You might also like

- PartnersDocument13 pagesPartnersvaloruroNo ratings yet

- Advanced Accounting QN 1,7 & 8Document18 pagesAdvanced Accounting QN 1,7 & 8MAGOMU DAN DAVIDNo ratings yet

- Uk3 2009 Dec ADocument6 pagesUk3 2009 Dec AApple ChinNo ratings yet

- T3uk 2009 Jun ADocument8 pagesT3uk 2009 Jun AApple ChinNo ratings yet

- Uk3 2010 Jun ADocument7 pagesUk3 2010 Jun AApple ChinNo ratings yet

- Uk3 2011 Jun ADocument7 pagesUk3 2011 Jun AApple ChinNo ratings yet

- Madaraka Ltd. Statement of Comprehensive Income For The Year Ended 31 March 2020 KES'000' KES'000'Document17 pagesMadaraka Ltd. Statement of Comprehensive Income For The Year Ended 31 March 2020 KES'000' KES'000'Maryjoy KilonzoNo ratings yet

- IPFMPSFR - Solutions 3 2023 Final - AADocument31 pagesIPFMPSFR - Solutions 3 2023 Final - AASabNo ratings yet

- Acounting Revision QuestionsDocument10 pagesAcounting Revision QuestionsJoseph KabiruNo ratings yet

- IA3 Chapter 14 Problem 31Document3 pagesIA3 Chapter 14 Problem 31Bea TumulakNo ratings yet

- Intacc Cash Flow SolutionDocument3 pagesIntacc Cash Flow SolutionMila MercadoNo ratings yet

- Accounting Assigment 01 IndividualDocument2 pagesAccounting Assigment 01 IndividualOmari MaugaNo ratings yet

- Company Profit and LossDocument6 pagesCompany Profit and LossFazal Rehman Mandokhail50% (2)

- Felix Fernando - C13-Q2Document3 pagesFelix Fernando - C13-Q2Steve IdnNo ratings yet

- Jawaban Soal Latihan Ch.11Document2 pagesJawaban Soal Latihan Ch.11Wira DinataNo ratings yet

- 4.3.2.3 Elaborate - Preparing Adjusting Entries From Unadjusted and Adjusted Trial BalanceDocument3 pages4.3.2.3 Elaborate - Preparing Adjusting Entries From Unadjusted and Adjusted Trial BalanceMa Fe Tabasa100% (2)

- Book1 xlsx1Document4 pagesBook1 xlsx1Pian NasutionNo ratings yet

- 2009 S3 Ase2007Document15 pages2009 S3 Ase2007May CcmNo ratings yet

- Bba 122 Fai 11 AnswerDocument12 pagesBba 122 Fai 11 AnswerTomi Wayne Malenga100% (1)

- Tutorial 10 CH 5.3.6 SolutionDocument5 pagesTutorial 10 CH 5.3.6 SolutionenglishlessonsNo ratings yet

- QuizDocument4 pagesQuizRinconada Benori ReynalynNo ratings yet

- T4 - (Assets) - Qs and SolutionDocument22 pagesT4 - (Assets) - Qs and SolutionCalvin MaNo ratings yet

- Applied Auditing-Prelim FinalDocument3 pagesApplied Auditing-Prelim FinalDominic E. BoticarioNo ratings yet

- Review2 Ch01 ADocument1 pageReview2 Ch01 AMayy ElleNo ratings yet

- Answer On AccountingDocument6 pagesAnswer On AccountingShahid MahmudNo ratings yet

- Worksheet 4Document6 pagesWorksheet 4Sneha KumariNo ratings yet

- MT2 Ch02Document24 pagesMT2 Ch02api-3725162No ratings yet

- Asm ACCOUNTINGDocument16 pagesAsm ACCOUNTINGVũ Khánh HuyềnNo ratings yet

- Acctg. Equation Puring CompanyDocument8 pagesAcctg. Equation Puring CompanyAngelNo ratings yet

- Analysis of Financial StatementsDocument27 pagesAnalysis of Financial StatementsnickcrokNo ratings yet

- Comprehensive Audit of Balance Sheet and Income Statement AccountsDocument25 pagesComprehensive Audit of Balance Sheet and Income Statement AccountsLuigi Enderez Balucan100% (1)

