You might also like

- Retirement Planning WorkbookDocument8 pagesRetirement Planning Workbooktwankfanny100% (3)

- Healing Grabovoi NumberDocument54 pagesHealing Grabovoi Numberabdulrohman yahya81% (103)

- Personal Budget TemplateDocument6 pagesPersonal Budget TemplateMrsRainesNo ratings yet

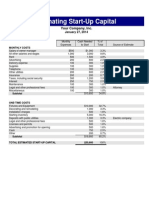

- Estimating Start-Up Capital: Your Company, IncDocument1 pageEstimating Start-Up Capital: Your Company, IncnightclownNo ratings yet

- Manufacturing Overhead Budget GuideDocument16 pagesManufacturing Overhead Budget GuideRonak Singh67% (3)

- Ec Creating Energy Circles PDFDocument10 pagesEc Creating Energy Circles PDFMaaman Abdulrahman Yahya100% (1)

- Business Application System Development, Acquisition, Implementation, and MaintenanceDocument111 pagesBusiness Application System Development, Acquisition, Implementation, and MaintenanceSudhir PatilNo ratings yet

- Crypto Mining Project Cost AnalysisDocument3 pagesCrypto Mining Project Cost AnalysisifyNo ratings yet

- Food and Beverage Revenue ForecastDocument10 pagesFood and Beverage Revenue ForecastJose BarajasNo ratings yet

- Month End Close ChecklistDocument10 pagesMonth End Close ChecklistKv kNo ratings yet

- Business Case Spreadsheet TemplateDocument37 pagesBusiness Case Spreadsheet TemplateEmmanuel Juárez Díaz100% (1)

- A Diamond Spirit Reading: Hans DecozDocument9 pagesA Diamond Spirit Reading: Hans Decozabdulrohman yahyaNo ratings yet

- A Diamond Spirit Reading: Hans DecozDocument9 pagesA Diamond Spirit Reading: Hans Decozabdulrohman yahyaNo ratings yet

- A Few Kat Thoughts About Job-Seeking: My ReasoningDocument8 pagesA Few Kat Thoughts About Job-Seeking: My Reasoningabdulrohman yahyaNo ratings yet

- Format of Financial Statements Under The Revised Schedule VIDocument97 pagesFormat of Financial Statements Under The Revised Schedule VIDebadarshi RoyNo ratings yet

- Monthly Cash Flow TemplateDocument33 pagesMonthly Cash Flow TemplateShah JeeNo ratings yet

- Financial ModelDocument83 pagesFinancial Modelapi-376449680% (5)

- Monitor cash flow with forecastsDocument2 pagesMonitor cash flow with forecastswresfrNo ratings yet

- Financial Markets Quiz 1Document8 pagesFinancial Markets Quiz 1Aingeal DiabhalNo ratings yet

- Cash Flow Small BusinessDocument39 pagesCash Flow Small Businessmariusdr84No ratings yet

- Annual ReportDocument193 pagesAnnual ReportShafali R ChandranNo ratings yet

- Business Case TemplateDocument2 pagesBusiness Case Templatedutty1-1No ratings yet

- Personlig BudgetDocument6 pagesPersonlig BudgetAnn SundkvistNo ratings yet

- Sunera Technologies Pvt. LTD.: Standard Operating Procedure TemplateDocument14 pagesSunera Technologies Pvt. LTD.: Standard Operating Procedure Templatesastrylanka_1980No ratings yet

- Simple Startup Budgeting TemplateDocument21 pagesSimple Startup Budgeting TemplateAni Nalitayui LifityaNo ratings yet

- Cost-Benefit Analysis TemplateDocument4 pagesCost-Benefit Analysis TemplateGeorgios PalaiologosNo ratings yet

- HR Cost of Hiring CalculatorDocument2 pagesHR Cost of Hiring Calculatornandex777No ratings yet

- Excel Budget Template: Project Start Date Scroll To Week #Document5 pagesExcel Budget Template: Project Start Date Scroll To Week #rajeev kaushalNo ratings yet

- Mindfulness With Breathing & Four Elements MeditationDocument98 pagesMindfulness With Breathing & Four Elements Meditationeressendil100% (1)

- Investment TrackerDocument8 pagesInvestment TrackerjanuarNo ratings yet

- Introduction To Indian Financial SystemDocument31 pagesIntroduction To Indian Financial SystemManoher Reddy100% (2)

- Annual Budget Development Summary: Project Name Project Manager Project AdvisorDocument9 pagesAnnual Budget Development Summary: Project Name Project Manager Project AdvisorthanglcNo ratings yet

- Cashflow Forecast Actual SampleDocument33 pagesCashflow Forecast Actual SampleAchanNo ratings yet

- Financial Modeling - PUNE Financial ModelingDocument1 pageFinancial Modeling - PUNE Financial ModelingBHARAT PRAKASH MAHANTNo ratings yet

