZnz5kd PDFChandu GoudNo ratings yet

- Invoice Template 5 WordDocument2 pagesInvoice Template 5 WordGuardian Network BangladeshNo ratings yet

- Debit Card Activation ProcessDocument2 pagesDebit Card Activation ProcessSajawal ManzoorNo ratings yet

- Ias 8 PDFDocument21 pagesIas 8 PDFJoedy Mae MangampoNo ratings yet

- StatementOfAccount 3092378518 Jul17 141113.csvDocument49 pagesStatementOfAccount 3092378518 Jul17 141113.csvOur educational ServiceNo ratings yet

- Сommonwealth AUDocument3 pagesСommonwealth AUbefix80880No ratings yet

- Air Cargo Freight ForwardersDocument7 pagesAir Cargo Freight ForwarderswilliamlyeNo ratings yet

- B. Cross-Functional: Bài 01: Introduction To Business ProcessesDocument81 pagesB. Cross-Functional: Bài 01: Introduction To Business ProcessesTrương Quốc PhongNo ratings yet

- D2.2 2300Mhz Role and Values in Network Performance and 4G 5G Spectrum AnalysisDocument20 pagesD2.2 2300Mhz Role and Values in Network Performance and 4G 5G Spectrum Analysishaipm1979No ratings yet

- TB12Document9 pagesTB12afrgod20No ratings yet