You might also like

- 4 Sem Bcom - Advanced Corporate AccountingDocument56 pages4 Sem Bcom - Advanced Corporate AccountingDipak Mahalik57% (7)

- Corporate RestructuringDocument20 pagesCorporate RestructuringHardik UdaniNo ratings yet

- Unit 1Document50 pagesUnit 1vaniphd3No ratings yet

- Chapter 3: Business Combination: Based On IFRS 3Document38 pagesChapter 3: Business Combination: Based On IFRS 3ሔርሞን ይድነቃቸውNo ratings yet

- Corporate Accounting IINotesDocument125 pagesCorporate Accounting IINotesPoonam Sunil Lalwani LalwaniNo ratings yet

- AmalagamationDocument3 pagesAmalagamationPavan ReddyNo ratings yet

- Amalgamation of Companies: Sushil KumarDocument49 pagesAmalgamation of Companies: Sushil KumarSundaramNo ratings yet

- Amalgamation of Companies (AS 14)Document22 pagesAmalgamation of Companies (AS 14)Sanaullah M SultanpurNo ratings yet

- UNIT-IV (Amalgamation of Companies) AmalgamationDocument4 pagesUNIT-IV (Amalgamation of Companies) AmalgamationCS & ITNo ratings yet

- Financial Accounting Theory (Sem V) PDFDocument4 pagesFinancial Accounting Theory (Sem V) PDFHarshal JainNo ratings yet

- Mergers and AcqDocument24 pagesMergers and AcqMaverick CardsNo ratings yet

- Amalgamation of Companies 2Document19 pagesAmalgamation of Companies 2Dipen Adhikari0% (1)

- Chapter - 2 Amalgamation of CompaniesDocument10 pagesChapter - 2 Amalgamation of CompanieshanumanthaiahgowdaNo ratings yet

- AmalgamationDocument3 pagesAmalgamationKdlr RRNo ratings yet

- Accounting FOR Amalgamation: Neha Garg Asst. Prof., CommerceDocument20 pagesAccounting FOR Amalgamation: Neha Garg Asst. Prof., CommerceNehaNo ratings yet

- Advanced Accounting SolvedDocument5 pagesAdvanced Accounting Solvedwaleedkhan567799No ratings yet

- Amalgamation and Absorption of CompaniesDocument89 pagesAmalgamation and Absorption of CompaniesHarshit Kumar GuptaNo ratings yet

- 14 Easy Way To Learn AmalgamationDocument3 pages14 Easy Way To Learn Amalgamationsudhy009100% (1)

- Amalgamantion and External ReconstructionDocument67 pagesAmalgamantion and External Reconstructionkhuranaamanpreet7gmailcomNo ratings yet

- Accounting For Amalgamation: What Is Amalgamation & Absorption?Document4 pagesAccounting For Amalgamation: What Is Amalgamation & Absorption?Bhuwan GuptaNo ratings yet

- Business Combinations : Ifrs 3Document45 pagesBusiness Combinations : Ifrs 3alemayehu100% (1)

- Amalgmation, Absorbtion, External ReconstructionDocument9 pagesAmalgmation, Absorbtion, External Reconstructionpijiyo78No ratings yet

- Wa0006.Document10 pagesWa0006.HemavathiNo ratings yet

- ACC208 CH 7 AmalgamationDocument23 pagesACC208 CH 7 AmalgamationSaja AlbarjesNo ratings yet

- AmalgamationDocument6 pagesAmalgamationbhavyaNo ratings yet

- Mergers and AcquisitionsDocument16 pagesMergers and Acquisitionsnaman somaniNo ratings yet

- CH-5 Business CombinationsDocument52 pagesCH-5 Business CombinationsRam KumarNo ratings yet

- Corporate Accounting I I FinalDocument82 pagesCorporate Accounting I I Finalthangarajbala123No ratings yet

- Aca Mergers and Acquitions of CompaniesDocument9 pagesAca Mergers and Acquitions of CompaniesRavichandraNo ratings yet

- WWW Yourarticlelibrary Com Accounting Amalgamation Amalgamation of Companie PDFDocument20 pagesWWW Yourarticlelibrary Com Accounting Amalgamation Amalgamation of Companie PDFMayur100% (1)