- CH 2 Answers PDFDocument5 pagesCH 2 Answers PDFLian Blakely CousinNo ratings yet

- Mark Scheme (Results) January 2014Document19 pagesMark Scheme (Results) January 2014Fahrin NehaNo ratings yet

- Answers To Extra QuestionsDocument8 pagesAnswers To Extra QuestionsHashani KumarasingheNo ratings yet

- Solutionchapter 18 - Advacc Solutionchapter 18 - AdvaccDocument68 pagesSolutionchapter 18 - Advacc Solutionchapter 18 - AdvaccDvcLouisNo ratings yet

- Chapter 4 - Intermediate Accounting Volume 1Document8 pagesChapter 4 - Intermediate Accounting Volume 1Buenaventura, Elijah B.No ratings yet

- Genuime Company Required 1 Debit CreditDocument15 pagesGenuime Company Required 1 Debit CreditAnonnNo ratings yet

- Accountancy 12 - DS2 - Set - 1Document15 pagesAccountancy 12 - DS2 - Set - 1Deepa Saravana KumarNo ratings yet

- Sesi 11 & 12 SharedDocument28 pagesSesi 11 & 12 SharedDian Permata SariNo ratings yet

- Receivables Practice SolvingDocument15 pagesReceivables Practice SolvingddalgisznNo ratings yet

- Intermediate Accounting 1 Second Grading Examination Key AnswersDocument12 pagesIntermediate Accounting 1 Second Grading Examination Key AnswersAbegail Joy De GuzmanNo ratings yet

- Chapter 16: Additional Question Practice: Three of TheDocument18 pagesChapter 16: Additional Question Practice: Three of TheHankhnilNo ratings yet

- Ans June 2018 Far410Document8 pagesAns June 2018 Far4102022478048No ratings yet

- Adobe Scan Mar 16, 2023Document20 pagesAdobe Scan Mar 16, 2023Renalyn Ps MewagNo ratings yet

- NyayDocument3 pagesNyayJunneth Pearl HomocNo ratings yet

- Suggested Solutions June 2007Document12 pagesSuggested Solutions June 2007kalowekamoNo ratings yet

- June 2009 Fa4a1Document9 pagesJune 2009 Fa4a1ksakala58No ratings yet

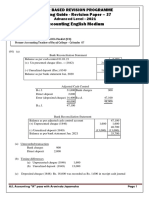

- Accounting English Medium: Paper Based Revision Programme Marking Guide - Revision Paper - 37Document6 pagesAccounting English Medium: Paper Based Revision Programme Marking Guide - Revision Paper - 37Malar SrirengarajahNo ratings yet

- Quiz For Week 7 Answer Key PR 1 and 4Document3 pagesQuiz For Week 7 Answer Key PR 1 and 4Joshuakenallen ricabuertaNo ratings yet

- Taxation - I: (Please Turn Over)Document3 pagesTaxation - I: (Please Turn Over)Laskar REAZ100% (1)

- 08chap 8 NP Farming Solutions 2020Document3 pages08chap 8 NP Farming Solutions 202044v8ct8cdyNo ratings yet

- MQP ANS 01 NDocument13 pagesMQP ANS 01 NAVINASH ROYNo ratings yet

- Irc Kit JJ20Document35 pagesIrc Kit JJ20Amir ArifNo ratings yet

- Sol. Man. - Chapter 4 - Accounts Receivable - Ia Part 1aDocument19 pagesSol. Man. - Chapter 4 - Accounts Receivable - Ia Part 1aMiguel AmihanNo ratings yet

- Partnership Accounts:: Assets Revaluation, Dissolution & Conversion To Limited CompanyDocument47 pagesPartnership Accounts:: Assets Revaluation, Dissolution & Conversion To Limited CompanyWen Xin GanNo ratings yet

- F2 Past Paper - Ans12-2006Document8 pagesF2 Past Paper - Ans12-2006ArsalanACCANo ratings yet

- Review of The Accounting Process Problems 2-1. (Tiger Company)Document5 pagesReview of The Accounting Process Problems 2-1. (Tiger Company)Pauline Kisha CastroNo ratings yet

- Cash Flow Statement ProblemDocument2 pagesCash Flow Statement Problemapi-3842194100% (2)

