You might also like

- Income Taxation QuizzerDocument41 pagesIncome Taxation QuizzerMarriz Tan100% (4)

- Income Tax DeductionsDocument31 pagesIncome Tax DeductionsJane Tuazon50% (2)

- HQ05 - Capital Gains TaxationDocument10 pagesHQ05 - Capital Gains TaxationClarisaJoy Sy100% (3)

- TAX.2811 Deductions From Gross IncomeDocument10 pagesTAX.2811 Deductions From Gross IncomeMary Ann Del PradoNo ratings yet

- Documentary Stamp TaxDocument6 pagesDocumentary Stamp TaxchrizNo ratings yet

- Answer Midterm - Docx 1Document8 pagesAnswer Midterm - Docx 1Yolly DiazNo ratings yet

- TAX Assessment October 2020Document8 pagesTAX Assessment October 2020FuturamaramaNo ratings yet

- S C Test Bank Income TaxationDocument135 pagesS C Test Bank Income Taxationthenikkitr50% (6)

- UL Taxation: Introduction to Income, Final and Capital Gains TaxDocument7 pagesUL Taxation: Introduction to Income, Final and Capital Gains TaxJimmyChaoNo ratings yet

- Exam - Tax - 2019 - KeyDocument2 pagesExam - Tax - 2019 - KeyKenneth Bryan Tegerero Tegio0% (1)

- Income TaxDocument20 pagesIncome Taxjuliaysabellepepitoaguilar100% (1)

- Acco 4133 - Taxation: College of Accountancy and FinanceDocument10 pagesAcco 4133 - Taxation: College of Accountancy and FinanceNadi Hood100% (1)

- Taxation - Gross Income - Quizzer - 2018 - MayDocument5 pagesTaxation - Gross Income - Quizzer - 2018 - MayKenneth Bryan Tegerero TegioNo ratings yet

- Taxation of Individuals QuizzerDocument37 pagesTaxation of Individuals QuizzerCharry Ramos62% (13)

- Income TaxationDocument6 pagesIncome TaxationLove Lee Hallarsis Fabicon86% (7)

- Taxation Law ReviewDocument8 pagesTaxation Law ReviewShirliz Jane Benitez100% (2)

- Exclusion from gross incomeDocument11 pagesExclusion from gross incomeMychie Lynne MayugaNo ratings yet

- CH08 VAT On ImportationDocument35 pagesCH08 VAT On Importationwilma olivoNo ratings yet

- Quiz Tax OPTDocument5 pagesQuiz Tax OPTAnonymous 7HGskN0% (1)

- Compensation and Fringe Benefits TaxDocument10 pagesCompensation and Fringe Benefits TaxJane TuazonNo ratings yet

- Take Home Quiz Income TaxationDocument5 pagesTake Home Quiz Income TaxationMae Astoveza100% (3)

- CPAR Fringe Benefit TaxDocument5 pagesCPAR Fringe Benefit TaxNikki75% (4)

- HQ04 - Final Income TaxationDocument5 pagesHQ04 - Final Income TaxationJimmyChaoNo ratings yet

- TAX - LEAD BATCH 3 - Preweek 1 PDFDocument28 pagesTAX - LEAD BATCH 3 - Preweek 1 PDFMay Litt0% (1)

- Deductions From Gross IncomeDocument49 pagesDeductions From Gross IncomeRoronoa ZoroNo ratings yet

- MAPUA INSTITUTE OF TECHNOLOGY INTEGRATED TAX REVIEW COURSEDocument12 pagesMAPUA INSTITUTE OF TECHNOLOGY INTEGRATED TAX REVIEW COURSEBon DanaoNo ratings yet

- Gross IncomeDocument68 pagesGross IncomeNour Aira NaoNo ratings yet

- Income Tax For Corporation PDFDocument7 pagesIncome Tax For Corporation PDFNadi HoodNo ratings yet

- Tax CPAR Final Pre Board2Document5 pagesTax CPAR Final Pre Board2No Longer Existing67% (3)

- Rules on excise tax for cosmetic proceduresDocument8 pagesRules on excise tax for cosmetic proceduresCaroline Claire BaricNo ratings yet

