You might also like

- Copia de Informe - Diario - Produccion 21 01 2021Document27 pagesCopia de Informe - Diario - Produccion 21 01 2021yeremeNo ratings yet

- Analyzing Quality Constraints in Sri Lankan Cinnamon Value ChainDocument26 pagesAnalyzing Quality Constraints in Sri Lankan Cinnamon Value ChainsenarathNo ratings yet

- Coffee Report and Outlook April 2023 - ICODocument39 pagesCoffee Report and Outlook April 2023 - ICOsyifa amaliaNo ratings yet

- Presentation by Dewan Mushtaq GroupDocument21 pagesPresentation by Dewan Mushtaq Groupmms_mzNo ratings yet

- Session 4 SPE Training Exceptional Price PerformanceDocument67 pagesSession 4 SPE Training Exceptional Price PerformanceJarodNo ratings yet

- Sugar Industry: PakistanDocument17 pagesSugar Industry: PakistanMuhammad AwaisNo ratings yet

- An Overview of Thai Sugar IndustryDocument8 pagesAn Overview of Thai Sugar IndustrysuonodimusicaNo ratings yet

- Compañía de Minas Buenaventura S.A.ADocument34 pagesCompañía de Minas Buenaventura S.A.AVictor ValdiviaNo ratings yet

- Business EconmicsDocument24 pagesBusiness EconmicsIrshad HussainNo ratings yet

- EnergyEthanolOutlook091918 PDFDocument16 pagesEnergyEthanolOutlook091918 PDFAbbas NisyaNo ratings yet

- Ethanol OutlookDocument16 pagesEthanol OutlookAbbas NisyaNo ratings yet

- Oilseeds Update November 2020Document40 pagesOilseeds Update November 2020Andry HoesniNo ratings yet

- Sugar Annual - Kingston - Jamaica - 04-15-2021Document8 pagesSugar Annual - Kingston - Jamaica - 04-15-2021Zineil BlackwoodNo ratings yet

- "Challenges and Development": Hailand Ugar ProductionDocument35 pages"Challenges and Development": Hailand Ugar ProductionnghiNo ratings yet

- Coffee Market in The USDocument110 pagesCoffee Market in The USRitika SinghalNo ratings yet

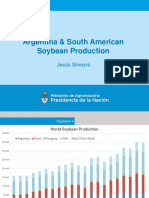

- A Reference Guide To Important Soybean Facts & FiguresDocument36 pagesA Reference Guide To Important Soybean Facts & FiguresBryan KuoKyNo ratings yet

- Mapa Base Regional KayraDocument1 pageMapa Base Regional KayraRENE SULLCA HUAMANINo ratings yet

- Nilai Genap Produktif AK NajwaDocument24 pagesNilai Genap Produktif AK NajwaMI Khairul FalahNo ratings yet

- Crops 0Document45 pagesCrops 0Sukhwant BhullarNo ratings yet

- 1 Current Status of Shrimp Aquaculture in India Anil Kumar FinalDocument21 pages1 Current Status of Shrimp Aquaculture in India Anil Kumar FinalGen SoibamNo ratings yet

- A Deep Dive Into Coffee - Production VS ConsumptionDocument8 pagesA Deep Dive Into Coffee - Production VS ConsumptionMFRNo ratings yet

- Mapa Regional Base CorreDocument1 pageMapa Regional Base CorreRENE SULLCA HUAMANINo ratings yet

- Coffee Report and Outlook December 2023 ICODocument43 pagesCoffee Report and Outlook December 2023 ICOqiweijhihNo ratings yet

- FFHP 19Document48 pagesFFHP 19Danny GoldstoneNo ratings yet

- Sugar Annual - Kingston - Jamaica - JM2022-0003Document8 pagesSugar Annual - Kingston - Jamaica - JM2022-0003HALİM KILIÇNo ratings yet

- 08 Adhoc Sensitivity AnalysisDocument8 pages08 Adhoc Sensitivity AnalysisUdhav JoshiNo ratings yet

- Form Setoran Nilai Raport Semester Genap Taun Pelajaran 2019-2020Document3 pagesForm Setoran Nilai Raport Semester Genap Taun Pelajaran 2019-2020InaKhusniawatiNo ratings yet

