You might also like

- Acknowledgement 4 5Document5 pagesAcknowledgement 4 5IT ANo ratings yet

- Unlocking The Secrets Of Bitcoin And Cryptocurrency: Crypto Currency Made EasyFrom EverandUnlocking The Secrets Of Bitcoin And Cryptocurrency: Crypto Currency Made EasyRating: 1 out of 5 stars1/5 (1)

- Bitcoinpreneur- A Beginners Guide to Bitcoin, and Everything You Need to Know to Start InvestingFrom EverandBitcoinpreneur- A Beginners Guide to Bitcoin, and Everything You Need to Know to Start InvestingNo ratings yet

- Methods to Overcome the Financial and Money Transfer Blockade against Palestine and any Country Suffering from Financial BlockadeFrom EverandMethods to Overcome the Financial and Money Transfer Blockade against Palestine and any Country Suffering from Financial BlockadeNo ratings yet

- Bitcoin Cash Versus Bitcoin: the Battle of the Cryptocurrencies: Crypto for beginners, #2From EverandBitcoin Cash Versus Bitcoin: the Battle of the Cryptocurrencies: Crypto for beginners, #2No ratings yet

- Cryptocurrency and the Incompatibility with the Current Banking System: CRYPTOCURRENCYFrom EverandCryptocurrency and the Incompatibility with the Current Banking System: CRYPTOCURRENCYNo ratings yet

- SEC Whistleblower Submission No. TCR1458580189411 - Mar-21-2016Document39 pagesSEC Whistleblower Submission No. TCR1458580189411 - Mar-21-2016Neil GillespieNo ratings yet

- Do Consumers Really Trust Cryptocurrencies?: Denni Arli Patrick Van EschDocument17 pagesDo Consumers Really Trust Cryptocurrencies?: Denni Arli Patrick Van EschsevaletotoNo ratings yet

- Cryptocurrencies: International Regulation AND Uniformization of PracticesDocument18 pagesCryptocurrencies: International Regulation AND Uniformization of PracticesRizalien Jane BongcayaoNo ratings yet

- Private Vs - Public CoDocument3 pagesPrivate Vs - Public CoKishor SatputeNo ratings yet

- ContractsDocument15 pagesContractsNnNo ratings yet

- Stable Money: What we can learn from Bitcoin, Libra, and Co.From EverandStable Money: What we can learn from Bitcoin, Libra, and Co.No ratings yet

- Money LaunderingDocument1 pageMoney LaunderingmarkformacNo ratings yet

- BBVA Continental-Preliminary Offering Circular PDFDocument362 pagesBBVA Continental-Preliminary Offering Circular PDFfanatico1982No ratings yet

- Federal Reserve On FintechDocument36 pagesFederal Reserve On FintechCrowdfundInsider100% (1)

- Cross Border Money TransferDocument8 pagesCross Border Money Transferintix intNo ratings yet

- Ramon Rosales Dominguez: Transaction Code: RRD4.500.000BOXESREDIQD03022022Document26 pagesRamon Rosales Dominguez: Transaction Code: RRD4.500.000BOXESREDIQD03022022Nivetha NaguNo ratings yet

- Credit Derivatives and Structured Credit: A Guide for InvestorsFrom EverandCredit Derivatives and Structured Credit: A Guide for InvestorsNo ratings yet

- RTGSDocument14 pagesRTGSHarshUpadhyayNo ratings yet

- Crypto AgreementDocument26 pagesCrypto AgreementAamir HuzaifaNo ratings yet

- International Banking SystemDocument24 pagesInternational Banking SystemSukumar Nandi100% (9)

- CryptoCurrency Portfolio ValuationDocument1 pageCryptoCurrency Portfolio ValuationRoha JavidNo ratings yet

- Money Laundering and The Bank Secrecy LawDocument3 pagesMoney Laundering and The Bank Secrecy Lawnut_crackreNo ratings yet

- IsinoDocument187 pagesIsinojohn100% (1)

- Open Letter To FinCEN's Proposed Amendment of The BSADocument31 pagesOpen Letter To FinCEN's Proposed Amendment of The BSASamIamNo ratings yet

- FedGlobal ACH PaymentsDocument2 pagesFedGlobal ACH PaymentscrazytrainNo ratings yet

- ReportDocument74 pagesReportar15t0tleNo ratings yet

- Cryptocurrency - A New Investment OpportunityDocument26 pagesCryptocurrency - A New Investment OpportunityMohd. Anisul IslamNo ratings yet

