You might also like

- Fundamental and Technical Analysis - Technical PaperDocument16 pagesFundamental and Technical Analysis - Technical PaperGauree AravkarNo ratings yet

- Tutorial 1 Q ADocument5 pagesTutorial 1 Q AKelvin LeongNo ratings yet

- Malayang Samahan NG Mga Manggagawa Sa M. Greenfield (Msmg-Uwp) v. RamosDocument3 pagesMalayang Samahan NG Mga Manggagawa Sa M. Greenfield (Msmg-Uwp) v. RamosAbigayle RecioNo ratings yet

- ACCA F6 Mock Exam QuestionsDocument22 pagesACCA F6 Mock Exam QuestionsGeo Don100% (1)

- Consulting Career PrimerDocument19 pagesConsulting Career PrimerAsgar AliNo ratings yet

- Wealth Management Planning: The UK Tax PrinciplesFrom EverandWealth Management Planning: The UK Tax PrinciplesRating: 4.5 out of 5 stars4.5/5 (2)

- Income Taxation 2019 Chapter 13A 13C 14 BanggawanDocument8 pagesIncome Taxation 2019 Chapter 13A 13C 14 BanggawanEricka Einjhel Lachama100% (8)

- Mizanul HikmahDocument1,038 pagesMizanul HikmahEjaz Husain100% (3)

- Audit of InventoryDocument7 pagesAudit of InventoryDianne Antoinette Basallo0% (1)

- d18 Atxuk QPDocument15 pagesd18 Atxuk QPakankshaNo ratings yet

- Advanced Taxation - United Kingdom (Atx - Uk) : Strategic Professional - OptionsDocument13 pagesAdvanced Taxation - United Kingdom (Atx - Uk) : Strategic Professional - OptionsRaza AliNo ratings yet

- Atxuk-2019-Marjun Sample-Q PDFDocument12 pagesAtxuk-2019-Marjun Sample-Q PDFONASHI DEVNANI BBANo ratings yet

- Advanced Taxation - United Kingdom (Atx - Uk) : Strategic Professional - OptionsDocument14 pagesAdvanced Taxation - United Kingdom (Atx - Uk) : Strategic Professional - OptionsRaza AliNo ratings yet

- TXUK 2018 SepDec QDocument9 pagesTXUK 2018 SepDec QmdNo ratings yet

- ATX - UK Sample Questions SummaryDocument15 pagesATX - UK Sample Questions SummaryONASHI DEVNANI BBANo ratings yet

- Taxation (United Kingdom) : September/December 2017 - Sample QuestionsDocument9 pagesTaxation (United Kingdom) : September/December 2017 - Sample QuestionsAyushman BhardwajNo ratings yet

- Taxation - United Kingdom (TX - UK) : Applied SkillsDocument17 pagesTaxation - United Kingdom (TX - UK) : Applied Skillsbuls eyeNo ratings yet

- Advanced Taxation (United Kingdom) : September/December 2016 - Sample QuestionsDocument17 pagesAdvanced Taxation (United Kingdom) : September/December 2016 - Sample QuestionsRaza AliNo ratings yet

- Taxation (United Kingdom) : March/June 2016 - Sample QuestionsDocument15 pagesTaxation (United Kingdom) : March/June 2016 - Sample QuestionsAmbreen KureemunNo ratings yet

- ACCA TX (F6) Tax Rates and Allowance Exam Formulae 2018Document3 pagesACCA TX (F6) Tax Rates and Allowance Exam Formulae 2018Katuta MwenyaNo ratings yet

- f6 Uk Specimen s16Document28 pagesf6 Uk Specimen s16Waleed QasimNo ratings yet

- Tx-Uk Mock 1Document20 pagesTx-Uk Mock 1Lalan JaiswalNo ratings yet

- Tax-Uk-J23-M24 Examinable Documents-Fa 2022Document6 pagesTax-Uk-J23-M24 Examinable Documents-Fa 2022chumnhomauxanhNo ratings yet

- Jun 2015 Q PDFDocument14 pagesJun 2015 Q PDFAmbreen KureemunNo ratings yet

- 14 - Tax TableDocument5 pages14 - Tax Tableayushagarwal23No ratings yet

- TX Uk Tax Rates June23 Mar24Document5 pagesTX Uk Tax Rates June23 Mar24Big SmutNo ratings yet