- Royal Dutch ShellDocument6 pagesRoyal Dutch ShellBálint HorváthNo ratings yet

- Soy Stats 2023 WebDocument36 pagesSoy Stats 2023 WebjohnnyNo ratings yet

- 40 - KTS-CM-12Document8 pages40 - KTS-CM-12IrenataNo ratings yet

- Chocolate Confectionery in Peru ContextDocument2 pagesChocolate Confectionery in Peru ContextGonzalo De La CruzNo ratings yet

- US COFFEE MARKET INSIGHTSDocument117 pagesUS COFFEE MARKET INSIGHTSSafridNo ratings yet

- Presentación Soja Global GrainDocument21 pagesPresentación Soja Global GrainXoares PatxNo ratings yet

- Laporan Stock & Omzet Penjualan GloskinDocument32 pagesLaporan Stock & Omzet Penjualan GloskinTetra PerwiraNo ratings yet

- Presentation On: Crude Oil & U.S. Dollar VS Indian RupeeDocument14 pagesPresentation On: Crude Oil & U.S. Dollar VS Indian Rupeemanojsaini09No ratings yet

- Iraqi Date Industry: A Review of Production, Processing, and MarketingDocument64 pagesIraqi Date Industry: A Review of Production, Processing, and MarketingMuhammad Sohail AkramNo ratings yet

- RP Ind Technical Appendix ISO 440699 Cleanliness Level Standards PDFDocument2 pagesRP Ind Technical Appendix ISO 440699 Cleanliness Level Standards PDFSamuel SiregarNo ratings yet

- Serba Farm Organic PlantationDocument23 pagesSerba Farm Organic PlantationET Hadi SaputraNo ratings yet

- Laporan (Rapor) Pts Ganjil 2020-2021 Wals 9gDocument11 pagesLaporan (Rapor) Pts Ganjil 2020-2021 Wals 9gNopis AfandiNo ratings yet

- Secciones Linea de Impulsion FinalDocument1 pageSecciones Linea de Impulsion FinalREYNALDO MORE CARHUAPOMANo ratings yet

- Addressing Poverty Challenges in NigeriaDocument5 pagesAddressing Poverty Challenges in NigeriaDELIGHT OLUWASANYANo ratings yet

- National Bank of PakistanDocument45 pagesNational Bank of PakistanMK AbirNo ratings yet

- Nestlé's Entry into the Refrigerated Pizza Market in the Late 1980sDocument27 pagesNestlé's Entry into the Refrigerated Pizza Market in the Late 1980sRandhir Kumar100% (1)

- Bio FertiliserDocument23 pagesBio FertiliserMaqsood KhalidNo ratings yet

- Analysis of Organic Acids by HPLCDocument5 pagesAnalysis of Organic Acids by HPLCAlexanderNo ratings yet

- Caobisco 16022018090629 Caobisco 29062017163536 2018 Statistics ExtractDocument4 pagesCaobisco 16022018090629 Caobisco 29062017163536 2018 Statistics ExtractMilica BarjaktarevicNo ratings yet

- Reach Vally Order DecDocument60 pagesReach Vally Order DecmanbarotNo ratings yet

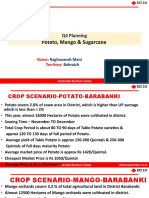

- Mango & Sugarcane Planning-Q4-BahraichDocument11 pagesMango & Sugarcane Planning-Q4-BahraichRishabh UpadhyayNo ratings yet

- Diamond: - Submitted ByDocument42 pagesDiamond: - Submitted ByAnkush GuptaNo ratings yet

- Ethanol, Red Meat Trade, and Food Security: Al Mussell, PHD Sr. Research AssociateDocument21 pagesEthanol, Red Meat Trade, and Food Security: Al Mussell, PHD Sr. Research AssociateEd ZNo ratings yet

- 110 - Anexo02.1 - TCC - ProtecaoFase - CDocument1 page110 - Anexo02.1 - TCC - ProtecaoFase - Cisaaf1No ratings yet

- Weekly Aquaculture Update - 2020-36Document3 pagesWeekly Aquaculture Update - 2020-36tNo ratings yet

- India MHM VConfDocument21 pagesIndia MHM VConfsanjnuNo ratings yet

- Presentation On Fertiliser Industry of IndiaDocument43 pagesPresentation On Fertiliser Industry of IndiaSyedMaazAliNo ratings yet