- Action Item Tracking TemplateDocument3 pagesAction Item Tracking TemplateOzu HedwigNo ratings yet

- Financial Modelling CVDocument3 pagesFinancial Modelling CVGanapathiraju SravaniNo ratings yet

- 401K PlannerDocument3 pages401K Plannertf2025No ratings yet

- Analyzing The Budgeting and Budgetary Control Process Followed at Bharat Electronics Limited, GhaziabadDocument59 pagesAnalyzing The Budgeting and Budgetary Control Process Followed at Bharat Electronics Limited, GhaziabadMustafa RezaieNo ratings yet

- Management Accounting SampleDocument25 pagesManagement Accounting SampleEdward Baffoe100% (1)

- Financial ModellingDocument12 pagesFinancial Modellingalokroutray40% (5)

- IM&C GUANO PROJECT CASH FLOWDocument1 pageIM&C GUANO PROJECT CASH FLOWrajvakNo ratings yet

- An Introduction To BacktestingDocument20 pagesAn Introduction To BacktestingwhitecrescentNo ratings yet

- Ultimate Financial ModelDocument36 pagesUltimate Financial ModelTom BookNo ratings yet

- Bad Debts ProcedureDocument3 pagesBad Debts ProcedureCM_NguyenNo ratings yet

- Product Cost AccountingDocument76 pagesProduct Cost Accountingabdulrohman yahya100% (1)

- Investment TrackerDocument9 pagesInvestment TrackerRick MischkaNo ratings yet

- David SMCC16ge Ppt06Document52 pagesDavid SMCC16ge Ppt06JoannaGañaNo ratings yet

- Yasin Wal Asma' IdrisiyahDocument10 pagesYasin Wal Asma' Idrisiyahabdulrohman yahya100% (3)

- 07 P3M3 Self Assess ProjectDocument22 pages07 P3M3 Self Assess ProjectSuhail IqbalNo ratings yet

- Balance Sheet: For Year Ending June 30, 2008Document3 pagesBalance Sheet: For Year Ending June 30, 2008arazeqNo ratings yet

- FIU Audit Finds Need to Improve Receivables CollectionDocument18 pagesFIU Audit Finds Need to Improve Receivables CollectionnaniappoNo ratings yet

- 01 - Principles of FinanceDocument50 pages01 - Principles of FinanceBagusranu Wahyudi PutraNo ratings yet

- Start Your Business Financial PlanDocument11 pagesStart Your Business Financial PlanEvert TrochNo ratings yet

- Excel TemplateDocument48 pagesExcel TemplateigfhlkasNo ratings yet

- Bedroom Expansion Cost Dashboard Tracks Budget vs Actual Under $2KDocument4 pagesBedroom Expansion Cost Dashboard Tracks Budget vs Actual Under $2KRioChristianGultomNo ratings yet

- Excel SampleDocument8 pagesExcel SampleVõ Văn PhúcNo ratings yet

- CaseDocument194 pagesCasevishnu100% (1)

- Exercise 1 (Skyline University College)Document6 pagesExercise 1 (Skyline University College)Salman SajidNo ratings yet

- Budget Memo 2015 PDFDocument2 pagesBudget Memo 2015 PDFDominic HuniNo ratings yet

- Best Answer 3Document14 pagesBest Answer 3Chelsi Christine TenorioNo ratings yet

- SRS TemplateDocument13 pagesSRS TemplateEverest WalugembeNo ratings yet

- Advanced Finacial ModellingDocument1 pageAdvanced Finacial ModellingLifeis BeautyfulNo ratings yet

- Project PlanningDocument20 pagesProject PlanningBlessieNo ratings yet

- Holding CompanyDocument5 pagesHolding CompanySADIANo ratings yet

- AutoCount Accounting User Manual (Reduse) PDFDocument243 pagesAutoCount Accounting User Manual (Reduse) PDFindartoimams100% (1)

- Cba ExampleDocument4 pagesCba Examplelaxave8817No ratings yet

- Capitallization Table Template: Strictly ConfidentialDocument3 pagesCapitallization Table Template: Strictly Confidentialsh munnaNo ratings yet

- Corporate Budget Memo No. 39Document95 pagesCorporate Budget Memo No. 39mcla28No ratings yet

- 1yr Cash FlowDocument1 page1yr Cash FlowShrikant KajaleNo ratings yet

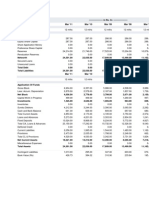

- Projected 5 Year Balance Sheet: Year 1 Year 2 Year 3 Year 4 Current AssetsDocument4 pagesProjected 5 Year Balance Sheet: Year 1 Year 2 Year 3 Year 4 Current AssetsHarkamal singhNo ratings yet

- 3-Year Cash Flow Statement: User To Complete Non-Shaded Fields, OnlyDocument5 pages3-Year Cash Flow Statement: User To Complete Non-Shaded Fields, OnlySabeoNo ratings yet