- Jun 2014 Q PDFDocument14 pagesJun 2014 Q PDFAmbreen KureemunNo ratings yet

- Examinable Documents, K and ATX-UK - FA 2019 Exam Docs June 20 To March 21 - Draft 2 (Clean) PDFDocument5 pagesExaminable Documents, K and ATX-UK - FA 2019 Exam Docs June 20 To March 21 - Draft 2 (Clean) PDFJudithNo ratings yet

- TX Uk j22 m23 TaxtablesDocument5 pagesTX Uk j22 m23 TaxtablesShafna ShamnasNo ratings yet

- TX Study School For Jul-Dec 2023 SemesterDocument18 pagesTX Study School For Jul-Dec 2023 Semestermaharajabby81No ratings yet

- f6 Mock QuestionDocument24 pagesf6 Mock QuestionSarad KharelNo ratings yet

- TX-UK and ATX-UK - FA 2020 Exam Docs June 21 To March 22 - FinalDocument7 pagesTX-UK and ATX-UK - FA 2020 Exam Docs June 21 To March 22 - FinalRidwan AhmedNo ratings yet

- Tax Rates and Allowances (FA23)Document6 pagesTax Rates and Allowances (FA23)nancybao0316No ratings yet

- Tax Table December 2020Document3 pagesTax Table December 2020Mohamed ShaminNo ratings yet

- TX NotesDocument157 pagesTX Notessahalacca123No ratings yet

- Paper F6 Taxation: Revision Mock Examination September 2016 Question PaperDocument22 pagesPaper F6 Taxation: Revision Mock Examination September 2016 Question PaperAhmed SabryNo ratings yet

- FTX (Uk) JDocument4 pagesFTX (Uk) JpavishneNo ratings yet

- Preparing Taxation Computations (UK Stream) : Tuesday 15 June 2010Document12 pagesPreparing Taxation Computations (UK Stream) : Tuesday 15 June 2010Erdene DexNo ratings yet

- Acca-F6uk 2009 Dec q-090820101Document13 pagesAcca-F6uk 2009 Dec q-090820101annez3112No ratings yet

- F6uk 2010 Dec Q PDFDocument10 pagesF6uk 2010 Dec Q PDFInsia AhmedNo ratings yet

- P6uk 2008 Dec QDocument14 pagesP6uk 2008 Dec QHassan BilalNo ratings yet

- Tax Tables 2018 19 - 4Document8 pagesTax Tables 2018 19 - 4Alellie Khay JordanNo ratings yet

- P6uk 2007 Dec Q PDFDocument12 pagesP6uk 2007 Dec Q PDFHassan BilalNo ratings yet

- Income Tax Rates and Allowances 2022-23 SummaryDocument5 pagesIncome Tax Rates and Allowances 2022-23 SummaryAmmaarah PatelNo ratings yet

- Advanced Taxation (United Kingdom) : Monday 2 June 2008Document14 pagesAdvanced Taxation (United Kingdom) : Monday 2 June 2008Hassan BilalNo ratings yet

- Acca 08Document11 pagesAcca 08anon-854895No ratings yet

- F6 Exam DetailDocument4 pagesF6 Exam DetailDanish HabibNo ratings yet

- CIPP Payroll FactcardDocument8 pagesCIPP Payroll FactcardRoxana GiurcaNo ratings yet

- Cii Tax Tables 2020 2021 Tax Tables 310321 To 310821Document5 pagesCii Tax Tables 2020 2021 Tax Tables 310321 To 310821stellaNo ratings yet

- Taxtable 2022 23 - FinalDocument3 pagesTaxtable 2022 23 - FinalfmpallabNo ratings yet

- Tax rates 2019/20 overviewDocument4 pagesTax rates 2019/20 overviewIssa BoyNo ratings yet

- Exam Paper - MainDocument10 pagesExam Paper - Main2016-ME-15 AnsabNo ratings yet

- Tax Card 2018/2019: Important NoticeDocument2 pagesTax Card 2018/2019: Important NoticeAhmed BilalNo ratings yet

- Tax Card 2022 v2Document2 pagesTax Card 2022 v2Ali AyubNo ratings yet

- Taxation in UKDocument15 pagesTaxation in UKluaybazNo ratings yet

- P6-Income Tax CalculationDocument15 pagesP6-Income Tax CalculationAnonymous rePT5rCr0% (1)