- Answer Key Ch8Document12 pagesAnswer Key Ch8Zarah RoveroNo ratings yet

- DONORS TAX THEORY AND KEY CONCEPTSDocument6 pagesDONORS TAX THEORY AND KEY CONCEPTSMoises A. Almendares100% (1)

- Tax Remedies QuizzerDocument3 pagesTax Remedies QuizzerCharrie Grace Pablo29% (7)

- Midterm Exam IntaxDocument16 pagesMidterm Exam IntaxIyarna Yasra100% (1)

- Tax Finals Summative s02Document13 pagesTax Finals Summative s02Von Andrei MedinaNo ratings yet

- Deductions From Gross Income 2 1Document42 pagesDeductions From Gross Income 2 1Katherine EderosasNo ratings yet

- Reviewer in Income TaxDocument97 pagesReviewer in Income TaxBianca Jane KinatadkanNo ratings yet

- Deductions From Gross IncomeDocument30 pagesDeductions From Gross IncomeKatherine Ederosas50% (4)

- Taxation - Corporation - Quizzer - 2018Document4 pagesTaxation - Corporation - Quizzer - 2018Kenneth Bryan Tegerero Tegio100% (4)

- Taxation - Final ExamDocument4 pagesTaxation - Final ExamKenneth Bryan Tegerero Tegio100% (1)

- Tax - FBT and de MinimisDocument19 pagesTax - FBT and de Minimisryan rosalesNo ratings yet

- Intro To Consumption TaxesDocument50 pagesIntro To Consumption TaxesKheianne DaveighNo ratings yet

- CPA Review: Philippines Tax Filing RequirementsDocument10 pagesCPA Review: Philippines Tax Filing RequirementsYamate0% (1)

- Deductions From Gross Income Lesson 13Document72 pagesDeductions From Gross Income Lesson 13Mikaela SamonteNo ratings yet

- Exempt SalesDocument46 pagesExempt SalesKheianne DaveighNo ratings yet

- Additional Income Tax QuizzerDocument2 pagesAdditional Income Tax QuizzerJohn Brian D. Soriano100% (1)

- AC 3103 MOCK EXAM TIPSDocument14 pagesAC 3103 MOCK EXAM TIPSChristine NionesNo ratings yet

- Week 2 (Principles of Taxation - Part 2)Document48 pagesWeek 2 (Principles of Taxation - Part 2)Beef TestosteroneNo ratings yet

- Taxation PreweekDocument25 pagesTaxation Preweekschaffy100% (5)

- Estate Tax Gross Estate GuideDocument6 pagesEstate Tax Gross Estate GuideCharry Ramos67% (3)

- 1Document9 pages1James Diaz100% (2)

- Chapter 4 Sources of Income PDFDocument5 pagesChapter 4 Sources of Income PDFkimberly tenebroNo ratings yet

- Northern CPAR: Taxation - Fringe Benefit Taxation: Rex B. Banggawan, Cpa, MbaDocument7 pagesNorthern CPAR: Taxation - Fringe Benefit Taxation: Rex B. Banggawan, Cpa, MbaLouiseNo ratings yet

- FringeDocument7 pagesFringeJoyce Anne TilanNo ratings yet

- Module 3.1 Fringe Benefits and de Minimis BenefitsDocument4 pagesModule 3.1 Fringe Benefits and de Minimis BenefitsGabs SolivenNo ratings yet

- REO Fringe Benefit TaxDocument5 pagesREO Fringe Benefit TaxJohn Michael MateoNo ratings yet

- Additional Notes Fringe Benefit TaxDocument10 pagesAdditional Notes Fringe Benefit TaxAngela Nicole NobletaNo ratings yet

- Module 5 Fringe Benefit TaxDocument45 pagesModule 5 Fringe Benefit TaxAjey MendiolaNo ratings yet

- Tax Treatments of Fringe BenefitsDocument63 pagesTax Treatments of Fringe BenefitsAdmNo ratings yet

- Tax Treatments of Fringe BenefitsDocument14 pagesTax Treatments of Fringe BenefitsAdmNo ratings yet

- Tax Planning.: Dhruv Desai. Shriyans JainDocument13 pagesTax Planning.: Dhruv Desai. Shriyans JainShreyans JainNo ratings yet

