You might also like

- Botswana Power SectorDocument19 pagesBotswana Power SectorJeremiah MatongotiNo ratings yet

- 2018-2027 Biselco PSPPDocument24 pages2018-2027 Biselco PSPPCalamianes Seaweed Marketing CooperativeNo ratings yet

- Renewable Integration - POWERGRIDDocument29 pagesRenewable Integration - POWERGRIDvaibhav bodkheNo ratings yet

- Power Plan for Haryana Sub-RegionDocument38 pagesPower Plan for Haryana Sub-Regionjiguparmar20094903No ratings yet

- BillDocument2 pagesBillHafiz RahimNo ratings yet

- Electricity ProjectDocument2 pagesElectricity ProjectNidhin ChandranNo ratings yet

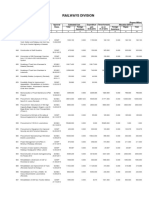

- Railways Division: On-Going SchemesDocument3 pagesRailways Division: On-Going SchemesHafiz Muhammad Zulqarnain JamilNo ratings yet

- 2015 - REP ERA Grid Analysis ReportDocument57 pages2015 - REP ERA Grid Analysis ReportsedianpoNo ratings yet

- Week 9-10 Per Unit QuantitiesDocument2 pagesWeek 9-10 Per Unit QuantitiesbeneNo ratings yet

- RENEWABLE ENERGY DEVELOPMENT PLAN (REDP) Demand / Supply ScenarioDocument12 pagesRENEWABLE ENERGY DEVELOPMENT PLAN (REDP) Demand / Supply ScenarioEnergy Trading QUEZELCO 1No ratings yet

- Smart Grid in TransmissionDocument26 pagesSmart Grid in TransmissionAEE 400KVNo ratings yet

- AIMS III Lessons Learned and Challenges - Presentation - 20210420 LTMS PIPDocument15 pagesAIMS III Lessons Learned and Challenges - Presentation - 20210420 LTMS PIPChong JiazhenNo ratings yet

- ENERGY MIX OPTIMIZATIONDocument22 pagesENERGY MIX OPTIMIZATIONReymart ManablugNo ratings yet

- Backup DataDocument6 pagesBackup DataAnjani kumarNo ratings yet

- Energy Demand On 2040 PDFDocument57 pagesEnergy Demand On 2040 PDFVastie RozulNo ratings yet

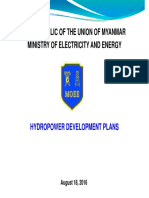

- The Republic of The Union of Myanmar Ministry of Electricity and Energy Hydropower Development PlansDocument24 pagesThe Republic of The Union of Myanmar Ministry of Electricity and Energy Hydropower Development PlansTHAN HAN100% (2)

- (10.5) PSPP - Distribution Utility 210924-1338Document21 pages(10.5) PSPP - Distribution Utility 210924-1338BernalynMalinaoNo ratings yet

- (10.5) PSPP - Distribution Utility 210924-1338Document21 pages(10.5) PSPP - Distribution Utility 210924-1338BernalynMalinaoNo ratings yet

- Rakesh R S Saudi Tabreed District CoolingDocument19 pagesRakesh R S Saudi Tabreed District CoolingAbdul Aziz Abdul Razak KedahNo ratings yet

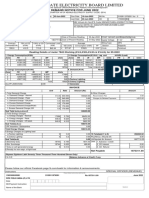

- Kerala State Electricity Board Limited: Demand Notice For June 2020Document2 pagesKerala State Electricity Board Limited: Demand Notice For June 2020Vamsi SwapnaNo ratings yet

- Supply Daya Listrik Bali (5)Document8 pagesSupply Daya Listrik Bali (5)Krisna BayuNo ratings yet

- Est 002273Document1 pageEst 002273PRINT HUBNo ratings yet

- DOP-II Project to Rehabilitate Distribution NetworkDocument12 pagesDOP-II Project to Rehabilitate Distribution NetworkAHMED HASSAN RAZANo ratings yet

- Amir Sab 8.2 KW and 5HPDocument3 pagesAmir Sab 8.2 KW and 5HPch.ahmad90000000No ratings yet

