You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Midterm TestDocument2 pagesMidterm TestHailee HayesNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Bibliography: BooksDocument14 pagesBibliography: BooksDilip KumarNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- 61089bos49694 Ipc Nov2019 gp1Document93 pages61089bos49694 Ipc Nov2019 gp1iswerya n.sNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Avinash Muthoot Finance ProjectDocument76 pagesAvinash Muthoot Finance ProjectSalman gs100% (1)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- IFRS 16 Leases - Basis of ConclusionDocument159 pagesIFRS 16 Leases - Basis of ConclusionErnest IpNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Creative AccountingDocument2 pagesCreative AccountingElton LopesNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- 40 - Financial Statements - TheoryDocument9 pages40 - Financial Statements - TheoryクロードNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Itc ValuationDocument31 pagesItc ValuationPrabhdeep DadyalNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Bank PerformanceDocument34 pagesBank Performancebr bhandariNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Financial StatementsDocument23 pagesFinancial StatementsShin Shan JeonNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Schroders: Schroder ISF Global SMLR Coms A Acc USDDocument2 pagesSchroders: Schroder ISF Global SMLR Coms A Acc USDSam AbdurahimNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Mrunal Sir Latest 2020 Handout 2 PDFDocument32 pagesMrunal Sir Latest 2020 Handout 2 PDFdaljit singhNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Sample Buyer Presentation - 2Document13 pagesSample Buyer Presentation - 2mauricio0327No ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- GO2 BankDocument1 pageGO2 Bank邱建华No ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Acctgchap 2Document15 pagesAcctgchap 2Anjelika ViescaNo ratings yet

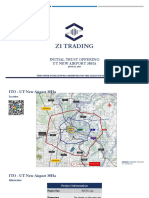

- UT New Airport 38ha - Project InformationDocument10 pagesUT New Airport 38ha - Project InformationPaul KitNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Company Profile HDFC BankDocument7 pagesCompany Profile HDFC Bankdominic wurdaNo ratings yet

- Tally 9Document326 pagesTally 9raju_rch100% (1)

- AC - OSE JUMMAI OGBONYA - APRIL, 2021 - 681964006 - FullStmtDocument5 pagesAC - OSE JUMMAI OGBONYA - APRIL, 2021 - 681964006 - FullStmtDauda jibrilNo ratings yet

- Concise Selina Solutions For Class 9 Maths Chapter 3 Compound Interest Using FormulaDocument42 pagesConcise Selina Solutions For Class 9 Maths Chapter 3 Compound Interest Using FormulaNarayanamurthy AmirapuNo ratings yet

- Loan CalculatorDocument4 pagesLoan CalculatorSumit GuptaNo ratings yet

- Hedge Fund BackersDocument6 pagesHedge Fund Backers1c796e65b8a4c8No ratings yet

- Developing The Philippines's Parametric and Crop Insurance IndustryDocument14 pagesDeveloping The Philippines's Parametric and Crop Insurance IndustryKarloAdrianoNo ratings yet

- Nationalisation of BanksDocument10 pagesNationalisation of BanksKavitha prabhakaranNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Sit Land Holdings LTDDocument2 pagesSit Land Holdings LTDnooneNo ratings yet

- CP 1 Consolidated Foods DataDocument5 pagesCP 1 Consolidated Foods DataASHUTOSH BISWALNo ratings yet

- About: Prudential PLCDocument8 pagesAbout: Prudential PLCMillton LucanoNo ratings yet

- Accounting For Liabilities: Learning ObjectivesDocument39 pagesAccounting For Liabilities: Learning ObjectivesJune KooNo ratings yet

- FAR Preweek Lecture (B42)Document14 pagesFAR Preweek Lecture (B42)Ciarie Mae Salgado50% (4)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- IDFC FIRST Bank Limited Sixth Annual Report FY 2019 20Document273 pagesIDFC FIRST Bank Limited Sixth Annual Report FY 2019 20Nihal YnNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)