- Septic Tank Sizing CalculatorDocument1 pageSeptic Tank Sizing CalculatorA MNo ratings yet

- NRD Research Breifings #1 FinalDocument13 pagesNRD Research Breifings #1 FinalzahidiwaqarNo ratings yet

- India Wheat Production by Year (1000 MT)Document1 pageIndia Wheat Production by Year (1000 MT)karankumar8689783No ratings yet

- 02 Update On Measles Rubella EliminationDocument32 pages02 Update On Measles Rubella Eliminationnavneet singhNo ratings yet

- Doc. 2Document1 pageDoc. 2Widhi NugrahaNo ratings yet

- Scharffen Berger Chocolate MakerDocument6 pagesScharffen Berger Chocolate MakerRashmikanta MaharajNo ratings yet

- Doga Doga Ka Post Mart AmDocument58 pagesDoga Doga Ka Post Mart Amkrishna sharmaNo ratings yet

- 027 Nagraj Aur Super Commando Dhruv PDFDocument62 pages027 Nagraj Aur Super Commando Dhruv PDFtripsabhiNo ratings yet

- Binomial Theorem-Jee (Main)Document19 pagesBinomial Theorem-Jee (Main)Resonance Dlpd76% (76)

- WT Chapter 6 2Document21 pagesWT Chapter 6 2kanchanabalajiNo ratings yet

- Permissible Currents Conductor Electrical PDFDocument2 pagesPermissible Currents Conductor Electrical PDFkrishna sharmaNo ratings yet

- Chapter 18 FiltrationDocument18 pagesChapter 18 FiltrationGMDGMD11No ratings yet

- Centre of Mass-Jee (Main)Document60 pagesCentre of Mass-Jee (Main)Resonance Dlpd85% (84)

- Chacha Chaudhary Aur Billoo Aur Pinky PDFDocument63 pagesChacha Chaudhary Aur Billoo Aur Pinky PDFRahulNo ratings yet

- Mauritius Sugar ByproductsDocument13 pagesMauritius Sugar ByproductsNashon AsekaNo ratings yet

- Electronic Effects & Applications - Jee (Main)Document52 pagesElectronic Effects & Applications - Jee (Main)Resonance Dlpd87% (109)

- Catalog RozaiTotal eDocument9 pagesCatalog RozaiTotal ekrishna sharmaNo ratings yet

- Material Data Sheets For Piping: 1 ForewordDocument50 pagesMaterial Data Sheets For Piping: 1 ForewordhsdeNo ratings yet

- Souders Brown EquationDocument1 pageSouders Brown Equationkrishna sharmaNo ratings yet

- Filtration CHP 12Document103 pagesFiltration CHP 12learningboxNo ratings yet

- Milling Mixed Juice Mixed Juice Heating: Filter CakeDocument4 pagesMilling Mixed Juice Mixed Juice Heating: Filter Cakekrishna sharmaNo ratings yet

- P A B C D M N: Conversion Between Radians and DegreesDocument5 pagesP A B C D M N: Conversion Between Radians and DegreeskumardavidNo ratings yet

- RefineryDocument14 pagesRefinerykrishna sharmaNo ratings yet

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Siemens MCCB Control Switches Price List PDFDocument104 pagesSiemens MCCB Control Switches Price List PDFkrishna sharmaNo ratings yet

- Separator Design MethodologyDocument19 pagesSeparator Design Methodologyromdhan88100% (1)

- Nptel Lecture Notes 2Document21 pagesNptel Lecture Notes 2balusappsNo ratings yet

- Selection of Liquid & Vapour SeparatorDocument33 pagesSelection of Liquid & Vapour SeparatorVismit BansalNo ratings yet

- Speciality Sugars Transform Meals Into Taste ExperiencesDocument21 pagesSpeciality Sugars Transform Meals Into Taste Experienceskrishna sharmaNo ratings yet

- Selection of Liquid & Vapour SeparatorDocument33 pagesSelection of Liquid & Vapour SeparatorVismit BansalNo ratings yet

- S. PobiDocument26 pagesS. Pobikrishna sharmaNo ratings yet

- Training Book - Hindi For ISO 14001Document10 pagesTraining Book - Hindi For ISO 14001krishna sharmaNo ratings yet

