You might also like

- External Audit ScopeDocument2 pagesExternal Audit ScopeBennice 8No ratings yet

- Spotlight: Audit Committee ResourceDocument5 pagesSpotlight: Audit Committee ResourceAbdelmadjid djibrineNo ratings yet

- Audit planning essentialsDocument2 pagesAudit planning essentialsIsabell CastroNo ratings yet

- Audit Planning and Materiality in CIS EnvironmentsDocument4 pagesAudit Planning and Materiality in CIS EnvironmentsLady BirdNo ratings yet

- Module 1 AUDIT PLANNINGDocument3 pagesModule 1 AUDIT PLANNINGLady BirdNo ratings yet

- Audit Planning: Auditor's Main ObjectiveDocument7 pagesAudit Planning: Auditor's Main Objectivemarie aniceteNo ratings yet

- Assessing External Audit Effectiveness: Audit Committee Oversight EssentialsDocument2 pagesAssessing External Audit Effectiveness: Audit Committee Oversight EssentialsWilson FernandoNo ratings yet

- Auditing 1: Internal AuditDocument45 pagesAuditing 1: Internal AuditChrizt ChrisNo ratings yet

- H001 - Intro To Internal AuditingDocument12 pagesH001 - Intro To Internal AuditingKevin James Sedurifa OledanNo ratings yet

- 2 Aci Assessing System Internal Control Fs Uk v4 LR PDFDocument2 pages2 Aci Assessing System Internal Control Fs Uk v4 LR PDFFira NoverinaNo ratings yet

- Assessing External Audit EffectivenessDocument8 pagesAssessing External Audit EffectivenessANANDNo ratings yet

- Lecture Notes: Auditing Theory AT.0106-Understanding The Entity and Its Environment MAY 2020Document7 pagesLecture Notes: Auditing Theory AT.0106-Understanding The Entity and Its Environment MAY 2020MaeNo ratings yet

- Assessing System of Internal ControlsDocument2 pagesAssessing System of Internal ControlsastiningrumdamayantiNo ratings yet

- GTAG3 Audit KontinyuDocument37 pagesGTAG3 Audit KontinyujonisupriadiNo ratings yet

- Part 2 NotesDocument21 pagesPart 2 NotesFazlihaq DurraniNo ratings yet

- Integrated Auditing: - Practice GuideDocument16 pagesIntegrated Auditing: - Practice GuideMaria Jeannie Curay100% (1)

- Neglected Audit AreasDocument3 pagesNeglected Audit AreasMarcos WilkerNo ratings yet

- Template Presentation - Entrance and Exit MeetingsDocument48 pagesTemplate Presentation - Entrance and Exit MeetingsRheneir MoraNo ratings yet

- Harnessing The Full Potential of Internal Audit: To Protect and EnhanceDocument12 pagesHarnessing The Full Potential of Internal Audit: To Protect and EnhanceAlya Khaira NazhifaNo ratings yet

- GTAG 3 Continuous Auditing Implications For Assurance Monitoring and Risk AssessmentDocument41 pagesGTAG 3 Continuous Auditing Implications For Assurance Monitoring and Risk AssessmentGurcan KarayelNo ratings yet

- 74937bos60526-Cp4 UnlockedDocument72 pages74937bos60526-Cp4 Unlockedhrudaya boysNo ratings yet

- Internal Audit: An Effective Tool for Cost ControlDocument16 pagesInternal Audit: An Effective Tool for Cost ControlNMA NMANo ratings yet

- GTAG 3 Continuous Auditing 2nd EditionDocument30 pagesGTAG 3 Continuous Auditing 2nd EditionDede AndriNo ratings yet

- This Study Resource Was: (Select All That Apply.)Document6 pagesThis Study Resource Was: (Select All That Apply.)Jeap JeavNo ratings yet

- Lesson 5 - Audit PlanningDocument4 pagesLesson 5 - Audit PlanningAllaina Uy BerbanoNo ratings yet

- At.3208-Understanding The Entity and Its EnvironmentDocument6 pagesAt.3208-Understanding The Entity and Its EnvironmentDenny June CraususNo ratings yet

- Internal Audit SolutionbriefDocument13 pagesInternal Audit SolutionbriefahmadNo ratings yet