- Cash Flow Statement Template: User To Complete Non-Shaded Fields, OnlyDocument4 pagesCash Flow Statement Template: User To Complete Non-Shaded Fields, OnlyGomv ConsNo ratings yet

- Cash flow statement templateDocument5 pagesCash flow statement templateCarloNo ratings yet

- Contoh Part Daily SJDocument8 pagesContoh Part Daily SJabdulrohman yahyaNo ratings yet

- Peraturan Direktur Jenderal Pajak Nomor 25.PJ - .2018 EnglishDocument18 pagesPeraturan Direktur Jenderal Pajak Nomor 25.PJ - .2018 EnglishMaria EkaNo ratings yet

- Future of Skills 2019: Anticipating What's Next For Your BusinessDocument38 pagesFuture of Skills 2019: Anticipating What's Next For Your BusinesssuryaNo ratings yet

- Peraturan Direktur Jenderal Pajak Nomor 25.PJ - .2018 EnglishDocument18 pagesPeraturan Direktur Jenderal Pajak Nomor 25.PJ - .2018 EnglishMaria EkaNo ratings yet

- Breatheology Ebook EnglishDocument269 pagesBreatheology Ebook EnglishDorinNo ratings yet

- SPK Rumus TerbilangDocument2 pagesSPK Rumus Terbilangabdulrohman yahyaNo ratings yet

- Cost Sheet FormatDocument9 pagesCost Sheet Formatabdulrohman yahyaNo ratings yet

- MudraDocument2 pagesMudraabdulrohman yahyaNo ratings yet

- Yasin ArobDocument8 pagesYasin Arobabdulrohman yahya100% (1)

- DB Vs DC ComparisonDocument7 pagesDB Vs DC ComparisonNadeemUPLNo ratings yet

- Literature ReviewDocument2 pagesLiterature Reviewvishal9008252539No ratings yet

- Economic Value AddedDocument3 pagesEconomic Value Addedsangya01No ratings yet

- Railway Rates in Re 032634 MBPDocument358 pagesRailway Rates in Re 032634 MBPdegiuseppeNo ratings yet

- BLUE DART EXPRESS DCF VALUATIONDocument6 pagesBLUE DART EXPRESS DCF VALUATIONRahulTiwariNo ratings yet

- Jeda ConsDocument2 pagesJeda ConsNathan ChinhondoNo ratings yet

- Laboratory and Precious Metal Refineries v4Document12 pagesLaboratory and Precious Metal Refineries v4Amb B. R. PersadNo ratings yet

- QAFD Project SolverDocument5 pagesQAFD Project SolverUJJWALNo ratings yet

- Chapter 2Document43 pagesChapter 2Truely MaleNo ratings yet

- Personal Finance CH 3 NotesDocument2 pagesPersonal Finance CH 3 NotesJohn RammNo ratings yet

- Faj v72 n6 3Document18 pagesFaj v72 n6 3VuNo ratings yet

- Stated Objective: Dow Jones Stoxx Global 1800 IndexDocument2 pagesStated Objective: Dow Jones Stoxx Global 1800 IndexMutimbaNo ratings yet

- 10.chapter 1 (Introduction To Investments) PDFDocument41 pages10.chapter 1 (Introduction To Investments) PDFEswari Devi100% (1)

- Balance Sheet of InfosysDocument5 pagesBalance Sheet of InfosysLincy SubinNo ratings yet

- Introduction of India InfolineDocument79 pagesIntroduction of India InfolineArvind Mahandhwal100% (1)

- Chapter 1: Introduction To International BankingDocument45 pagesChapter 1: Introduction To International BankingJagrataNo ratings yet

- Exchange Rate Policy and Modelling in IndiaDocument117 pagesExchange Rate Policy and Modelling in IndiaArjun SriHariNo ratings yet

- ALFI and ABBL Guidelines and Recommendations For Depositaries Safekeeping of Other AssetsDocument62 pagesALFI and ABBL Guidelines and Recommendations For Depositaries Safekeeping of Other AssetsludivineNo ratings yet

- CAT Exam Practice Paper-II Question Bank on PercentagesDocument14 pagesCAT Exam Practice Paper-II Question Bank on PercentagesShubhamAuspiciosoGothwalNo ratings yet

- AFA QuizDocument15 pagesAFA QuizNoelia Mc DonaldNo ratings yet

- Final All Important Question of Mba IV Sem 2023Document11 pagesFinal All Important Question of Mba IV Sem 2023Arjun vermaNo ratings yet

- Business Ethics Case AnalysisDocument10 pagesBusiness Ethics Case AnalysisMarielle Taryao Padilla50% (2)

- Investleaf - MarketingDocument4 pagesInvestleaf - MarketingPushpak Reddy GattupalliNo ratings yet

- NBMCW March 2011Document252 pagesNBMCW March 2011Sampath SundaramNo ratings yet