- Merger and Acquisition: Presented By: Nidhi Goswami Prashant Sharma Sunidhi Rathee Viprendra VikramDocument26 pagesMerger and Acquisition: Presented By: Nidhi Goswami Prashant Sharma Sunidhi Rathee Viprendra VikramgonidhiNo ratings yet

- Mergers & Acquisitions and Financial RestructuringDocument30 pagesMergers & Acquisitions and Financial Restructuringloving_girl165712No ratings yet

- Course: Subject: Lesson: Author's Name: College: Reviewer's NameDocument43 pagesCourse: Subject: Lesson: Author's Name: College: Reviewer's NameChew96No ratings yet

- CH 2 - Group Financial StatmentDocument47 pagesCH 2 - Group Financial StatmentWedaje AlemayehuNo ratings yet

- Financial Accounting Sem 4Document15 pagesFinancial Accounting Sem 4Siddharth SagarNo ratings yet

- Financial Accounting Sem 4 - CompressedDocument15 pagesFinancial Accounting Sem 4 - CompressedSiddharth SagarNo ratings yet

- MZ-Chapter Four BC-STDocument93 pagesMZ-Chapter Four BC-STfeyisab409No ratings yet

- Corporate RestructuringDocument12 pagesCorporate RestructuringDinesh kumar JenaNo ratings yet

- Lecture NotesDocument7 pagesLecture Noteskaren perrerasNo ratings yet

- Amalgamation of CompaniesDocument8 pagesAmalgamation of CompaniesVikram NaniNo ratings yet

- Company Secretataryship Training ProjectDocument17 pagesCompany Secretataryship Training ProjectPragati DixitNo ratings yet

- Amalgmation, Absorbtion, External ReconstructionDocument12 pagesAmalgmation, Absorbtion, External Reconstructionpijiyo78No ratings yet

- Chapter - 1: Meaning and DefinitionDocument12 pagesChapter - 1: Meaning and DefinitionShilpa S RaoNo ratings yet

- Group Accounts - Cashflow Statement-1Document19 pagesGroup Accounts - Cashflow Statement-1antony omondiNo ratings yet

- Chapter-2 Mergers and AcquisitionsDocument33 pagesChapter-2 Mergers and AcquisitionsMihir KeniaNo ratings yet

- Reviewer BUSINESS COMBINATIONDocument50 pagesReviewer BUSINESS COMBINATIONRamos JovelNo ratings yet

- Accounting Viva Question & AnsDocument11 pagesAccounting Viva Question & AnsSakib Ahmed AnikNo ratings yet

- Amalgamation of CompaniesDocument46 pagesAmalgamation of CompaniesRoyal funNo ratings yet

- Amalgamation of CompaniesDocument22 pagesAmalgamation of CompaniesSmit Shah0% (1)

- Unit: I Lesson: 1 Amalgamation and External ReconstructionDocument43 pagesUnit: I Lesson: 1 Amalgamation and External ReconstructionVandana SharmaNo ratings yet

- AmalgamationDocument48 pagesAmalgamationJaTinGupTa100% (2)

- MRGR AcqnDocument60 pagesMRGR AcqnMominul Hoq100% (1)

- New Microsoft Word DocumentDocument3 pagesNew Microsoft Word Documentishagoyal595160100% (1)

- Mergersand AcquisitionsDocument46 pagesMergersand AcquisitionsNur Batrisyia BalqisNo ratings yet

- Corporate RestructuringDocument40 pagesCorporate RestructuringSarita ThakurNo ratings yet

- Sem V Amalgamation - & - AbsorptionDocument3 pagesSem V Amalgamation - & - AbsorptionAnita SoniNo ratings yet

- CA Final Course Paper 2 Strategic Financial Management Chapter 13 CA. Biharilal DeoraDocument79 pagesCA Final Course Paper 2 Strategic Financial Management Chapter 13 CA. Biharilal DeoraPiyush KulkarniNo ratings yet

- Amalgamation Absorption ReconstrctionDocument4 pagesAmalgamation Absorption ReconstrctionDivyaNo ratings yet