- How To Set Up A New Internal Audit Activity: Chartered Institute of Internal AuditorsDocument7 pagesHow To Set Up A New Internal Audit Activity: Chartered Institute of Internal AuditorsDENo ratings yet

- Chapter 5 AuditDocument62 pagesChapter 5 Auditmaryumarshad2No ratings yet

- Internal AuditDocument7 pagesInternal AuditJundel AbieraNo ratings yet

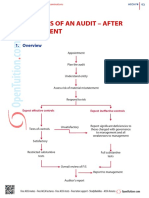

- The Stages of An Audit - After Appointment: 1. OverviewDocument6 pagesThe Stages of An Audit - After Appointment: 1. OverviewArina ANo ratings yet

- Engagement Value Enabler 3: Audit Objective: Step 1: Why To Audit?Document10 pagesEngagement Value Enabler 3: Audit Objective: Step 1: Why To Audit?Jonnabel SulascoNo ratings yet

- 74936bos60526-Cp3 UnlockedDocument70 pages74936bos60526-Cp3 Unlockedhrudaya boysNo ratings yet

- Aci HandbookDocument270 pagesAci Handbookmuhammad irsyad khresna ajiNo ratings yet

- Understand entity risk assessmentDocument12 pagesUnderstand entity risk assessmentMarjorie BernasNo ratings yet

- F - Practice Guide - Formulating Audit OpinionsDocument20 pagesF - Practice Guide - Formulating Audit OpinionsimianmoralesNo ratings yet

- Risk-Based Process AuditsDocument12 pagesRisk-Based Process AuditsDizzyDudeNo ratings yet

- Final OAP Practice Guide Dec 2011Document29 pagesFinal OAP Practice Guide Dec 2011Pramod AthiyarathuNo ratings yet

- Chapter+2+ +Audit+Planning+and+Internal+Controls+Considerations+ +part+1Document16 pagesChapter+2+ +Audit+Planning+and+Internal+Controls+Considerations+ +part+1Dan MorettoNo ratings yet

- Function of Audit PlannningDocument4 pagesFunction of Audit PlannningGelly Dominique GuijoNo ratings yet

- Annual Internal Audit Coverage PlansDocument8 pagesAnnual Internal Audit Coverage PlansAartikaNo ratings yet

- Audit Liquid Measurement (Class 7050)Document4 pagesAudit Liquid Measurement (Class 7050)yoyokpurwantoNo ratings yet

- ISA 315 Understanding Internal ControlsDocument3 pagesISA 315 Understanding Internal ControlsDanica Christele AlfaroNo ratings yet

- Lecture Notes: Auditing Theory AT.0107-Understanding The Entity's Internal Control MAY 2020Document6 pagesLecture Notes: Auditing Theory AT.0107-Understanding The Entity's Internal Control MAY 2020MaeNo ratings yet

- 5 PlanningDocument20 pages5 PlanningSayraj Siddiki AnikNo ratings yet

- Audit Planning StepsDocument42 pagesAudit Planning StepsYismawNo ratings yet

- Ey Insurance Maintaining Internal Controls and Trust While Remote Working During Covid 19Document11 pagesEy Insurance Maintaining Internal Controls and Trust While Remote Working During Covid 19Arun RajanNo ratings yet

- ISO 9001 Auditing Practices Group Guidance On: Internal AuditsDocument4 pagesISO 9001 Auditing Practices Group Guidance On: Internal AuditsGuadalupe Aniceto SanchezNo ratings yet

- Assessing System of Internal ControlsDocument2 pagesAssessing System of Internal ControlsMary MwansaNo ratings yet

- Internal Audit Roles IIDocument13 pagesInternal Audit Roles IIAsif KhanNo ratings yet

- Auditing Full Version Sir Jaypee Tinipid Version1Document17 pagesAuditing Full Version Sir Jaypee Tinipid Version1Lovely Rose ArpiaNo ratings yet

- SOX-Internal Audit Manual FY2012Document19 pagesSOX-Internal Audit Manual FY2012Diana MarcelaNo ratings yet

- 18AKJ - Sri Widya Ningsih-Audit InternalDocument5 pages18AKJ - Sri Widya Ningsih-Audit InternalTantiNo ratings yet