- The Administration of The Estate of The Late Ann Birkin Up To Issue of The Grant of ProbateDocument8 pagesThe Administration of The Estate of The Late Ann Birkin Up To Issue of The Grant of Probatef9zvxkvw5mNo ratings yet

- Bitcoin Legendary: The Truth About The Most Revolutionary Asset Of Our LifetimeFrom EverandBitcoin Legendary: The Truth About The Most Revolutionary Asset Of Our LifetimeNo ratings yet

- Coinmint vs. Ashton Soniat Fraud CaseDocument8 pagesCoinmint vs. Ashton Soniat Fraud CaseDon HewlettNo ratings yet

- TestimonyDocument27 pagesTestimonyMichaelPatrickMcSweeneyNo ratings yet

- Bitcoin CryptocurrencyDocument1 pageBitcoin CryptocurrencyNikki KumariNo ratings yet

- ASEAN+3 Multi-Currency Bond Issuance Framework: Implementation Guidelines for the PhilippinesFrom EverandASEAN+3 Multi-Currency Bond Issuance Framework: Implementation Guidelines for the PhilippinesNo ratings yet

- UNIT 1 E Payment SystemDocument76 pagesUNIT 1 E Payment SystemRahul DesuNo ratings yet

- Money TransferDocument4 pagesMoney TransferpasaksNo ratings yet

- VIBHS - Funds Withdrawal RequestDocument3 pagesVIBHS - Funds Withdrawal RequestAkhil HussainNo ratings yet

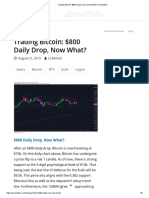

- Trading Bitcoin - $800 Daily Drop, Now What - InvestituteDocument6 pagesTrading Bitcoin - $800 Daily Drop, Now What - InvestituteNorman M.No ratings yet

- Bitcoin: Beginner's Simplified Guide to Make Money with BitcoinFrom EverandBitcoin: Beginner's Simplified Guide to Make Money with BitcoinNo ratings yet

- PEMI - Investment Application Form (IAF)Document1 pagePEMI - Investment Application Form (IAF)junmiguelNo ratings yet

- Wire Deposit Form PDFDocument1 pageWire Deposit Form PDFphuiyeeNo ratings yet

- The Cryptocurrency WalletDocument3 pagesThe Cryptocurrency WalletElenaNo ratings yet

- Standard Chartered BankDocument56 pagesStandard Chartered BankTarekNo ratings yet

- Reservation and Acquisition AgreementDocument7 pagesReservation and Acquisition AgreementLjutko MeisterNo ratings yet

- Bitcoin Explained: Beginner’s Guide To Understanding BitcoinFrom EverandBitcoin Explained: Beginner’s Guide To Understanding BitcoinNo ratings yet

- Duke Energy PremierNotes ProspectusDocument37 pagesDuke Energy PremierNotes ProspectusshoppingonlyNo ratings yet

- Highlight Issue BitcoinDocument20 pagesHighlight Issue BitcoinNur IkaNo ratings yet

- Cryptocurrencies and BlockchainDocument26 pagesCryptocurrencies and BlockchainAlex LindgrenNo ratings yet

- Bitcoin Gold Mining and Cryptocurrency Blockchain, Trading, and Investing Mastery GuideFrom EverandBitcoin Gold Mining and Cryptocurrency Blockchain, Trading, and Investing Mastery GuideNo ratings yet

- Payment System 200909 enDocument371 pagesPayment System 200909 enMichiel BeerensNo ratings yet

- Source of Funds ComplianceDocument2 pagesSource of Funds ComplianceAnonymous MddQJywVNo ratings yet

- Fatf PDFDocument42 pagesFatf PDFHEMANT SARVANKARNo ratings yet

- Format Description Mt103 RCM v1 0 RCCDocument10 pagesFormat Description Mt103 RCM v1 0 RCCharirk1986No ratings yet

- IRS Pub 2194 - Disaster Relief Tax AddendumDocument136 pagesIRS Pub 2194 - Disaster Relief Tax AddendumdonlucekNo ratings yet

- Parreno Vs COADocument1 pageParreno Vs COAPortia WynonaNo ratings yet

- SPL Digest CasesDocument12 pagesSPL Digest CasesMikaelGo-OngNo ratings yet

- Moot Court MemorialDocument7 pagesMoot Court MemorialHETRAM SIYAG100% (1)

