You might also like

- GRC Technology Solutions BETA3.0Document28 pagesGRC Technology Solutions BETA3.0rominders100% (2)

- GlossoryDocument8 pagesGlossoryromindersNo ratings yet

- Accounting TermsDocument2 pagesAccounting TermsromindersNo ratings yet

- GOT Niagara Postcard Summer2018 RevisedDocument2 pagesGOT Niagara Postcard Summer2018 RevisedromindersNo ratings yet

- CFCS Candidate HandbookDocument21 pagesCFCS Candidate Handbookrominders0% (1)

- 10 Things Compliance Officers Need To Do inDocument11 pages10 Things Compliance Officers Need To Do inromindersNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Basics PDFDocument21 pagesBasics PDFSunil KumarNo ratings yet

- RESUME1Document2 pagesRESUME1sagar09100% (5)

- Terasaki FDP 2013Document40 pagesTerasaki FDP 2013MannyBaldonadoDeJesus100% (1)

- Assignment 1 - Vertical Alignment - SolutionsDocument6 pagesAssignment 1 - Vertical Alignment - SolutionsArmando Ramirez100% (1)

- 5 Teacher Induction Program - Module 5Document27 pages5 Teacher Induction Program - Module 5LAZABELLE BAGALLON0% (1)

- Highway Journal Feb 2023Document52 pagesHighway Journal Feb 2023ShaileshRastogiNo ratings yet

- BGP PDFDocument100 pagesBGP PDFJeya ChandranNo ratings yet

- Max9924 Max9927Document23 pagesMax9924 Max9927someone elseNo ratings yet

- Cable Schedule - Instrument - Surfin - Malanpur-R0Document3 pagesCable Schedule - Instrument - Surfin - Malanpur-R0arunpandey1686No ratings yet

- Trainer Manual Internal Quality AuditDocument32 pagesTrainer Manual Internal Quality AuditMuhammad Erwin Yamashita100% (5)

- Din 48204Document3 pagesDin 48204Thanh Dang100% (4)

- Finite State MachineDocument75 pagesFinite State Machinecall_asitNo ratings yet

- EceDocument75 pagesEcevignesh16vlsiNo ratings yet

- Debate Lesson PlanDocument3 pagesDebate Lesson Planapi-280689729No ratings yet

- M4110 Leakage Reactance InterfaceDocument2 pagesM4110 Leakage Reactance InterfaceGuru MishraNo ratings yet

- GeminiDocument397 pagesGeminiJohnnyJC86No ratings yet

- Concise Beam DemoDocument33 pagesConcise Beam DemoluciafmNo ratings yet

- Perbandingan Implementasi Smart City Di Indonesia: Studi Kasus: Perbandingan Smart People Di Kota Surabaya Dan Kota MalangDocument11 pagesPerbandingan Implementasi Smart City Di Indonesia: Studi Kasus: Perbandingan Smart People Di Kota Surabaya Dan Kota Malanglely ersilyaNo ratings yet

- JOB Performer: Q .1: What Is Permit?Document5 pagesJOB Performer: Q .1: What Is Permit?Shahid BhattiNo ratings yet

- Basic Concept of ProbabilityDocument12 pagesBasic Concept of Probability8wc9sncvpwNo ratings yet

- sp.1.3.3 Atoms,+Elements+&+Molecules+ActivityDocument4 pagessp.1.3.3 Atoms,+Elements+&+Molecules+ActivityBryaniNo ratings yet

- (Database Management Systems) : Biag, Marvin, B. BSIT - 202 September 6 2019Document7 pages(Database Management Systems) : Biag, Marvin, B. BSIT - 202 September 6 2019Marcos JeremyNo ratings yet

- PDFDocument1 pagePDFJaime Arroyo0% (1)

- Chapter 4 Seepage TheoriesDocument60 pagesChapter 4 Seepage Theoriesmimahmoud100% (1)

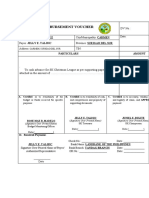

- Disbursement VoucherDocument7 pagesDisbursement VoucherDan MarkNo ratings yet

- Rewriting Snow White As A Powerful WomanDocument6 pagesRewriting Snow White As A Powerful WomanLaura RodriguezNo ratings yet

- Asugal Albi 4540Document2 pagesAsugal Albi 4540dyetex100% (1)

- Module 0-Course Orientation: Objectives OutlineDocument2 pagesModule 0-Course Orientation: Objectives OutlineEmmanuel CausonNo ratings yet

- Laser Mig - Hybrid - WeldinggDocument26 pagesLaser Mig - Hybrid - WeldinggFeratNo ratings yet

- Exam TimetableDocument16 pagesExam Timetablenyarko_eNo ratings yet