You might also like

- Chapter 5Document26 pagesChapter 5Reese Parker33% (3)

- Chap 009Document51 pagesChap 009kmillatNo ratings yet

- C15.0021 Money, Banking, and Financial Markets: Professor A. Sinan Cebenoyan NYU-Stern-FinanceDocument6 pagesC15.0021 Money, Banking, and Financial Markets: Professor A. Sinan Cebenoyan NYU-Stern-FinanceSunil SunitaNo ratings yet

- Econ 304 HW 2Document8 pagesEcon 304 HW 2Tedjo Ardyandaru ImardjokoNo ratings yet

- Alorica Employee Handbook GuideDocument2 pagesAlorica Employee Handbook Guidejd stud0% (1)

- Young Men Are Still Better Off Than Young WomenDocument7 pagesYoung Men Are Still Better Off Than Young WomenLegal MomentumNo ratings yet

- Chapter 7 Case - Valuation Ratios in The Restaurant IndustryDocument2 pagesChapter 7 Case - Valuation Ratios in The Restaurant IndustrySarah Ihugo40% (5)

- STEM OPT Ext 2020 WorkshopDocument55 pagesSTEM OPT Ext 2020 WorkshopLiren YinNo ratings yet

- Henri BoulangerieDocument7 pagesHenri BoulangerievietNo ratings yet

- ANALYZE: Understanding Amortization: Part I: Amortization BasicsDocument4 pagesANALYZE: Understanding Amortization: Part I: Amortization BasicsJacob Orr0% (3)

- EULA IV Report First EditionDocument11 pagesEULA IV Report First EditionMelissa JordanNo ratings yet

- Case Presentation - Woodland Furniture LTDDocument16 pagesCase Presentation - Woodland Furniture LTDLucksonNo ratings yet

- SEVP Special Report: STEM OPT FAQsDocument5 pagesSEVP Special Report: STEM OPT FAQsVineethNo ratings yet

- PSC Upasachib 3rdpaperDocument11 pagesPSC Upasachib 3rdpaperbikram_068No ratings yet

- AEO - LBO Scenario #1a, Case 1 OverviewDocument4 pagesAEO - LBO Scenario #1a, Case 1 Overviewmilken466No ratings yet

- Role of the Federal Reserve ExplainedDocument2 pagesRole of the Federal Reserve ExplainedFUD Apple100% (1)

- Santa Barbara County COVID-19 Impact ReportDocument78 pagesSanta Barbara County COVID-19 Impact ReportBrooke TaylorNo ratings yet

- Ps 1Document3 pagesPs 1Anonymous mX3YrTLnSZ0% (2)

- ADM3346 Fall 2019 Assignment 9 Revised Nov 22Document2 pagesADM3346 Fall 2019 Assignment 9 Revised Nov 22Sam Fish100% (1)

- Glo-Stick, Inc.: Financial Statement Investigation A02-04-2015Document6 pagesGlo-Stick, Inc.: Financial Statement Investigation A02-04-2015碧莹成No ratings yet

- Cruz2007 Chapter3 SM FinalDocument20 pagesCruz2007 Chapter3 SM Finalasd50% (4)

- Next Level Tax Course: The only book a newbie needs for a foundation of the tax industryFrom EverandNext Level Tax Course: The only book a newbie needs for a foundation of the tax industryNo ratings yet

- Chapter 18 SolutionsDocument38 pagesChapter 18 SolutionsMichael Cox50% (2)

- Chapter 2 Review of Accounting, Financial Statements, TaxesDocument25 pagesChapter 2 Review of Accounting, Financial Statements, TaxesRohit SinghaniaNo ratings yet

- Practical Financial Management Chapter 2 SolManDocument25 pagesPractical Financial Management Chapter 2 SolManMichelle de Guzman100% (1)

- US Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesFrom EverandUS Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesNo ratings yet

- Module 03 Income Tax Concepts RevisedDocument20 pagesModule 03 Income Tax Concepts RevisedArianne Fortuna AugustoNo ratings yet

- TIF Problems 11 21 2019 PDFDocument360 pagesTIF Problems 11 21 2019 PDFomar mcintoshNo ratings yet

- Dfi 201 Lec Three Managing Taxes Teaching NotesDocument14 pagesDfi 201 Lec Three Managing Taxes Teaching Notesraina mattNo ratings yet