- Control Testing Vs Substantive by CPA MADHAV BHANDARIDocument59 pagesControl Testing Vs Substantive by CPA MADHAV BHANDARIMacmilan Trevor JamuNo ratings yet

- Chapter 3: Process of Assurance: Planning The AssignmentDocument12 pagesChapter 3: Process of Assurance: Planning The AssignmentShahid MahmudNo ratings yet

- SOX and Financial Audit GuideDocument47 pagesSOX and Financial Audit GuideArianne May Amosin100% (1)

- MODULE 1 2 ExercisesDocument8 pagesMODULE 1 2 ExercisesAMNo ratings yet

- Internal Audit RoleDocument12 pagesInternal Audit RoleBobbyD.ResjaNo ratings yet

- H004 - Risk-Based Audit PlanDocument11 pagesH004 - Risk-Based Audit PlanKevin James Sedurifa OledanNo ratings yet

- Match resume to job descriptionDocument2 pagesMatch resume to job descriptionSelva Bavani SelwaduraiNo ratings yet

- 5 Why Root Cause Corrective ActionsDocument13 pages5 Why Root Cause Corrective Actionsalex1123No ratings yet

- FCFE TemplateDocument9 pagesFCFE TemplateSelva Bavani SelwaduraiNo ratings yet

- Specimen Internal Audit Report: Appendix 15Document5 pagesSpecimen Internal Audit Report: Appendix 15Selva Bavani SelwaduraiNo ratings yet

- Monroeconsulting Com PDFDocument1 pageMonroeconsulting Com PDFSelva Bavani SelwaduraiNo ratings yet

- ACCA Study Guide and Exam TipsDocument8 pagesACCA Study Guide and Exam TipsSelva Bavani SelwaduraiNo ratings yet

- Internal Audit MapDocument1 pageInternal Audit Maptauqeer25No ratings yet

- I Recommended Audit Fees in MalaysiaDocument2 pagesI Recommended Audit Fees in MalaysiaSelva Bavani SelwaduraiNo ratings yet

- Monroeconsulting Com PDFDocument1 pageMonroeconsulting Com PDFSelva Bavani SelwaduraiNo ratings yet

- Internal Audit Executive: Job DescriptionDocument2 pagesInternal Audit Executive: Job DescriptionSelva Bavani SelwaduraiNo ratings yet

- Acknowledgement - TaxDocument1 pageAcknowledgement - TaxSelva Bavani SelwaduraiNo ratings yet

- 2016 Calendar: January 2016Document12 pages2016 Calendar: January 2016chikayNo ratings yet

- Working Paper TemplatesDocument9 pagesWorking Paper TemplatesTroisNo ratings yet

- Itle Rocess: UrposeDocument4 pagesItle Rocess: UrposeSelva Bavani SelwaduraiNo ratings yet

- Internal Audit Executive: Job DescriptionDocument2 pagesInternal Audit Executive: Job DescriptionSelva Bavani SelwaduraiNo ratings yet

- Audit Working Papers PDFDocument49 pagesAudit Working Papers PDFSelva Bavani SelwaduraiNo ratings yet

- Delivering Internal Audit FindingsDocument9 pagesDelivering Internal Audit FindingsSelva Bavani SelwaduraiNo ratings yet

- Planning Phase - Guidelines For Observation of Physical InventoriesDocument5 pagesPlanning Phase - Guidelines For Observation of Physical InventoriesSelva Bavani SelwaduraiNo ratings yet

- Portfolio ExampleDocument34 pagesPortfolio ExampleAlin TuvicNo ratings yet

- How to Hire a Lawyer for Your Legal NeedsDocument7 pagesHow to Hire a Lawyer for Your Legal NeedsNivash Dhespal SinghNo ratings yet

- 3 Aci External Audit Scope Fs Uk v12 LRDocument2 pages3 Aci External Audit Scope Fs Uk v12 LRSelva Bavani SelwaduraiNo ratings yet

- Chapter CRM 6 15Document3 pagesChapter CRM 6 15Selva Bavani SelwaduraiNo ratings yet

- Russell Global Sectors Methodology OverviewDocument5 pagesRussell Global Sectors Methodology OverviewSelva Bavani Selwadurai0% (1)

