You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Civ Pro Q&ADocument7 pagesCiv Pro Q&ASGTNo ratings yet

- A Study in Mutual Funds in IndiaDocument91 pagesA Study in Mutual Funds in IndiaNazir Ahmad AmirNo ratings yet

- Assessment Paper and Instructions To Candidates:: FM320 - Quantitative Finance Suitable For All CandidatesDocument5 pagesAssessment Paper and Instructions To Candidates:: FM320 - Quantitative Finance Suitable For All CandidatesYingzhi XuNo ratings yet

- Republic v. ManaloDocument19 pagesRepublic v. ManaloSif Ivaldi (Sif)No ratings yet

- House of Representatives Electoral Tribunal and Teodoro C. Cruz, Respondents. Kapunan, J.Document3 pagesHouse of Representatives Electoral Tribunal and Teodoro C. Cruz, Respondents. Kapunan, J.Zachary BañezNo ratings yet

- The FactsDocument28 pagesThe FactsAlfred DanezNo ratings yet

- 05 Manongsong v. EstimoDocument8 pages05 Manongsong v. EstimoCharles MagistradoNo ratings yet

- 02 Santos v. CADocument6 pages02 Santos v. CACharles MagistradoNo ratings yet

- Mo Ya Lim Yao v. CIMDocument47 pagesMo Ya Lim Yao v. CIMCharles MagistradoNo ratings yet

- People v. CabilesDocument2 pagesPeople v. CabilesCharles MagistradoNo ratings yet

- Dizon v. CA 302 SCRA 288 (1999)Document7 pagesDizon v. CA 302 SCRA 288 (1999)JMae MagatNo ratings yet

- 126 MBTC v. ASB HoldingsDocument8 pages126 MBTC v. ASB HoldingsCharles MagistradoNo ratings yet

- 127 Sps. Sobrejuanite v. ASB DevelopmentDocument6 pages127 Sps. Sobrejuanite v. ASB DevelopmentCharles MagistradoNo ratings yet

- 03 Sps. Buenaventura v. CADocument7 pages03 Sps. Buenaventura v. CACharles MagistradoNo ratings yet

- Metropolitan Waterworks Vs Hon. DawaynGR No. 160732, June 21, 2004-LAW GOVERNING LCDocument7 pagesMetropolitan Waterworks Vs Hon. DawaynGR No. 160732, June 21, 2004-LAW GOVERNING LCDuko Alcala EnjambreNo ratings yet

- 121 JL Bernardo Construction v. CADocument7 pages121 JL Bernardo Construction v. CACharles MagistradoNo ratings yet

- Supreme Court Decision on Property Ownership DisputeDocument10 pagesSupreme Court Decision on Property Ownership DisputeCharles MagistradoNo ratings yet

- 120 de Barreto v. VillanuevaDocument7 pages120 de Barreto v. VillanuevaCharles MagistradoNo ratings yet

- 11 Evangelista & Co. v. Abad SantosDocument5 pages11 Evangelista & Co. v. Abad SantosCharles MagistradoNo ratings yet

- SEC ruling on Ruby Industrial Corporation rehabilitation planDocument9 pagesSEC ruling on Ruby Industrial Corporation rehabilitation planCharles MagistradoNo ratings yet

- 123 RCBC v. IAC and BF HomesDocument9 pages123 RCBC v. IAC and BF HomesCharles MagistradoNo ratings yet

- Council of Red Men Vs Veterans Army, 7 Phil 685, 1907Document3 pagesCouncil of Red Men Vs Veterans Army, 7 Phil 685, 1907Dianne BalagsoNo ratings yet

- 119 Uy v. ZamoraDocument2 pages119 Uy v. ZamoraCharles MagistradoNo ratings yet

- 12 Realubit v. JasoDocument5 pages12 Realubit v. JasoCharles MagistradoNo ratings yet

- 05 Viray v. PeopleDocument9 pages05 Viray v. PeopleCharles MagistradoNo ratings yet

- 10 Lim & Galvez v. SengDocument5 pages10 Lim & Galvez v. SengGene Charles MagistradoNo ratings yet

- 5 Litton Vs HillDocument5 pages5 Litton Vs HillIreneLeahC.RomeroNo ratings yet

- Council of Red Men Vs Veterans Army, 7 Phil 685, 1907Document3 pagesCouncil of Red Men Vs Veterans Army, 7 Phil 685, 1907Dianne BalagsoNo ratings yet

- 10 Lim & Galvez v. SengDocument5 pages10 Lim & Galvez v. SengGene Charles MagistradoNo ratings yet