- 0.3 Module 03 - Income Tax ConceptsDocument18 pages0.3 Module 03 - Income Tax ConceptsDawn QuimatNo ratings yet

- Tax Savings Strategies for Small Businesses: A Comprehensive Guide For 2024From EverandTax Savings Strategies for Small Businesses: A Comprehensive Guide For 2024No ratings yet

- Gross Income and ExclusionsDocument37 pagesGross Income and ExclusionsMo ZhuNo ratings yet

- The Fast Plan for Tax Reform: A Fair, Accountable, and Simple Tax Plan to Chop Away the Federal Tax ThicketFrom EverandThe Fast Plan for Tax Reform: A Fair, Accountable, and Simple Tax Plan to Chop Away the Federal Tax ThicketNo ratings yet

- TIF Problems 11-21 (2014)Document347 pagesTIF Problems 11-21 (2014)Mariella NiyoyunguruzaNo ratings yet

- INCOME TAX REVIEWER FOR MARIANO MARCOS STATE UNIVERSITYDocument50 pagesINCOME TAX REVIEWER FOR MARIANO MARCOS STATE UNIVERSITYMay Encarnina P. Gaoiran100% (5)

- Example Showing Unfairness & Discrimination - Labor's PolicyDocument12 pagesExample Showing Unfairness & Discrimination - Labor's PolicyJohn GriffithNo ratings yet

- Personal Tax Planning: Working at the MarginDocument9 pagesPersonal Tax Planning: Working at the MarginGayathri SudheerNo ratings yet

- Test Bank For Taxation For Decision Makers 2020 10th by Dennis EscoffierDocument36 pagesTest Bank For Taxation For Decision Makers 2020 10th by Dennis Escoffiersublunardisbench.2jz85100% (29)

- Buckwold 20ce sm04Document68 pagesBuckwold 20ce sm04Kailash Kumar100% (1)

- Chapters 1-3Document12 pagesChapters 1-3BethellaSamPhillipsNo ratings yet

- Tax Question BankDocument34 pagesTax Question BankRahul RajNo ratings yet

- Ebook Byrd and Chens Canadian Tax Principles 2018 2019 1St Edition Byrd Test Bank Full Chapter PDFDocument68 pagesEbook Byrd and Chens Canadian Tax Principles 2018 2019 1St Edition Byrd Test Bank Full Chapter PDFShannonRussellapcx100% (12)

- Fit Chap012Document53 pagesFit Chap012biomed12No ratings yet

- Byrd and Chens Canadian Tax Principles 2018 2019 1st Edition Byrd Test BankDocument39 pagesByrd and Chens Canadian Tax Principles 2018 2019 1st Edition Byrd Test Bankhumidityhaygsim8p100% (14)

- ANSWER: Calculating The Tax BASE. Not Tax RateDocument17 pagesANSWER: Calculating The Tax BASE. Not Tax RateAngelia TNo ratings yet

- Important - Read This FirstDocument10 pagesImportant - Read This Firstwilson garzonNo ratings yet

- Income Taxation Reviewer: Mariano Marcos State University-College of Law 2011Document59 pagesIncome Taxation Reviewer: Mariano Marcos State University-College of Law 2011Kristelle Quibuyen100% (1)

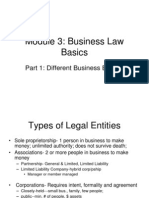

- Business Law - BasicDocument30 pagesBusiness Law - BasicGama Kristian AdikurniaNo ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- Acc 702 Assignment 4Document8 pagesAcc 702 Assignment 4laukkeasNo ratings yet

- Maximizing Your Wealth: A Comprehensive Guide to Understanding Gross and Net SalaryFrom EverandMaximizing Your Wealth: A Comprehensive Guide to Understanding Gross and Net SalaryNo ratings yet

- 413sol3 04Document17 pages413sol3 04drtoeNo ratings yet

- Cut Your Clients Tax Bill: Individual Tax Planning Tips and StrategiesFrom EverandCut Your Clients Tax Bill: Individual Tax Planning Tips and StrategiesNo ratings yet

- TIF Problems 07-10 (2014)Document141 pagesTIF Problems 07-10 (2014)Mariella NiyoyunguruzaNo ratings yet