- Comparison of Design and Analysis of Tube Sheet Thickness by Using Uhx Code-2/comparison of Design and Analysis of Tube Sheet Thickness by Using Uhx Code-2 PDFDocument13 pagesComparison of Design and Analysis of Tube Sheet Thickness by Using Uhx Code-2/comparison of Design and Analysis of Tube Sheet Thickness by Using Uhx Code-2 PDFruponline1No ratings yet

- M.S. SundaramDocument21 pagesM.S. Sundaramkrishna sharmaNo ratings yet

- MR S. RanuDocument24 pagesMR S. Ranukrishna sharmaNo ratings yet

- GTP - 16 33 KV Xlpe Cable 3c X 95 SQMMDocument3 pagesGTP - 16 33 KV Xlpe Cable 3c X 95 SQMMraj_stuff006No ratings yet

- Reliance East West Pipeline Punj LoydDocument3 pagesReliance East West Pipeline Punj LoydPuneet Zaidu100% (1)

- Ceramkii WebDocument2 pagesCeramkii WebD01No ratings yet

- Bomba InspectionDocument30 pagesBomba InspectionAn-an Chan100% (1)

- Turbine ElsterDocument4 pagesTurbine Elsterpalotito_eNo ratings yet

- Sep Tank DesignDocument36 pagesSep Tank Designsrinivasakannan23No ratings yet

- Exp SrilankaDocument10 pagesExp SrilankaAnthony Kabuga100% (1)

- SVA Aximax 2HL 3698SF Made in USADocument3 pagesSVA Aximax 2HL 3698SF Made in USADhanus KodiNo ratings yet

- D789188CTDocument9 pagesD789188CTplvg2009No ratings yet

- PMMRR 1997 - Book PDFDocument113 pagesPMMRR 1997 - Book PDFwasita wadariNo ratings yet

- Full English-Gb9685-2008, April 12th China Food ContactDocument260 pagesFull English-Gb9685-2008, April 12th China Food ContactAlberto GiudiciNo ratings yet

- SAB120-151 Spare Parts 2015.05Document52 pagesSAB120-151 Spare Parts 2015.05Andrei Taranu100% (2)

- The Italian Restaurant Print 1Document6 pagesThe Italian Restaurant Print 1Leahu DanielNo ratings yet

- Ductless SPLIT SystemsDocument16 pagesDuctless SPLIT SystemstitomottaNo ratings yet

- SurfaceDrilling PDFDocument260 pagesSurfaceDrilling PDFVictor Hernan100% (3)

- Foreword: Lam Siew WahDocument68 pagesForeword: Lam Siew WahngthienyNo ratings yet

- Ca 450 en 1609Document2 pagesCa 450 en 1609Randolf WenholdNo ratings yet

- Strategic Planner Sales ResumeDocument8 pagesStrategic Planner Sales ResumeSushil GoyalNo ratings yet

- RADIOLINEDocument198 pagesRADIOLINERavenShieldXNo ratings yet

- Curwal cw50 ProbroDocument8 pagesCurwal cw50 ProbroMohammed RiyazNo ratings yet

- Sbakx 32Document11 pagesSbakx 32rer0427No ratings yet

- Ncrdme Conference Schedule: 27july-2018 (Friday)Document4 pagesNcrdme Conference Schedule: 27july-2018 (Friday)Ramsai ChigurupatiNo ratings yet

- Service Service Manual Manual: Onan Generator Set For MarineDocument204 pagesService Service Manual Manual: Onan Generator Set For MarinenajeebabdulkadarNo ratings yet

- Contoh Resume Terbaik 2Document2 pagesContoh Resume Terbaik 2Amin IqmalNo ratings yet

- ESTIMATING COSTSDocument36 pagesESTIMATING COSTSgovindsinghsolankiNo ratings yet

- LF End Suction Pump: A Grundfos CompanyDocument4 pagesLF End Suction Pump: A Grundfos CompanyDya WiNo ratings yet

- Polo Allstar LeafletDocument2 pagesPolo Allstar LeafletZaraki KenpachiNo ratings yet

- Dust Collector ValvesDocument8 pagesDust Collector ValvesAnonymous lswzqloNo ratings yet

- Holiday TestDocument4 pagesHoliday TestSaptarshi MandalNo ratings yet

- Summat IveDocument10 pagesSummat IveNorma Panares100% (1)