- 5 Litton Vs HillDocument5 pages5 Litton Vs HillIreneLeahC.RomeroNo ratings yet

- Supreme Court Rules on Religious Freedom Case Involving Court Interpreter's Conjugal ArrangementDocument58 pagesSupreme Court Rules on Religious Freedom Case Involving Court Interpreter's Conjugal ArrangementShantle Taciana P. FabicoNo ratings yet

- 11 Evangelista & Co. v. Abad SantosDocument5 pages11 Evangelista & Co. v. Abad SantosCharles MagistradoNo ratings yet

- Silverio vs. RepublicDocument7 pagesSilverio vs. RepublicpatriceNo ratings yet

- Project Planning Analysis and ManagementDocument24 pagesProject Planning Analysis and Managementnaren mishra100% (1)

- Haryana SSC Staff Selection ReceiptDocument1 pageHaryana SSC Staff Selection ReceiptAshu BansalNo ratings yet

- GLENMARK PHARMA OVERVIEWDocument6 pagesGLENMARK PHARMA OVERVIEWdarshan jainNo ratings yet

- Ratio Analysis & Financial Benchmarking for NonprofitsDocument38 pagesRatio Analysis & Financial Benchmarking for NonprofitsRehan NasirNo ratings yet

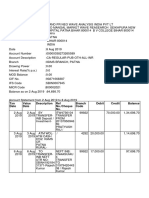

- TXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceDocument3 pagesTXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceNishi GuptaNo ratings yet

- Sentença ACP 0800224-44 - 2013 - 8 - 01 - 0001Document120 pagesSentença ACP 0800224-44 - 2013 - 8 - 01 - 0001IsaacBenevidesNo ratings yet

- Management Accounting Systems inDocument9 pagesManagement Accounting Systems inanashj2No ratings yet

- Tax Sheltered SchemesDocument13 pagesTax Sheltered SchemesVivek DwivediNo ratings yet

- Kinh Do Group Corporation (KDC) : Relentless Business ExpansionDocument6 pagesKinh Do Group Corporation (KDC) : Relentless Business ExpansionSujata ShashiNo ratings yet

- F 4506Document2 pagesF 4506kittie_86No ratings yet

- Integration Layout TXT Suministrolr Aeat Sii v5Document53 pagesIntegration Layout TXT Suministrolr Aeat Sii v5Murdum MurdumNo ratings yet

- Leonardo Bognot V RRI Lending CorporationDocument10 pagesLeonardo Bognot V RRI Lending CorporationMarchini Sandro Cañizares KongNo ratings yet

- CKSBDocument23 pagesCKSBayushiNo ratings yet

- Eurobonds: Euro BondsDocument5 pagesEurobonds: Euro BondssuperjagdishNo ratings yet

- BWN JC 110112 (Init)Document28 pagesBWN JC 110112 (Init)Ana WesselNo ratings yet

- Tamilnadu Pension Calculation ARREARS SoftwareDocument13 pagesTamilnadu Pension Calculation ARREARS Softwarejayakumarbalaji50% (4)

- Financial Awareness and Economic ScenariosDocument4 pagesFinancial Awareness and Economic ScenariosSuvasish DasguptaNo ratings yet

- FinalsDocument11 pagesFinalsTong KennedyNo ratings yet

- Bank entitled to sell pledged shares in default of Islamic facilityDocument16 pagesBank entitled to sell pledged shares in default of Islamic facilityabdul rahimNo ratings yet

- Final Assignment AstDocument6 pagesFinal Assignment AstAngelica CerioNo ratings yet

- Republic of Kenya: Kenya Gazette Supplement No. 107 (Acts No.11)Document26 pagesRepublic of Kenya: Kenya Gazette Supplement No. 107 (Acts No.11)Benard OderoNo ratings yet

- AE 315 FM Sum2021 Week 3 Capital Budgeting Quiz Anserki B FOR DISTRIBDocument7 pagesAE 315 FM Sum2021 Week 3 Capital Budgeting Quiz Anserki B FOR DISTRIBArly Kurt TorresNo ratings yet

- General Power of AttorneyDocument1 pageGeneral Power of AttorneyAriel Hartung100% (1)

- Management Accounting Overhead VariancesDocument12 pagesManagement Accounting Overhead VariancesNors PataytayNo ratings yet

- Bangko Sentral NG Pilipinas Coins and Notes - Commemorative CurrencDocument4 pagesBangko Sentral NG Pilipinas Coins and Notes - Commemorative Currencrafael oviedoNo ratings yet

- Stock Exchange in India OverviewDocument72 pagesStock Exchange in India OverviewRizwana BegumNo ratings yet

- Equity Methods - ECIB - Tax Settlement ForecastingDocument13 pagesEquity Methods - ECIB - Tax Settlement ForecastingmzurzdcoNo ratings yet