- Week 8 Inclusions and Exclusions From The Gross Income 2023 24 1Document102 pagesWeek 8 Inclusions and Exclusions From The Gross Income 2023 24 1Arellano Rhovic R.No ratings yet

- 3 Introduction To Income TaxationDocument9 pages3 Introduction To Income TaxationRenz Allen BanaagNo ratings yet

- Foods.: A Short Phrase Used in Advertising To Identify Our ProductDocument2 pagesFoods.: A Short Phrase Used in Advertising To Identify Our Productrajes wariNo ratings yet

- SAP Accounts Receivable Training TutorialDocument34 pagesSAP Accounts Receivable Training TutorialERPDocs80% (5)

- Pestel Analysis NotesDocument2 pagesPestel Analysis Notesrajes wariNo ratings yet

- Foods.: A Short Phrase Used in Advertising To Identify Our ProductDocument2 pagesFoods.: A Short Phrase Used in Advertising To Identify Our Productrajes wariNo ratings yet

- Log Book May Final WorkDocument41 pagesLog Book May Final Workrajes wariNo ratings yet

- Log Book Hanson July WorkDocument33 pagesLog Book Hanson July Workrajes wariNo ratings yet

- Telephone Business Conversation Role-PlayDocument3 pagesTelephone Business Conversation Role-Playrajes wariNo ratings yet

- Hotel PicturesDocument2 pagesHotel Picturesrajes wariNo ratings yet

- INVOICE Photography and VideographyDocument1 pageINVOICE Photography and Videographyrajes wariNo ratings yet

- Date Work Summary/Daily Activities Duration RemarksDocument38 pagesDate Work Summary/Daily Activities Duration Remarksrajes wariNo ratings yet

- Account Receivable Department Goals and ResponsibilitiesDocument3 pagesAccount Receivable Department Goals and Responsibilitiesrajes wariNo ratings yet

- Accounting Information System 1 - Ais20103Document35 pagesAccounting Information System 1 - Ais20103rajes wariNo ratings yet

- EditingDocument5 pagesEditingrajes wariNo ratings yet

- Task ResponsibilityDocument1 pageTask Responsibilityrajes wariNo ratings yet

- 170121131635Document29 pages170121131635Hazim YusoffNo ratings yet

- Practical Training Report: Bachelor of Accountancy (Hons.) Faculty of AccountancyDocument13 pagesPractical Training Report: Bachelor of Accountancy (Hons.) Faculty of AccountancytalashNo ratings yet

- Bar Graph and ConclusionDocument4 pagesBar Graph and Conclusionrajes wari0% (1)

- LI ReportDocument28 pagesLI Reportrajes wariNo ratings yet

- Challenges GST of Implementation in MalaysiaDocument3 pagesChallenges GST of Implementation in Malaysiarajes wariNo ratings yet

- Review of GST Vs SST Implementation in MalaysiaDocument10 pagesReview of GST Vs SST Implementation in Malaysiarajes wariNo ratings yet

- Bank Islam Malaysia Bhd v Adnan bin Omar case analysisDocument10 pagesBank Islam Malaysia Bhd v Adnan bin Omar case analysisrajes wariNo ratings yet

- Accounting Information System 1 - Ais20103Document9 pagesAccounting Information System 1 - Ais20103rajes wariNo ratings yet

- Executive Summary NewDocument3 pagesExecutive Summary Newrajes wariNo ratings yet

- Impairment of Goodwill AtapDocument2 pagesImpairment of Goodwill Ataprajes wariNo ratings yet

- Exam PaperDocument5 pagesExam Paperrajes wariNo ratings yet

- Shariah ComplianceDocument3 pagesShariah Compliancerajes wariNo ratings yet

- Code of Ethics for AuditorsDocument29 pagesCode of Ethics for Auditorsrajes wari50% (2)

- Impairment of Goodwill AtapDocument2 pagesImpairment of Goodwill Ataprajes wariNo ratings yet

- Tax Allowable ExpensesDocument2 pagesTax Allowable Expensesdavidhor75% (4)

- Principle of MicroeconomicsDocument4 pagesPrinciple of Microeconomicsrajes wariNo ratings yet

- Refrigeration and Air Conditioning Technology 8th Edition Tomczyk Silberstein Whitman Johnson Solution ManualDocument5 pagesRefrigeration and Air Conditioning Technology 8th Edition Tomczyk Silberstein Whitman Johnson Solution Manualrachel100% (24)