- Amalgamation of CompaniesDocument3 pagesAmalgamation of CompaniessandeepNo ratings yet

- Intermediate Accounting 2: a QuickStudy Digital Reference GuideFrom EverandIntermediate Accounting 2: a QuickStudy Digital Reference GuideNo ratings yet

- Throughput Accounting and The Theory of ConstraintsDocument8 pagesThroughput Accounting and The Theory of ConstraintsMd AzimNo ratings yet

- What Is Transfer Pricing?Document2 pagesWhat Is Transfer Pricing?Md AzimNo ratings yet

- Return On Investment: Example of The ROI Formula CalculationDocument3 pagesReturn On Investment: Example of The ROI Formula CalculationMd Azim100% (1)

- Method of Predicting Corporate FailuresDocument1 pageMethod of Predicting Corporate FailuresMd AzimNo ratings yet

- Problems of Target CostingDocument2 pagesProblems of Target CostingMd AzimNo ratings yet

- How To Know Fraud in AdvanceDocument6 pagesHow To Know Fraud in AdvanceMd AzimNo ratings yet

- HeteroscedasticityDocument2 pagesHeteroscedasticityMd AzimNo ratings yet

- Probability and Statistics: To P, or Not To P?: Module Leader: DR James AbdeyDocument2 pagesProbability and Statistics: To P, or Not To P?: Module Leader: DR James AbdeyMd AzimNo ratings yet

- Probability and Statistics: To P, or Not To P?: Module Leader: DR James AbdeyDocument2 pagesProbability and Statistics: To P, or Not To P?: Module Leader: DR James AbdeyMd AzimNo ratings yet

- Accounting For Long Term AssetsDocument8 pagesAccounting For Long Term AssetsMd AzimNo ratings yet

- Probability and Statistics: To P, or Not To P?: Module Leader: DR James AbdeyDocument2 pagesProbability and Statistics: To P, or Not To P?: Module Leader: DR James AbdeyMd AzimNo ratings yet

- Probability and Statistics: To P, or Not To P?: Module Leader: DR James AbdeyDocument4 pagesProbability and Statistics: To P, or Not To P?: Module Leader: DR James AbdeyMd AzimNo ratings yet

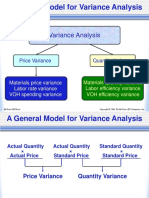

- Standard Costing and Variance AnalysisDocument11 pagesStandard Costing and Variance AnalysisMd AzimNo ratings yet

- Between Population: Difference MeansDocument2 pagesBetween Population: Difference MeansMd AzimNo ratings yet

- Probability and Statistics: To P, or Not To P?: Module Leader: DR James AbdeyDocument2 pagesProbability and Statistics: To P, or Not To P?: Module Leader: DR James AbdeyMd AzimNo ratings yet

- Deductive Reasoning Vs Inductive ReasoningDocument2 pagesDeductive Reasoning Vs Inductive ReasoningMd AzimNo ratings yet

- Probit Model: Conceptual FrameworkDocument1 pageProbit Model: Conceptual FrameworkMd AzimNo ratings yet

- Artificial Neural Network Model For Business Failure Prediction of Distressed Firms in Colombo Stock Exchanged - Sujeewa - 2014 PDFDocument18 pagesArtificial Neural Network Model For Business Failure Prediction of Distressed Firms in Colombo Stock Exchanged - Sujeewa - 2014 PDFMd AzimNo ratings yet

- Types of RANDOM SAMPLINGDocument2 pagesTypes of RANDOM SAMPLINGMd AzimNo ratings yet

- Accountability of Accounting StakeholdersDocument7 pagesAccountability of Accounting StakeholdersMd AzimNo ratings yet

- Chapter - Goodwill ValuationDocument6 pagesChapter - Goodwill ValuationMd AzimNo ratings yet

- (Week 2) Preliminary Analytical ProcedureDocument56 pages(Week 2) Preliminary Analytical ProcedureJonathan EdricNo ratings yet

- Study Material 9032Document29 pagesStudy Material 9032Md. Amran HossainNo ratings yet

- 2010 - Rosly - Shariah Parameter ReconsideredDocument19 pages2010 - Rosly - Shariah Parameter ReconsideredyuwonliloNo ratings yet