- CCP5312 20211231Document1 pageCCP5312 20211231Ravi JoshiNo ratings yet

- Income Tax Treatment of Agricultural IncomeDocument9 pagesIncome Tax Treatment of Agricultural Incomeprabs2007No ratings yet

- Reliance HR Services: Report ViewerDocument1 pageReliance HR Services: Report ViewerBhavesh MishraNo ratings yet

- BAC Fee Schedule 1st January 2024Document1 pageBAC Fee Schedule 1st January 2024Fei SeanNo ratings yet

- Assigment - 3: Nama: Listi Maulida Saapitri NPM: 1111197034Document1 pageAssigment - 3: Nama: Listi Maulida Saapitri NPM: 1111197034Wanabakti SatriaNo ratings yet

- EY Tax Alert: Malaysian DevelopmentsDocument10 pagesEY Tax Alert: Malaysian DevelopmentsSirius StarNo ratings yet

- PDFDocument22 pagesPDFKarthik ShimogaNo ratings yet

- Register your bank details for payments under 40 charactersDocument1 pageRegister your bank details for payments under 40 charactersGampang GedeNo ratings yet

- CertificateDocument3 pagesCertificateMalik Jee100% (1)

- Ola BillDocument3 pagesOla BillMohit TanwarNo ratings yet

- Ms Kik Express Sleeper Class (SL) : Electronic Reserva On Slip (ERS)Document1 pageMs Kik Express Sleeper Class (SL) : Electronic Reserva On Slip (ERS)Gowtham LNo ratings yet

- Gmail - Your Thursday Morning Trip With UberDocument3 pagesGmail - Your Thursday Morning Trip With Uberbernard nezarlonNo ratings yet

- Credit CardDocument2 pagesCredit CardpauloNo ratings yet

- VAT Registration and Compliance RequirementsDocument34 pagesVAT Registration and Compliance RequirementsNatalie SerranoNo ratings yet

- Document TypeDocument1 pageDocument TypeAdam JurekNo ratings yet

- ITR 1 Excel Sheet To Download OnlyDocument6 pagesITR 1 Excel Sheet To Download OnlyRahul Kumar100% (1)

- Foreclosure LetterDocument3 pagesForeclosure LetterabinayaNo ratings yet

- Bank Reconciliation Process: Step 1. Adjusting The Balance Per BankDocument5 pagesBank Reconciliation Process: Step 1. Adjusting The Balance Per BankSulaimon AbiodunNo ratings yet

- ListDocument24 pagesListManav PtelNo ratings yet

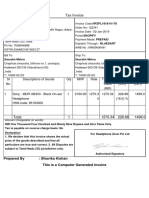

- Tax Invoice: SI No. Descriptions of Goods Qty MRP Rate Taxable Value (INR) Igst (INR) Amount (INR)Document1 pageTax Invoice: SI No. Descriptions of Goods Qty MRP Rate Taxable Value (INR) Igst (INR) Amount (INR)Saurabh MehraNo ratings yet

- Fees Summary - IICKLDocument1 pageFees Summary - IICKLZhess BugNo ratings yet

- Tax Invoice: Booking DetailsDocument2 pagesTax Invoice: Booking DetailsRajiv SinghNo ratings yet

- CFI Accounting FactsheetDocument1 pageCFI Accounting FactsheetPirvuNo ratings yet

- Atc 1 PDFDocument2 pagesAtc 1 PDFSatvik ManaktalaNo ratings yet

- Statement of Account BBVADocument7 pagesStatement of Account BBVAchistopher freundNo ratings yet

- 20201213-Statements-9476 - (1) - UnlockedDocument4 pages20201213-Statements-9476 - (1) - UnlockedHamza AzamNo ratings yet

- Tax Deduction at Source BasicsDocument25 pagesTax Deduction at Source BasicsdagliamitNo ratings yet

- Use black ink for Florida employer tax reportDocument3 pagesUse black ink for Florida employer tax reportjackNo ratings yet

- Case Digests Taxation Law - Philippine Landmark CasesDocument2 pagesCase Digests Taxation Law - Philippine Landmark CasesEmilee TerestaNo ratings yet