- UK TaxDocument8 pagesUK TaxAvinash sncsNo ratings yet

- Default Tariff Cap Level - LetterDocument3 pagesDefault Tariff Cap Level - LetterAlex ButcherNo ratings yet

- ChangesinFinanceAct2022 23Document8 pagesChangesinFinanceAct2022 23rightvisiontaxsolution3No ratings yet

- CPD Course: 30 MinsDocument12 pagesCPD Course: 30 MinsDavid BriggsNo ratings yet

- Answers: Tuition (Course) ExaminationDocument16 pagesAnswers: Tuition (Course) ExaminationHussein SeetalNo ratings yet

- Tax Year Rates and Allowances 2018/2019Document9 pagesTax Year Rates and Allowances 2018/2019kat_zoeNo ratings yet

- Value of The NHS Pension Scheme FINALDocument62 pagesValue of The NHS Pension Scheme FINALpboletaNo ratings yet

- Calculating Average Rate of Return (ARR) : Method and Worked ExampleDocument4 pagesCalculating Average Rate of Return (ARR) : Method and Worked ExamplehjycjycjycNo ratings yet

- Principles of Taxation 2019 ICAS IMPDocument803 pagesPrinciples of Taxation 2019 ICAS IMPVeronica BaileyNo ratings yet

- Model Scottish Budget 2018/19 (June 2018)Document10 pagesModel Scottish Budget 2018/19 (June 2018)msp-archiveNo ratings yet

- Tax Planning Advice for REP Limited and LamarDocument10 pagesTax Planning Advice for REP Limited and LamarJalees Ul HassanNo ratings yet

- Faqs For Acca Members: 1. What Is The Mra About? Does It Apply To Me?Document3 pagesFaqs For Acca Members: 1. What Is The Mra About? Does It Apply To Me?Dilawar HayatNo ratings yet

- ACCA Exam History DetailsDocument3 pagesACCA Exam History DetailsDilawar HayatNo ratings yet

- MJ17 Hybrids F9 Clean ProofDocument6 pagesMJ17 Hybrids F9 Clean ProofVinny Lu VLNo ratings yet

- Financial Management: September/December 2017 - Sample QuestionsDocument6 pagesFinancial Management: September/December 2017 - Sample QuestionsVinny Lu VLNo ratings yet

- Password CompDocument1 pagePassword CompDilawar HayatNo ratings yet

- f9 2018 Marjun QDocument6 pagesf9 2018 Marjun QDilawar HayatNo ratings yet

- Financial Management Fundamentals Level Skills Module NPV CalculationDocument8 pagesFinancial Management Fundamentals Level Skills Module NPV CalculationgulhasanNo ratings yet

- Subject: Casual Leave Application: TH THDocument1 pageSubject: Casual Leave Application: TH THDilawar HayatNo ratings yet

- SD17 Hybrid F9 Answers Clean ProofDocument10 pagesSD17 Hybrid F9 Answers Clean ProofVinny Lu VLNo ratings yet

- 'Abdallāh Al-Samāhijī's "Munyat Al-MumārisīnDocument30 pages'Abdallāh Al-Samāhijī's "Munyat Al-Mumārisīnba7raini100% (1)

- 'Abdallāh Al-Samāhijī's "Munyat Al-MumārisīnDocument30 pages'Abdallāh Al-Samāhijī's "Munyat Al-Mumārisīnba7raini100% (1)

- P6uk 2018 Mar - Jun QDocument14 pagesP6uk 2018 Mar - Jun QDilawar HayatNo ratings yet

- A Brief History of The Fourteen InfalliblesDocument9 pagesA Brief History of The Fourteen InfalliblesDilawar HayatNo ratings yet

- P6UK 2017 Sep Dec Hybrid ADocument11 pagesP6UK 2017 Sep Dec Hybrid ADilawar HayatNo ratings yet

- P6uk 2018 Jun ADocument11 pagesP6uk 2018 Jun ADilawar HayatNo ratings yet

- As Sahifa DuaKumailDocument113 pagesAs Sahifa DuaKumailImammiyah HallNo ratings yet

- P6UK 2017 Sep Dec Hybrid Qs v2Document17 pagesP6UK 2017 Sep Dec Hybrid Qs v2Dilawar HayatNo ratings yet