- AC191 Autumn 2011 FINALDocument9 pagesAC191 Autumn 2011 FINALgerlaniamelgacoNo ratings yet

- The Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeFrom EverandThe Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeNo ratings yet

- Where Will Your Strategy Guru Lead YouDocument2 pagesWhere Will Your Strategy Guru Lead YouShailendra KelaniNo ratings yet

- Toy Stories - Association For Psychological Science - APSDocument5 pagesToy Stories - Association For Psychological Science - APSShailendra KelaniNo ratings yet

- Prework Leading Change (Gup 2)Document2 pagesPrework Leading Change (Gup 2)Shailendra KelaniNo ratings yet

- Stores ManagementDocument49 pagesStores ManagementsanshekhNo ratings yet

- BestPractices#6 Asset Management Feb2019Document4 pagesBestPractices#6 Asset Management Feb2019Shailendra KelaniNo ratings yet

- 20 Sales Management Strategies To Lead Your Sales Team To SuccessDocument17 pages20 Sales Management Strategies To Lead Your Sales Team To SuccessShailendra KelaniNo ratings yet

- No33 Maximizingbenefitsofself-Assess GoodDocument8 pagesNo33 Maximizingbenefitsofself-Assess GoodShailendra KelaniNo ratings yet

- 40 Strategic Questions To Ask To Evaluate Company DirectionDocument7 pages40 Strategic Questions To Ask To Evaluate Company DirectionShailendra Kelani100% (1)

- Life LessonsDocument4 pagesLife LessonsShailendra KelaniNo ratings yet

- The Great TransformerDocument2 pagesThe Great TransformerShailendra KelaniNo ratings yet

- Annexures Entreprenure QuestionnaireDocument7 pagesAnnexures Entreprenure QuestionnaireShailendra KelaniNo ratings yet

- Blueprint To A BillionDocument20 pagesBlueprint To A Billionolumakin100% (1)

- Life/Work Lessons: These Behaviors Can Improve Your Performance and Value To Your OrganizationDocument1 pageLife/Work Lessons: These Behaviors Can Improve Your Performance and Value To Your OrganizationShailendra KelaniNo ratings yet

- 9505-The Instant Sales ProDocument1 page9505-The Instant Sales ProShailendra KelaniNo ratings yet

- IBM Transactional Sales MatrixDocument24 pagesIBM Transactional Sales MatrixaviNo ratings yet

- Entrepreneurship and Entrepreneurial Motivation: Nadire YimamuDocument45 pagesEntrepreneurship and Entrepreneurial Motivation: Nadire YimamuShailendra KelaniNo ratings yet

- Organizational Assessment: A Review of Experience: Universalia Occasional Paper No. 31, October 1998Document16 pagesOrganizational Assessment: A Review of Experience: Universalia Occasional Paper No. 31, October 1998Shailendra KelaniNo ratings yet

- Syllabus: The Landmark ForumDocument4 pagesSyllabus: The Landmark Forumcessna5538c100% (1)

- Super Productivity WorksheetDocument2 pagesSuper Productivity WorksheetShailendra Kelani0% (1)

- Brief Summary of The Coaching Habit PDFDocument6 pagesBrief Summary of The Coaching Habit PDFserkan kayaNo ratings yet

- ManageGrowth PDFDocument98 pagesManageGrowth PDFShailendra KelaniNo ratings yet

- High-Impact Leadership Transitions PDFDocument16 pagesHigh-Impact Leadership Transitions PDFShailendra KelaniNo ratings yet

- Robin Sharma Weekly Design SystemDocument1 pageRobin Sharma Weekly Design Systemgmsbhat100% (4)

- Landmark Forum Syl Lab UsDocument1 pageLandmark Forum Syl Lab UsShailendra KelaniNo ratings yet

- Principles of Management NotesDocument16 pagesPrinciples of Management NotesShailendra KelaniNo ratings yet

- Principles of Management LECTURE NotesDocument32 pagesPrinciples of Management LECTURE NotesPrasant BistNo ratings yet

- Process Understanding & Improvement: Excellence QualityDocument9 pagesProcess Understanding & Improvement: Excellence Qualityvenky020377No ratings yet

- Staying Small SMEDocument9 pagesStaying Small SMEShailendra KelaniNo ratings yet

