You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- P 8-12 Valix 2015 Volume 1Document4 pagesP 8-12 Valix 2015 Volume 1blahblahblueNo ratings yet

- 1-A Company Which Owns The Stock of Three Different BanksDocument5 pages1-A Company Which Owns The Stock of Three Different BanksalikahdNo ratings yet

- Accounting Lag PDFDocument27 pagesAccounting Lag PDFPallavi KapoorNo ratings yet

- 2017 3M Annual Report PDFDocument150 pages2017 3M Annual Report PDFPallavi KapoorNo ratings yet

- Pallavi Kapoor PDFDocument39 pagesPallavi Kapoor PDFPallavi KapoorNo ratings yet

- Pallavi Kapoor PDFDocument39 pagesPallavi Kapoor PDFPallavi KapoorNo ratings yet

- Apple Ebi 1t PDFDocument4 pagesApple Ebi 1t PDFPallavi KapoorNo ratings yet

- Apple 10k 2017Document124 pagesApple 10k 201776132No ratings yet

- GEDocument224 pagesGEDan ShepardNo ratings yet

- Financial Theory and Corporate PolicyDocument958 pagesFinancial Theory and Corporate PolicyDiego Ontaneda100% (1)

- 3m Ebit PDFDocument4 pages3m Ebit PDFPallavi KapoorNo ratings yet

- 30 S and P PDFDocument2 pages30 S and P PDFPallavi KapoorNo ratings yet

- Apple Ebit PDFDocument4 pagesApple Ebit PDFPallavi KapoorNo ratings yet

- AP - TestbankDocument22 pagesAP - TestbankRamon Jonathan SapalaranNo ratings yet

- Lisam Enterprises, Inc. vs. Banco de Oro Unibank, Inc. 670 SCRA 310, April 23, 2012 NatureDocument2 pagesLisam Enterprises, Inc. vs. Banco de Oro Unibank, Inc. 670 SCRA 310, April 23, 2012 NatureSong OngNo ratings yet

- Bank Failure: What Are The Bank Failures?Document5 pagesBank Failure: What Are The Bank Failures?Aaftab AhmadNo ratings yet

- Third PresentationDocument17 pagesThird PresentationalNo ratings yet

- K.L.E. Society's B.V. Bellad Law College, Belagavi Notice: ND RDDocument3 pagesK.L.E. Society's B.V. Bellad Law College, Belagavi Notice: ND RDRanjan BaradurNo ratings yet

- Internal Assignment Applicable For June 2017 Examination: Course: Commercial Banking System and Role of RBIDocument2 pagesInternal Assignment Applicable For June 2017 Examination: Course: Commercial Banking System and Role of RBInbala.iyerNo ratings yet

- Long-Term and Short-Term Financial Decisions Problems Week 7Document4 pagesLong-Term and Short-Term Financial Decisions Problems Week 7Ajeet YadavNo ratings yet

- Case 11-2 SolutionDocument2 pagesCase 11-2 SolutionArjun PratapNo ratings yet

- Atmqt3 4Document248 pagesAtmqt3 4Chu Minh Lan100% (1)

- Mariano Lerin Bookstore Chart of AccountsDocument15 pagesMariano Lerin Bookstore Chart of AccountsMaria Beatriz Aban Munda75% (4)

- Interest Swap Renewal RFRDocument47 pagesInterest Swap Renewal RFRJames Anderson Luna SilvaNo ratings yet

- Mortgage Bankers Association Document Custodian General Training Session For GSEsDocument209 pagesMortgage Bankers Association Document Custodian General Training Session For GSEsDeontosNo ratings yet

- Annual Report 2012 PDFDocument200 pagesAnnual Report 2012 PDFzafarNo ratings yet

- Central Bank V Morfe IncompleteDocument2 pagesCentral Bank V Morfe IncompletecinNo ratings yet

- Icpau Paper 15Document19 pagesIcpau Paper 15Innocent Won AberNo ratings yet

- Tai Tong Chuache v. Insurance CommissionDocument2 pagesTai Tong Chuache v. Insurance Commissionviva_33100% (1)

- Shareholders VsDocument2 pagesShareholders VsNidheesh TpNo ratings yet

- UBL Internship ReportDocument50 pagesUBL Internship ReportAmmarNo ratings yet

- Horacio Ortiz - Free Investors Efficient Markets and CrisisDocument13 pagesHoracio Ortiz - Free Investors Efficient Markets and CrisisjulibazzoNo ratings yet

- Notarized Documents As Public InstrumentsDocument15 pagesNotarized Documents As Public InstrumentsKarl Andrei CarandangNo ratings yet

- Contracts: General ProvisionsDocument94 pagesContracts: General Provisionsgilbert213No ratings yet

- Filing Small Claims Cases Under P100kDocument1 pageFiling Small Claims Cases Under P100kaL_2kNo ratings yet

- ReceivablesDocument58 pagesReceivablesHannah OrosNo ratings yet

- Nirc 1997Document160 pagesNirc 1997Charlie Magne G. SantiaguelNo ratings yet

- PDF of PGBPDocument7 pagesPDF of PGBPCHENDUCHAITHUNo ratings yet

- Real Estate Venture Capital Fund OpportunityDocument46 pagesReal Estate Venture Capital Fund OpportunityAnil MadhavNo ratings yet

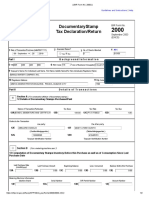

- Drafted BIR Form No. 2000Document2 pagesDrafted BIR Form No. 2000Kevin BesaNo ratings yet

- 01 23 19 Catalina IM Catalina Entitlement Fund PDFDocument52 pages01 23 19 Catalina IM Catalina Entitlement Fund PDFDavid MendezNo ratings yet