You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Wk8 Laura Martin REPORTDocument18 pagesWk8 Laura Martin REPORTNino Chen100% (2)

- Klabin Reports 2nd Quarter Earnings of R$ 15 Million: HighlightsDocument10 pagesKlabin Reports 2nd Quarter Earnings of R$ 15 Million: HighlightsKlabin_RINo ratings yet

- What Is The Magic Formula GreenblattDocument14 pagesWhat Is The Magic Formula GreenblattChrisTheodorouNo ratings yet

- Granules India Research Reports Investors PresentationDocument51 pagesGranules India Research Reports Investors Presentationvasu.nadapanaNo ratings yet

- Airtel Case Study PDFDocument14 pagesAirtel Case Study PDFMohit RanaNo ratings yet

- EC Bulletin Annual Incentive Plan Design SurveyDocument6 pagesEC Bulletin Annual Incentive Plan Design SurveyVikas RamavarmaNo ratings yet

- Of Long-Term Growth: Nurturing The RootsDocument68 pagesOf Long-Term Growth: Nurturing The RootsDhea Rizky AprillaNo ratings yet

- Nestle & Alcon - The Value of A ListingDocument9 pagesNestle & Alcon - The Value of A ListingSreya DeNo ratings yet

- SMIFS Research Everest Industries LTD ICRDocument19 pagesSMIFS Research Everest Industries LTD ICRMahamadali DesaiNo ratings yet

- Building A 3 Statement Financial Model: in ExcelDocument85 pagesBuilding A 3 Statement Financial Model: in ExcelSureshNo ratings yet

- Case: AUTOZONE, INC.Document17 pagesCase: AUTOZONE, INC.rzannat94100% (2)

- Accounting Assignment # 02Document8 pagesAccounting Assignment # 02Amna YounasNo ratings yet

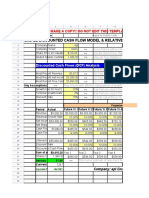

- Simple Discounted Cash Flow Model & Relative ValuationDocument14 pagesSimple Discounted Cash Flow Model & Relative ValuationlearnNo ratings yet

- Relative Valuation JaiDocument29 pagesRelative Valuation JaiGarima SinghNo ratings yet

- SynergyDocument19 pagesSynergyYash AgarwalNo ratings yet

- Financial Analysis AssignmentDocument5 pagesFinancial Analysis AssignmentSaifiNo ratings yet

- Ubs I Banking GuideDocument47 pagesUbs I Banking GuideMukund SinghNo ratings yet

- Indoor Soccer Facility Business PlanDocument30 pagesIndoor Soccer Facility Business Planoj123456No ratings yet

- Ar 2019 # Samindo-4 PDFDocument271 pagesAr 2019 # Samindo-4 PDFpradityo88100% (1)

- Rapport ORBIS Sur SCR MOTORS IMPORT EXPORT CO LTD PDFDocument29 pagesRapport ORBIS Sur SCR MOTORS IMPORT EXPORT CO LTD PDFmoiNo ratings yet

- R56 Fundamentals of Credit AnalysisDocument23 pagesR56 Fundamentals of Credit AnalysisDiegoNo ratings yet

- Tips For CpaleDocument14 pagesTips For CpaleJerson FerrerNo ratings yet

- MAXIS Annual Report 2010 (2.8MB)Document283 pagesMAXIS Annual Report 2010 (2.8MB)Tee Chee KeongNo ratings yet

- Royal Vopak Annual Report 2016Document227 pagesRoyal Vopak Annual Report 2016Anonymous Hnv6u54HNo ratings yet

- AMT - Pro FormaDocument8 pagesAMT - Pro FormaConorTimmins100% (1)

- Financial Statements, Taxes, and Cash Flow: Mcgraw-Hill/IrwinDocument25 pagesFinancial Statements, Taxes, and Cash Flow: Mcgraw-Hill/IrwinDani Yustiardi MunarsoNo ratings yet

- Report IFA For Norway On Interest DeductionDocument19 pagesReport IFA For Norway On Interest DeductionAnna ScaoaNo ratings yet

- Problemset5 AnswersDocument11 pagesProblemset5 AnswersHowo4DieNo ratings yet

- CityFibre Infrastructure Holdings PLC Preliminary Statement of Annual Results Year Ended 31 December 2017Document16 pagesCityFibre Infrastructure Holdings PLC Preliminary Statement of Annual Results Year Ended 31 December 2017Hubert CierpicaNo ratings yet

- Valeo 2017 Registration DocumentDocument454 pagesValeo 2017 Registration DocumentFadyNo ratings yet