You might also like

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Audit of IntangiblesDocument7 pagesAudit of IntangiblesAireese33% (3)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- How To Calculate A CorrelationDocument5 pagesHow To Calculate A CorrelationAireeseNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Cleaning ACDocument4 pagesCleaning ACAireeseNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Lesson 1 AP: Minimum Composition of The SFP and Some Audit NotesDocument14 pagesLesson 1 AP: Minimum Composition of The SFP and Some Audit NotesAireese0% (1)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- His Love Interest (The Jose Rizal)Document5 pagesHis Love Interest (The Jose Rizal)Aireese100% (1)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Resolution No. 11Document2 pagesResolution No. 11AireeseNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- What Are Sso Good Theis TopiDocument11 pagesWhat Are Sso Good Theis TopiAireeseNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Key Determinants of Capital Structure in Iran: 1.1 BackgroundDocument15 pagesKey Determinants of Capital Structure in Iran: 1.1 BackgroundAireeseNo ratings yet

- Amorphophallus Titanium: Titan ArumDocument4 pagesAmorphophallus Titanium: Titan ArumAireeseNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Learn About The Philippine CockatooDocument4 pagesLearn About The Philippine CockatooAireeseNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- MangkonoDocument3 pagesMangkonoAireeseNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- CH 07 WebDocument62 pagesCH 07 WebAireeseNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Siebenrockiella Leytensis: Brief SummaryDocument1 pageSiebenrockiella Leytensis: Brief SummaryAireeseNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Below Are Examples of Topics of Business Essay Topics To Help You Get StartedDocument25 pagesBelow Are Examples of Topics of Business Essay Topics To Help You Get StartedAireeseNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- HowACreditCardIsProcessed PDFDocument5 pagesHowACreditCardIsProcessed PDFKornelius SitepuNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- TermsDocument3 pagesTermsAmy GarrettNo ratings yet

- Business Restructuring by Brian Bergin, PWCDocument26 pagesBusiness Restructuring by Brian Bergin, PWCDublinChamber100% (1)

- I. Understanding The Client'S Business and Industry The ClientDocument2 pagesI. Understanding The Client'S Business and Industry The Clienthanna jeanNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- PNB Vs CirDocument8 pagesPNB Vs CirAnonymous VtsflLix1No ratings yet

- A Study On Barriers To E-Commerce Adoption in Vadodara District SMEsDocument15 pagesA Study On Barriers To E-Commerce Adoption in Vadodara District SMEsKushagra purohitNo ratings yet

- Understanding Monetary PolicyDocument26 pagesUnderstanding Monetary PolicyDr. Rakesh BhatiNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- International Trade Assignment 2Document22 pagesInternational Trade Assignment 2Gayatri PanjwaniNo ratings yet

- ConclusionDocument1 pageConclusionVirendra JhaNo ratings yet

- 300+ REAL TIME E-Banking Objective Questions & AnswersDocument31 pages300+ REAL TIME E-Banking Objective Questions & Answersbarun vishwakarmaNo ratings yet

- Draft Formate For Calculating Claimed Amount For Increase of Pennsions and Other Govt Related Benefits For PTCL EmployeesDocument5 pagesDraft Formate For Calculating Claimed Amount For Increase of Pennsions and Other Govt Related Benefits For PTCL EmployeesAdnanRasheedNo ratings yet

- Union Bank vs. Sps Tiu DigestDocument3 pagesUnion Bank vs. Sps Tiu DigestCaitlin KintanarNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- National Internal Revenue Code of The Philippines (NIRC)Document195 pagesNational Internal Revenue Code of The Philippines (NIRC)Jennybabe PetaNo ratings yet

- Consortium AdvancesDocument10 pagesConsortium Advancesmedhekar_renukaNo ratings yet

- Plan de EstudiosDocument27 pagesPlan de EstudiosRobertoNo ratings yet

- Annuity and Perpetuity HandoutsDocument3 pagesAnnuity and Perpetuity HandoutsKen AguilaNo ratings yet

- All Bank CEO List PDFDocument5 pagesAll Bank CEO List PDFKishanNo ratings yet

- JR 4 Axs BLBQVHH GL VDocument4 pagesJR 4 Axs BLBQVHH GL Vgaurav sehrawatNo ratings yet

- RatingsScale 2008 PDFDocument13 pagesRatingsScale 2008 PDFPradeep272No ratings yet

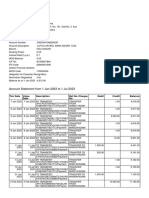

- Date Description Cheque No Debit Credit BalanceDocument4 pagesDate Description Cheque No Debit Credit BalanceRAHUL RAJARAMNo ratings yet

- 2016 2017 - Lembar Jawaban Ukk AkuntansiDocument79 pages2016 2017 - Lembar Jawaban Ukk Akuntansitomy andriyantoNo ratings yet

- RCBC Senate TestimonyDocument10 pagesRCBC Senate TestimonyMa FajardoNo ratings yet

- Opening Saving Account in HDFC BankDocument31 pagesOpening Saving Account in HDFC BankSukhchain AggarwalNo ratings yet

- Glackin 1Document64 pagesGlackin 1thestorydotieNo ratings yet

- Obligations Are ExtinguishedDocument24 pagesObligations Are ExtinguishedikayNo ratings yet

- Transferring Funds : International Personal BankDocument4 pagesTransferring Funds : International Personal BankGarbo BentleyNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Comparative Study of The Public Sector Amp Private Sector BankDocument67 pagesComparative Study of The Public Sector Amp Private Sector Bankvandana_daki3941No ratings yet

- Struktur Organisasi KC Cirebon Okt 2023Document13 pagesStruktur Organisasi KC Cirebon Okt 2023wulandariNo ratings yet

- Dude Wheres My RecoveryDocument19 pagesDude Wheres My RecoveryOccupyEconomics100% (1)

- E00a6 Non Performance Assets - HDFC BankDocument62 pagesE00a6 Non Performance Assets - HDFC BankwebstdsnrNo ratings yet

- The Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)From EverandThe Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Rating: 4 out of 5 stars4/5 (33)