- Law 126: Evidence Ma'am Victoria Avena: Drilon1Document37 pagesLaw 126: Evidence Ma'am Victoria Avena: Drilon1cmv mendozaNo ratings yet

- Fernando vs. COADocument7 pagesFernando vs. COAedelyn rivasNo ratings yet

- What Is Corporate GovernanceDocument5 pagesWhat Is Corporate GovernanceAkif AlamNo ratings yet

- H SsipDocument4 pagesH SsipAnicadlien Ellipaw Inin50% (2)

- Sample Copy Not For Use: RepairconDocument11 pagesSample Copy Not For Use: RepairconSaskia RodenburgNo ratings yet

- Dwnload Full Cultural Anthropology 3rd Edition Bonvillain Test Bank PDFDocument35 pagesDwnload Full Cultural Anthropology 3rd Edition Bonvillain Test Bank PDFelizabethellisxaqyjtopmd100% (14)

- Sheryl L. Loesch, Clerk Re 5.10-Cv-00503, Gillespie V Thirteenth CircuitDocument46 pagesSheryl L. Loesch, Clerk Re 5.10-Cv-00503, Gillespie V Thirteenth CircuitNeil Gillespie100% (1)

- Bill of Rights by Atty. Anselmo S. Rodiel IVDocument78 pagesBill of Rights by Atty. Anselmo S. Rodiel IVAnselmo Rodiel IV100% (1)

- Complaint Affidavit SampleDocument3 pagesComplaint Affidavit SampleAzrael Cassiel100% (1)

- Negotiable Instruments ReviewerDocument16 pagesNegotiable Instruments ReviewerColee StiflerNo ratings yet

- Internal Audit CharterDocument5 pagesInternal Audit CharterUrsu BârlogeaNo ratings yet

- AKBAYAN Versus Aquino DigestDocument2 pagesAKBAYAN Versus Aquino DigestElaineMarcillaNo ratings yet

- Committee For Public Council Services Complaint With Springfield Over Public RecordsDocument52 pagesCommittee For Public Council Services Complaint With Springfield Over Public RecordsPatrick JohnsonNo ratings yet

- Reyes Vs AlmanzorDocument6 pagesReyes Vs AlmanzorEL Filibusterisimo Paul CatayloNo ratings yet

- Important NotesDocument8 pagesImportant NotesSimiNo ratings yet

- نموذج عقد بيع عقار - 2Document4 pagesنموذج عقد بيع عقار - 2hguelizNo ratings yet

- NUS Personal Data Consent For Job ApplicantsDocument2 pagesNUS Personal Data Consent For Job ApplicantsPrashant MittalNo ratings yet

- MLC 003Document13 pagesMLC 003Евгений Стародубов100% (1)

- Pub 195nc PDFDocument12 pagesPub 195nc PDFmalathi_enNo ratings yet

- Parinas Vs PaguintoDocument3 pagesParinas Vs PaguintoEarnswell Pacina TanNo ratings yet

- Engineering Ethics and Professional Conduct - CasesDocument13 pagesEngineering Ethics and Professional Conduct - CasesMoses KaswaNo ratings yet

- S-000-1654-0990V - 0 - 0010 Human Resource Management Plan NSRP Nghi SonDocument7 pagesS-000-1654-0990V - 0 - 0010 Human Resource Management Plan NSRP Nghi SonjenniferNo ratings yet

- Quo Warranto: Court. - The Solicitor General or A Public Prosecutor May, With The Permission of The Court in WhichDocument2 pagesQuo Warranto: Court. - The Solicitor General or A Public Prosecutor May, With The Permission of The Court in Whichanalou agustin villezaNo ratings yet

- John Driscoll v. Gloucester CityDocument12 pagesJohn Driscoll v. Gloucester CityNewJerseyPublicRadioNo ratings yet

- Company LawDocument2 pagesCompany LawShrayee MukherjiNo ratings yet

- PEOPLE V Simon-CrimlawDocument1 pagePEOPLE V Simon-CrimlawDann Nix100% (1)

- Human Rights Alert: Corrective Actions in Re: Litigation Involving Financial InstitutionsDocument3 pagesHuman Rights Alert: Corrective Actions in Re: Litigation Involving Financial InstitutionsHuman Rights Alert - NGO (RA)No ratings yet