- Christians Who Defended and Died For Muhammad and His Family - Mateen J. CharbonneauDocument53 pagesChristians Who Defended and Died For Muhammad and His Family - Mateen J. CharbonneauCarlosAmadorFonseca100% (1)

- F8int 2011 Dec ADocument14 pagesF8int 2011 Dec ADilawar HayatNo ratings yet

- Thirdpartyrep Brand Guide 052314Document39 pagesThirdpartyrep Brand Guide 052314Tasfin HabibNo ratings yet

- CadburyDocument11 pagesCadburyAnkita RajNo ratings yet

- HK Companies Ordinance Auditor ReportsDocument23 pagesHK Companies Ordinance Auditor Reportsbbe431No ratings yet

- Aditya Vikram Birla KimigrgDocument9 pagesAditya Vikram Birla KimigrgKeeran TamusyoNo ratings yet

- Precio de Acido Sulfurico 7Document11 pagesPrecio de Acido Sulfurico 7Ronaldo CMNo ratings yet

- Chapter 2 The Business Vision MissionDocument61 pagesChapter 2 The Business Vision MissionKang MarvinsNo ratings yet

- Organizing Genius - The Skunk WorksDocument14 pagesOrganizing Genius - The Skunk WorksAbhimanyu SinghNo ratings yet

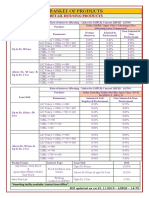

- BASKET OF RETAIL PRODUCTS RATESDocument3 pagesBASKET OF RETAIL PRODUCTS RATESVirendra K VermaNo ratings yet

- 5Cs Consolidaiton of Fragmented IndustriesDocument20 pages5Cs Consolidaiton of Fragmented Industriesxavier25100% (2)

- Edelman Appoints Kerry Irwin To Lead Re-Launch of Edelman in RussiaDocument1 pageEdelman Appoints Kerry Irwin To Lead Re-Launch of Edelman in RussiaEdelmanNo ratings yet

- Cost Accounting Basics and Job Order CycleDocument22 pagesCost Accounting Basics and Job Order CycleJi Baltazar100% (1)

- RJR Nabisco LBODocument14 pagesRJR Nabisco LBONazir Ahmad BahariNo ratings yet

- Contact Sushant Kumar Add Sushant Kumar To Your NetworkDocument2 pagesContact Sushant Kumar Add Sushant Kumar To Your NetworkJaspreet Singh SahaniNo ratings yet

- BrandingDocument28 pagesBrandingTejal PatilNo ratings yet

- Doubtful AccountsDocument2 pagesDoubtful AccountsCharles Reginald K. HwangNo ratings yet

- 057.AINIO & Associates Pty LTD: Current & Historical Company ExtractDocument5 pages057.AINIO & Associates Pty LTD: Current & Historical Company ExtractFlinders TrusteesNo ratings yet

- Annexure 2 To Amfi BP Cir No 68 - Supplementary Ckyc FormDocument2 pagesAnnexure 2 To Amfi BP Cir No 68 - Supplementary Ckyc Formapi-349453187No ratings yet

- Setting The Record Straight: Truths About Indexing: Vanguard Research January 2018Document12 pagesSetting The Record Straight: Truths About Indexing: Vanguard Research January 2018TBP_Think_TankNo ratings yet

- Solvency / Ratio/ Leverage / Liquididty AnalysisDocument142 pagesSolvency / Ratio/ Leverage / Liquididty AnalysisshobasridharNo ratings yet

- An Empirical Analysis of Auditor Reporting and Its Association With Abnormal AccrualsDocument27 pagesAn Empirical Analysis of Auditor Reporting and Its Association With Abnormal AccrualsMRRMNo ratings yet

- British Petroleum Annual Report 2005 Adoption IFRS 1Document119 pagesBritish Petroleum Annual Report 2005 Adoption IFRS 1RidlaNo ratings yet

- Bataan Shipyard v. PCGGDocument21 pagesBataan Shipyard v. PCGGRhoddickMagrataNo ratings yet

- Comparative Analysis of Broking FirmsDocument12 pagesComparative Analysis of Broking FirmsJames RamirezNo ratings yet

- Sem 1 2018 Mid Term With Venue - Elm Campus - pdf2Document3 pagesSem 1 2018 Mid Term With Venue - Elm Campus - pdf2Bear Bear LeongNo ratings yet