You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Quasilinear Note PWDocument11 pagesQuasilinear Note PWParag WaknisNo ratings yet

- Chapter8 - Limited CommitmentDocument23 pagesChapter8 - Limited CommitmentParag WaknisNo ratings yet

- Chapter12 - LSRMT - Stochatic GrowthDocument16 pagesChapter12 - LSRMT - Stochatic GrowthParag WaknisNo ratings yet

- Introduction To Labor Search Models: Dr. Parag WaknisDocument27 pagesIntroduction To Labor Search Models: Dr. Parag WaknisParag WaknisNo ratings yet

- Introduction To Labor Search Models Diamond, Mortensen, & Pissarides ModelDocument39 pagesIntroduction To Labor Search Models Diamond, Mortensen, & Pissarides ModelParag WaknisNo ratings yet

- Demonetization Through Segmented MarketsDocument9 pagesDemonetization Through Segmented MarketsParag WaknisNo ratings yet

- ParagWaknis Blackeconomy Ideas4india PDFDocument3 pagesParagWaknis Blackeconomy Ideas4india PDFParag WaknisNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Purchase Order: Amazon Seller Services Private Limited - DelhiDocument6 pagesPurchase Order: Amazon Seller Services Private Limited - DelhiLeelaram Ram GuptaNo ratings yet

- Chapter 6 Supply, Demand, and Government Policies-EditedDocument26 pagesChapter 6 Supply, Demand, and Government Policies-Editedvikash vermaNo ratings yet

- Firm Brochure: A Full Service Law Firm Based in Kabul, AfghanistanDocument12 pagesFirm Brochure: A Full Service Law Firm Based in Kabul, AfghanistanAista Putra WisenewNo ratings yet

- EFU General Wins Achievement Award / Gold Medal of FPCCIDocument32 pagesEFU General Wins Achievement Award / Gold Medal of FPCCIawaisNo ratings yet

- BIR Ruling DA-11-08Document4 pagesBIR Ruling DA-11-08Nash Ortiz LuisNo ratings yet

- Complete 420 Manual SIS Unit 89Document231 pagesComplete 420 Manual SIS Unit 89Tri Wahyuningsih100% (1)

- (In Philippine Pesos) : Se Detendre La Plage IncDocument5 pages(In Philippine Pesos) : Se Detendre La Plage IncJheza Mae PitogoNo ratings yet

- E Government Towards A PA ApproachDocument25 pagesE Government Towards A PA ApproachRobby Indra LukmanNo ratings yet

- MidTerm-Govt.-accounting-RAMOS, ROSEMARIE CDocument12 pagesMidTerm-Govt.-accounting-RAMOS, ROSEMARIE Cagentnic100% (1)

- The Official Bulletin: 2012 Q1 / No. 635Document50 pagesThe Official Bulletin: 2012 Q1 / No. 635IATSENo ratings yet

- Mkuchajr ProposalDocument9 pagesMkuchajr ProposalinnocentmkuchajrNo ratings yet

- ISWK XII Economics (030) QP & MS REHEARSAL 1 (23-24)Document15 pagesISWK XII Economics (030) QP & MS REHEARSAL 1 (23-24)hanaNo ratings yet

- Assignmentkarla Company Provided The Following Information For 2016 PDF FreeDocument1 pageAssignmentkarla Company Provided The Following Information For 2016 PDF FreePatrisha Carpio BeleyNo ratings yet

- Supply: Meaning and ScopeDocument32 pagesSupply: Meaning and Scopesaket kumarNo ratings yet

- 2nd Batch Cases TaxDocument16 pages2nd Batch Cases TaxRay John Arandia DorigNo ratings yet

- Section 80P - Deduction For Co-Operative SocietiesDocument15 pagesSection 80P - Deduction For Co-Operative SocietiesSURESHNo ratings yet

- Tax Planning With Reference To New Business - NatureDocument26 pagesTax Planning With Reference To New Business - NatureasifanisNo ratings yet

- 693-Article Text-1187-2-10-20210911Document16 pages693-Article Text-1187-2-10-20210911FachrumNo ratings yet

- Cost Sheet For 2 BHKDocument1 pageCost Sheet For 2 BHKBharat SharmaNo ratings yet

- NIRC Outline With SectionsDocument16 pagesNIRC Outline With SectionstakyousNo ratings yet

- Forms BrgyDocument13 pagesForms BrgyErlinda LagunaNo ratings yet

- Living Wage Critique Version 1Document33 pagesLiving Wage Critique Version 1David FarrarNo ratings yet

- Business Regulatory Framework (M. Law) (Regular)Document127 pagesBusiness Regulatory Framework (M. Law) (Regular)Yogesh SaindaneNo ratings yet

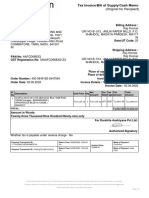

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)RoxdNo ratings yet

- Pamcor - Memorandum de LaraDocument17 pagesPamcor - Memorandum de LaraMikko Angela Axalan-PosioNo ratings yet

- Global Cash Card - Paystub Detail PDFDocument1 pageGlobal Cash Card - Paystub Detail PDFVerónica Del RioNo ratings yet

- Chapter 20 Homework SolutionDocument6 pagesChapter 20 Homework SolutionJackNo ratings yet

- Salary Wef 6 15Document3 pagesSalary Wef 6 15debdulaldamNo ratings yet

- Payment of Bonus Act 1965Document11 pagesPayment of Bonus Act 1965KNOWLEDGE CREATORS100% (2)

- CP PDF FinalDocument70 pagesCP PDF Finalvijaya100% (3)