- Work, Energy Power RevDocument31 pagesWork, Energy Power RevRency Micaella CristobalNo ratings yet

- Worksheet - Solubility - Water As A SolventDocument2 pagesWorksheet - Solubility - Water As A Solventben4657No ratings yet

- Personal and Group Trainer Juan Carlos GonzalezDocument2 pagesPersonal and Group Trainer Juan Carlos GonzalezDidier G PeñuelaNo ratings yet

- IEC60947 3 Approved PDFDocument3 pagesIEC60947 3 Approved PDFosmpotNo ratings yet

- Asbestos exposure bulletinDocument2 pagesAsbestos exposure bulletintimNo ratings yet

- CN LSHC The Future of Pharmacy en 031120Document8 pagesCN LSHC The Future of Pharmacy en 031120marina_netNo ratings yet

- Structure Dismantling JSADocument2 pagesStructure Dismantling JSAtnssbhaskar69% (13)

- MicrosystemDocument5 pagesMicrosystembabalalaNo ratings yet

- Chemistry Tshirt ProjectDocument7 pagesChemistry Tshirt Projectapi-524483093No ratings yet

- Persuasive Speech On Behalf of Inspector GooleDocument4 pagesPersuasive Speech On Behalf of Inspector GooleSahanaNo ratings yet

- Arthropods: A Guide to the Diverse PhylumDocument10 pagesArthropods: A Guide to the Diverse Phylumpkkalai112No ratings yet

- Installation TubeeeDocument7 pagesInstallation TubeeeDini NovitrianingsihNo ratings yet

- AMGG-S - 1 - Environmental Safeguard Monitoring - 25.03.2021Document48 pagesAMGG-S - 1 - Environmental Safeguard Monitoring - 25.03.2021Mahidul Islam RatulNo ratings yet

- Certificate of Employment Document TitleDocument1 pageCertificate of Employment Document TitleAyni ReyesNo ratings yet

- M96SC05 Oleo StrutDocument6 pagesM96SC05 Oleo Strutchaumont12345No ratings yet

- Writing About Emotional Experiences As A Therapeutic Process PDFDocument6 pagesWriting About Emotional Experiences As A Therapeutic Process PDFOscarNo ratings yet

- MSDS - ENTEL BatteryDocument3 pagesMSDS - ENTEL BatteryChengNo ratings yet

- Rendemen Dan Skrining Fitokimia Pada Ekstrak DaunDocument6 pagesRendemen Dan Skrining Fitokimia Pada Ekstrak DaunArdya YusidhaNo ratings yet

- ASP Quarterly Report FormsDocument16 pagesASP Quarterly Report FormsMaria Rosario GeronimoNo ratings yet

- Objectives and Aspects of School Health ServicesDocument4 pagesObjectives and Aspects of School Health ServicesRaed AlhnaityNo ratings yet

- Extraction and Isolation of Saponins PDFDocument2 pagesExtraction and Isolation of Saponins PDFMikeNo ratings yet

- Thalassemia WikiDocument12 pagesThalassemia Wikiholy_miracleNo ratings yet

- embragues-INTORK KBK14800 Erhsa2013 PDFDocument56 pagesembragues-INTORK KBK14800 Erhsa2013 PDFPablo RuizNo ratings yet

- Ipao Program Flyer 17novDocument1 pageIpao Program Flyer 17novapi-246252391No ratings yet

- Project Report On Biodegradable Plates, Glasses, Food Container, Spoon Etc.Document6 pagesProject Report On Biodegradable Plates, Glasses, Food Container, Spoon Etc.EIRI Board of Consultants and Publishers0% (1)

- HZB-15S Service ManualDocument20 pagesHZB-15S Service ManualJason Cravy100% (1)

- Self-Adhesive Resin Cements Ph-Neutralization, HydrophilicityDocument7 pagesSelf-Adhesive Resin Cements Ph-Neutralization, HydrophilicityCarolina Rodríguez RamírezNo ratings yet

- Bio23 LindenDocument34 pagesBio23 LindenDjamal ToeNo ratings yet

- ZV Class Links @Medliferesuscitation-CopyDocument31 pagesZV Class Links @Medliferesuscitation-CopyDebajyoti DasNo ratings yet