- Business Growth Through People Growth 25thapr00 - tcm114-136023Document8 pagesBusiness Growth Through People Growth 25thapr00 - tcm114-136023Vishnu PrasadNo ratings yet

- Inventory Part 1Document24 pagesInventory Part 1Sukma Faradila Putri PangestuNo ratings yet

- Acct 5930 Quiz 1 Question 1Document26 pagesAcct 5930 Quiz 1 Question 1Mauhammad NajamNo ratings yet

- IAS 12 Income TaxesDocument54 pagesIAS 12 Income Taxessimiong100% (1)

- Summary Cash Flow - Investing ActivitiesDocument9 pagesSummary Cash Flow - Investing ActivitiesLesego BaneleNo ratings yet

- 12 AccountancyDocument48 pages12 Accountancyraghu monnappaNo ratings yet

- 1.-Bookkeeping (1) LessonDocument25 pages1.-Bookkeeping (1) LessonRodel Carreon Candelaria100% (1)

- Bal Bharati Mid Term XIi - 2023-24Document9 pagesBal Bharati Mid Term XIi - 2023-24Thakur ShikharNo ratings yet

- Accounting Paper 1Document24 pagesAccounting Paper 1snowFlakes ANo ratings yet

- Makalah BOP - Kelompok 2 - Monetary EconomicsDocument15 pagesMakalah BOP - Kelompok 2 - Monetary EconomicsMochammad YusufNo ratings yet

- Introduction To Book Keeping and AccountancyDocument27 pagesIntroduction To Book Keeping and AccountancyJanhvi ThakkarNo ratings yet

- Preview Principles of Accounts For Caribbean Examinations TextbooksDocument18 pagesPreview Principles of Accounts For Caribbean Examinations TextbooksOkari Banton50% (4)

- MGT401 Short Notes Lec 1 - 45Document33 pagesMGT401 Short Notes Lec 1 - 45HRrehmanNo ratings yet

- AmZpMjcBQkemaTI3AaJHwA Final-exam-Accounting SolutionsDocument3 pagesAmZpMjcBQkemaTI3AaJHwA Final-exam-Accounting SolutionsPRANAV BHARARA0% (2)

- Financial Accounting: Adjusting The AccountsDocument33 pagesFinancial Accounting: Adjusting The AccountsGiang PhungNo ratings yet

- Class - 4 TransactionDocument8 pagesClass - 4 TransactionAkshay SinghNo ratings yet

- Week 3 Adjusting EntriesDocument17 pagesWeek 3 Adjusting EntriesShiellai Mae PolintangNo ratings yet

- Accounting Edexcel Jan 2017Document20 pagesAccounting Edexcel Jan 2017Simra RiyazNo ratings yet

- Job Order Cost Accounting: Study ObjectivesDocument39 pagesJob Order Cost Accounting: Study ObjectivesNanik DeniaNo ratings yet

- Activity 6Document12 pagesActivity 6danica gomezNo ratings yet

- Chapter 4 Completing The Accounting Cycle PDFDocument20 pagesChapter 4 Completing The Accounting Cycle PDFJed Riel BalatanNo ratings yet

- Company AccountsDocument26 pagesCompany AccountsSaleh AbubakarNo ratings yet

- Finanical Statments RajDocument30 pagesFinanical Statments RajAsħîŞĥLøÝåNo ratings yet

- Assignment BBAS 4103Document11 pagesAssignment BBAS 4103Nadiah Atiqah Nor HishamudinNo ratings yet

- Chapter9 10 TestbankkDocument43 pagesChapter9 10 Testbankk2Ng0100% (10)

- About The Business 1.1 Business Profile Positif CorporationDocument7 pagesAbout The Business 1.1 Business Profile Positif CorporationLinh DalanginNo ratings yet

- P2 Reviewer PDFDocument64 pagesP2 Reviewer PDFBeef TestosteroneNo ratings yet

- Chapter 16Document27 pagesChapter 16Red Christian Palustre100% (1)

- Keac 103Document53 pagesKeac 103Techie MeasureNo ratings yet

- Annex K-Bank Reconciliation Statement PDFDocument12 pagesAnnex K-Bank Reconciliation Statement PDFRg Abulkhayr Lawi GuilingNo ratings yet

- Statement PDFDocument4 pagesStatement PDFSanta Dela Cruz NaluzNo ratings yet