You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Customer Satisfaction Project ReportDocument75 pagesCustomer Satisfaction Project ReportSiddareddy Siddu84% (108)

- Customer Satisfaction Project ReportDocument75 pagesCustomer Satisfaction Project ReportSiddareddy Siddu84% (108)

- Customer Satisfaction Project ReportDocument75 pagesCustomer Satisfaction Project ReportSiddareddy Siddu84% (108)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- A Project Report On Direct TaxDocument53 pagesA Project Report On Direct Taxrani26oct84% (44)

- Pharmacist - ResumeDocument2 pagesPharmacist - Resumentambik21No ratings yet

- Case Study CommunicationDocument3 pagesCase Study CommunicationZahir FariqieNo ratings yet

- Swimlane Diagram Template - VPDDocument2 pagesSwimlane Diagram Template - VPDpradeepNo ratings yet

- Final Payroll Project Report1Document86 pagesFinal Payroll Project Report1pradeepNo ratings yet

- Patton KanbanDocument32 pagesPatton KanbanDipen Ashokkumar KadamNo ratings yet

- Copy2-Ramanand Professional (1) CV 2Document2 pagesCopy2-Ramanand Professional (1) CV 2pradeepNo ratings yet

- A Summer Internship Project Report OnDocument4 pagesA Summer Internship Project Report OnpradeepNo ratings yet

- Priyanka ChaudharyDocument3 pagesPriyanka ChaudharypradeepNo ratings yet

- W1 What Is Professional DevelopmentDocument21 pagesW1 What Is Professional DevelopmentjustKThingsNo ratings yet

- Think Like A FREAK (Abridgement)Document12 pagesThink Like A FREAK (Abridgement)Ron TurfordNo ratings yet

- Internship Report On Human Resource Management Practices On Prime Bank LimitedDocument49 pagesInternship Report On Human Resource Management Practices On Prime Bank LimitedÃñûshkâ SûmãñNo ratings yet

- Pantaloon Evolving HR Issues in Pantaloon Retail India Ltd. With Case StudyDocument69 pagesPantaloon Evolving HR Issues in Pantaloon Retail India Ltd. With Case StudyH. Phani Krishna Kant0% (1)

- Ains 21 Answers To The Questions in The Course Guide 6th EditionDocument6 pagesAins 21 Answers To The Questions in The Course Guide 6th Editioncrazymanu4No ratings yet

- Naveen Kumar Resume-2022Document4 pagesNaveen Kumar Resume-2022NavinNo ratings yet

- Compare Management's Classical and Behavioral TheoryDocument10 pagesCompare Management's Classical and Behavioral TheoryDilan A AlmousaNo ratings yet

- Ssa Ss 5 Fs NonfillableDocument2 pagesSsa Ss 5 Fs Nonfillableallende7No ratings yet

- Payment of Wages Act, 1936: E.L.L. AssignmentDocument7 pagesPayment of Wages Act, 1936: E.L.L. AssignmentAakanksha SinghNo ratings yet

- Measuring Turnover: Internal vs. External TurnoverDocument1 pageMeasuring Turnover: Internal vs. External TurnoverRoshan JhaNo ratings yet

- Thuyết trình TH True MilkDocument20 pagesThuyết trình TH True MilkNgọc HânNo ratings yet

- CAAT (Computer Assisted Auditing Technique) TestsDocument78 pagesCAAT (Computer Assisted Auditing Technique) TestsVanessaDulayAbejay100% (3)

- Application Letter & Job Interview 2Document13 pagesApplication Letter & Job Interview 2nurfadilla. mNo ratings yet

- Employee and Independent ContractorDocument14 pagesEmployee and Independent ContractorsmarikaNo ratings yet

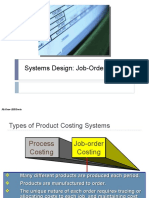

- Systems Design: Job-Order Costing: Mcgraw-Hill/IrwinDocument18 pagesSystems Design: Job-Order Costing: Mcgraw-Hill/IrwintowkirNo ratings yet

- Resume Writing Tips PDFDocument11 pagesResume Writing Tips PDFGiang Nguyễn TrườngNo ratings yet

- English Law Terminology-1Document23 pagesEnglish Law Terminology-1NOVAK9898No ratings yet

- Engineers India 5321780316Document234 pagesEngineers India 5321780316eepNo ratings yet

- PHP 50,000/month PHP 30,000/month Yes PHP 2,000: - ConformeDocument1 pagePHP 50,000/month PHP 30,000/month Yes PHP 2,000: - ConformeluckyNo ratings yet

- New Report of VolkaDocument32 pagesNew Report of VolkaMuhammad Imran100% (1)

- Construction Today September October 2013Document196 pagesConstruction Today September October 2013Martillo SaavNo ratings yet

- Advert - Marketing and Communications InternDocument3 pagesAdvert - Marketing and Communications Internangie_nimmoNo ratings yet

- Ongc Pension&mediDocument17 pagesOngc Pension&medidipti bhimNo ratings yet

- Chevron Regulatory Report Draft For Public CommentDocument115 pagesChevron Regulatory Report Draft For Public CommentKQED NewsNo ratings yet

- NO. Subject Page No. 1: Aero Based Control Systems Private LimitedDocument51 pagesNO. Subject Page No. 1: Aero Based Control Systems Private LimitedFarzanaNo ratings yet

- Application Guide For Ontario Human Capital Priorities StreamDocument38 pagesApplication Guide For Ontario Human Capital Priorities StreamHassan ZahrirNo ratings yet

- Do You Really Think We Are So Stupid 3PDocument6 pagesDo You Really Think We Are So Stupid 3PAngye Jhasbleidy Dominguez LeonNo ratings yet