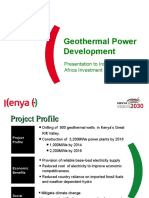

- Geothermal Power Development: Presentation To Institutional Investor Africa Investment ConferenceDocument16 pagesGeothermal Power Development: Presentation To Institutional Investor Africa Investment ConferenceKenya Ict BoardNo ratings yet

- SL - No. Category Nos. Consumer (%) Consumption (%)Document2 pagesSL - No. Category Nos. Consumer (%) Consumption (%)havejsnjNo ratings yet

- Sanjid Vai EEE Syllabus PDFDocument27 pagesSanjid Vai EEE Syllabus PDFSakib HossainNo ratings yet

- Power Plant IntroductionDocument15 pagesPower Plant IntroductionBlackNo ratings yet

- Farakka-Gokarna 400 KV D/C, Sagardighi-Gokarna 400 KV D/C fault levelsDocument1 pageFarakka-Gokarna 400 KV D/C, Sagardighi-Gokarna 400 KV D/C fault levelsbinodeNo ratings yet

- The Crucial Role of Natural Gas and LNG For Power in BangladeshDocument19 pagesThe Crucial Role of Natural Gas and LNG For Power in BangladeshLNG Cell PetrobanglaNo ratings yet

- Cost Benefit Analysis-1Document2 pagesCost Benefit Analysis-1dhjNo ratings yet

- Albania Transmission Network Development PlanDocument15 pagesAlbania Transmission Network Development PlanJ.LNo ratings yet

- Lecture 13Document34 pagesLecture 13kamran bhatNo ratings yet

- TEL Semi Post-Sales Revenue RoadmapDocument2 pagesTEL Semi Post-Sales Revenue Roadmap00 00No ratings yet

- Energy MGMT 15th-16th Jun 2015Document26 pagesEnergy MGMT 15th-16th Jun 2015vikash kumarNo ratings yet

- 39 Power Sector Assets V SEM CALACADocument14 pages39 Power Sector Assets V SEM CALACAIsagani CastilloNo ratings yet

- 5.2. Pakistan Country Presentation by A. AllaudinDocument24 pages5.2. Pakistan Country Presentation by A. Allaudinquantum_leap_windNo ratings yet

- Bahan APPKLIDocument13 pagesBahan APPKLIprimaev.idNo ratings yet

- Top Players 19-21 Lac 24 Lac 10 T 12 T 14 T Manual Hydro Manual Hydro Manual Hydro L&T Case Dynapac Escorts Escorts Hamm VolvoDocument10 pagesTop Players 19-21 Lac 24 Lac 10 T 12 T 14 T Manual Hydro Manual Hydro Manual Hydro L&T Case Dynapac Escorts Escorts Hamm VolvoAmit Vijay Gupta0% (1)

- 2016-172+RC Sukelco PDFDocument17 pages2016-172+RC Sukelco PDFArchAngel Grace Moreno BayangNo ratings yet

- Penyusutan Pemda 2022Document2,997 pagesPenyusutan Pemda 2022Galus DinamNo ratings yet

- Tel No.:033-24239659/9651 FAX No.:033-24239652/53 WebDocument18 pagesTel No.:033-24239659/9651 FAX No.:033-24239652/53 WebSanjay SatyajitNo ratings yet

- Pys PracDocument9 pagesPys PracpfaneloNo ratings yet

- Crem September 2020Document11 pagesCrem September 2020kamijou08No ratings yet

- Tamil Nadu Transmission Corporation LTD::: Report DateDocument16 pagesTamil Nadu Transmission Corporation LTD::: Report DateSrinivasan VairamanickamNo ratings yet

- Granite Processing Plant Project ReportDocument58 pagesGranite Processing Plant Project ReportsyamskhtNo ratings yet

- All Substation LossesDocument17 pagesAll Substation Lossesjecomm4No ratings yet

- 2020-2029 - Tielco - Tablas Island - PSPPDocument18 pages2020-2029 - Tielco - Tablas Island - PSPPHans CunananNo ratings yet