- Peer Reviewed - International Journal Vol-5, Issue-3, 2021 (IJEBAR)Document14 pagesPeer Reviewed - International Journal Vol-5, Issue-3, 2021 (IJEBAR)raiso fahriNo ratings yet

- Sarmiento - Prefinal Accounting ActivityDocument11 pagesSarmiento - Prefinal Accounting ActivityNicole SarmientoNo ratings yet

- Operations and Supply Chain ManagementDocument22 pagesOperations and Supply Chain ManagementPranali NagtilakNo ratings yet

- FinancialStatement 2020 (Q3)Document307 pagesFinancialStatement 2020 (Q3)Tonga ProjectNo ratings yet

- Orascom Construction PLC Corporate Presentation September 2022Document27 pagesOrascom Construction PLC Corporate Presentation September 2022Mira HoutNo ratings yet

- MCom CBCS Syllabus and Course Structure 2015 16 1Document50 pagesMCom CBCS Syllabus and Course Structure 2015 16 1Ganesh KotteNo ratings yet

- FIN 286 - Valuation - G TwiteDocument7 pagesFIN 286 - Valuation - G TwiteVasileNo ratings yet

- How Does A Holding Company WorkDocument6 pagesHow Does A Holding Company WorkDenardConwiBesa100% (2)

- Fabm2 Module 3Document18 pagesFabm2 Module 3Rea Mariz Jordan50% (2)

- Assignment FPADocument5 pagesAssignment FPAsuwilanji nachilombeNo ratings yet

- Income Statement Balance Sheet Cash Flow Ratios FCFF Eva & Roic News Analysis 1 News Analysis 2Document9 pagesIncome Statement Balance Sheet Cash Flow Ratios FCFF Eva & Roic News Analysis 1 News Analysis 2ramarao1981No ratings yet

- A. Calculate Watkins's Value of OperationsDocument20 pagesA. Calculate Watkins's Value of OperationsNarmeen Khan100% (1)

- GROUP ASSIGNMENT - 7-ELEVEN COMPANY - PDFDocument17 pagesGROUP ASSIGNMENT - 7-ELEVEN COMPANY - PDFNurul AzlinNo ratings yet

- Ca Foundation Accounts Paper Dec23Document11 pagesCa Foundation Accounts Paper Dec23aagarwal786riteshNo ratings yet

- Chapter 1 - FMDocument23 pagesChapter 1 - FMYoutube OnlyNo ratings yet

- Problem - No.1 Amalgamation in The Nature of Purchase - Net Asset Method Without Statutory Reserve)Document6 pagesProblem - No.1 Amalgamation in The Nature of Purchase - Net Asset Method Without Statutory Reserve)Siva SankariNo ratings yet

- FD Practice QuestionsDocument5 pagesFD Practice QuestionsYashNo ratings yet

- First Yacht ProjectDocument20 pagesFirst Yacht ProjectRaja HindustaniNo ratings yet

- IAS 16 and IAS 38Document84 pagesIAS 16 and IAS 38Danu DorinaNo ratings yet

- Merchandising Bus Prub Periodic MethodDocument2 pagesMerchandising Bus Prub Periodic MethodChristopher Keith BernidoNo ratings yet

- FIN 515 Midterm ExamDocument4 pagesFIN 515 Midterm ExamDeVryHelpNo ratings yet

- Correction of Errors PDFDocument7 pagesCorrection of Errors PDFKylaSalvador0% (2)

- IGCSE Business Analysis Past PaperDocument4 pagesIGCSE Business Analysis Past PaperPasta SempaNo ratings yet

- ABC and XYZ - AnswerDocument6 pagesABC and XYZ - AnswerMohammad El HajjNo ratings yet

- MBA Project On Working CapitalDocument57 pagesMBA Project On Working CapitalVijai PillarsettiNo ratings yet

- Preface To IFRS StandardsDocument14 pagesPreface To IFRS StandardsQBO CourseNo ratings yet

- Auditing Cup - 19 Rmyc Answer Key Elimination Round EasyDocument14 pagesAuditing Cup - 19 Rmyc Answer Key Elimination Round EasyFarhana GuiandalNo ratings yet