- 6 Components of HealthDocument10 pages6 Components of HealthSelva Bavani SelwaduraiNo ratings yet

- (Labour Law-1) - 1Document4 pages(Labour Law-1) - 1Arghyadeep NagNo ratings yet

- Gear Box ReportDocument39 pagesGear Box ReportNisar HussainNo ratings yet

- Trimble M3 UserGuide 100A English PDFDocument168 pagesTrimble M3 UserGuide 100A English PDFVladan SpasenovicNo ratings yet

- TheMinitestCookbook SampleDocument28 pagesTheMinitestCookbook SampleeveevansNo ratings yet

- AWS CWI Training Program PDFDocument22 pagesAWS CWI Training Program PDFDjamelNo ratings yet

- Case Study Biomaterials Selection For A Joint ReplacementDocument8 pagesCase Study Biomaterials Selection For A Joint ReplacementBjarne Van haegenbergNo ratings yet

- Case of Harvey V FaceyDocument2 pagesCase of Harvey V Faceyveera89% (18)

- ATA55 CatalogueDocument5 pagesATA55 CatalogueHikmat KtkNo ratings yet

- CTA RulingDocument12 pagesCTA RulingGhia TalidongNo ratings yet

- Direct Cuspal Coverage Posterior Resin Composite RestorationsDocument8 pagesDirect Cuspal Coverage Posterior Resin Composite Restorationsdentace1No ratings yet

- GEMS Calender 2019-20Document2 pagesGEMS Calender 2019-20Rushiraj SinhNo ratings yet

- Electricity Markets and Renewable GenerationDocument326 pagesElectricity Markets and Renewable GenerationElimar RojasNo ratings yet

- Interview Questions For PBDocument3 pagesInterview Questions For PBskrtripathiNo ratings yet

- Philippine Department of Education lesson on productivity toolsDocument5 pagesPhilippine Department of Education lesson on productivity toolsKarl Nonog100% (1)

- FINANCIAL RATIOS AND CALCULATIONSDocument13 pagesFINANCIAL RATIOS AND CALCULATIONS1 KohNo ratings yet

- MF AXIOM Cyber Brief PDFDocument2 pagesMF AXIOM Cyber Brief PDFluis demetrio martinez ruizNo ratings yet

- Philippine Environmental Laws SummaryDocument54 pagesPhilippine Environmental Laws SummaryHayel Rabaja50% (2)

- Tcs Employment Application Form: Basic DetailsDocument6 pagesTcs Employment Application Form: Basic DetailsRakesh Reddy GeetlaNo ratings yet

- NL Back Pressure Valve Brochure 032613Document9 pagesNL Back Pressure Valve Brochure 032613EquilibarNo ratings yet

- Chapter 03 - Coding in The SAPScript EditorDocument25 pagesChapter 03 - Coding in The SAPScript EditorLukas CelyNo ratings yet

- Openlectures Publicity PackDocument20 pagesOpenlectures Publicity PacksuhangdageekNo ratings yet

- Comparison of ROBOT and MIDAS GENDocument2 pagesComparison of ROBOT and MIDAS GENAshish LoyaNo ratings yet

- TL594 Pulse-Width-Modulation Control Circuit: 1 Features 3 DescriptionDocument33 pagesTL594 Pulse-Width-Modulation Control Circuit: 1 Features 3 Descriptionاحمد زغارىNo ratings yet

- CSC:361-Software Engineering: Semester: Fall2020Document39 pagesCSC:361-Software Engineering: Semester: Fall2020hamsfayyazNo ratings yet

- International Trade Finance - Nov 2009Document8 pagesInternational Trade Finance - Nov 2009Basilio MaliwangaNo ratings yet

- Inductance Meter AdapterDocument3 pagesInductance Meter AdapterioanNo ratings yet

- LogDocument20 pagesLogAbang SkyNo ratings yet

- Verification of Hook Element in Midas GenDocument3 pagesVerification of Hook Element in Midas GenSASHIN ServiSoftNo ratings yet

- How to Clear a TableDocument20 pagesHow to Clear a TableRochell CapellanNo ratings yet

- Tools and Techniques of Cost ReductionDocument27 pagesTools and Techniques of Cost Reductionপ্রিয়াঙ্কুর ধর100% (2)