- Energy Regulatory CommissionDocument17 pagesEnergy Regulatory CommissionHans CunananNo ratings yet

- Third Division G.R. No. 204719, December 05, 2016: Supreme Court of The PhilippinesDocument17 pagesThird Division G.R. No. 204719, December 05, 2016: Supreme Court of The PhilippinesJoe RealNo ratings yet

- Option B Solar & Inverter System ReplacementDocument2 pagesOption B Solar & Inverter System Replacementuchenna chieduNo ratings yet

- 1.amrapur2020 4Document2 pages1.amrapur2020 4Kumar ShashiNo ratings yet

- WS Unit 4Document114 pagesWS Unit 4Himanshu RaiNo ratings yet

- KEP-22-23-01 Lifting Price ListDocument25 pagesKEP-22-23-01 Lifting Price ListShekhar Pratap SinghNo ratings yet

- DecconvDocument2 pagesDecconvabul hussainNo ratings yet

- Korina Power Plant ProjectDocument19 pagesKorina Power Plant ProjectNugroho CWNo ratings yet

- Enpi (Old) Production: Month Unit Jan Feb Mar Apr MayDocument3 pagesEnpi (Old) Production: Month Unit Jan Feb Mar Apr MayDuy Phong PhanNo ratings yet

- Design Inputs (Technical Specifications)Document5 pagesDesign Inputs (Technical Specifications)Clar CabundocanNo ratings yet

- Introduction Indian PsDocument15 pagesIntroduction Indian PsRavinder SharmaNo ratings yet

- StarLAN Technology ReportFrom EverandStarLAN Technology ReportRating: 3 out of 5 stars3/5 (1)

- MTPDP 2004-2010Document283 pagesMTPDP 2004-2010restigabuyaNo ratings yet

- Department of Public Works and Highways Department of Public Works and HighwaysDocument18 pagesDepartment of Public Works and Highways Department of Public Works and HighwaysrestigabuyaNo ratings yet

- Roadmap of P Noy Roadmap of P.Noy: Logo LogoDocument10 pagesRoadmap of P Noy Roadmap of P.Noy: Logo LogorestigabuyaNo ratings yet

- Accelerating G Private-Public Partnership (PPP) To Achieve Inclusive Growth To Achieve Inclusive GrowthDocument11 pagesAccelerating G Private-Public Partnership (PPP) To Achieve Inclusive Growth To Achieve Inclusive Growthrestigabuya100% (1)

- Accelerating G Private-Public Partnership (PPP) To Achieve Inclusive Growth To Achieve Inclusive GrowthDocument11 pagesAccelerating G Private-Public Partnership (PPP) To Achieve Inclusive Growth To Achieve Inclusive Growthrestigabuya100% (1)

- HomeWork MCS-Nurul Sari (1101002048) - Case 5.1 5.4Document5 pagesHomeWork MCS-Nurul Sari (1101002048) - Case 5.1 5.4Nurul SariNo ratings yet

- Grafice in WordDocument8 pagesGrafice in WordJeNo ratings yet

- ALLIED-Weekly-Market-Report 23 08 2020Document12 pagesALLIED-Weekly-Market-Report 23 08 2020Supreme starNo ratings yet

- 3 Sample Mpesa Aggregator - Agent AgreementDocument17 pages3 Sample Mpesa Aggregator - Agent AgreementSamuel KamauNo ratings yet

- Applied Economics 2nd Periodic ExamDocument4 pagesApplied Economics 2nd Periodic ExamKrisha FernandezNo ratings yet

- Glossary of Banking ServicesDocument6 pagesGlossary of Banking ServicesKarthik GottipatiNo ratings yet

- GoldDocument25 pagesGoldarun1417100% (1)

- Keeping in Touch With Rural IndiaDocument4 pagesKeeping in Touch With Rural Indiasaurabh shekharNo ratings yet

- Ramoso vs Court of Appeals ruling on piercing corporate veilDocument1 pageRamoso vs Court of Appeals ruling on piercing corporate veilBernadetteNo ratings yet

- BAS Vs BSSDocument2 pagesBAS Vs BSSGunjan ShahNo ratings yet

- SEC Accredited Asset Valuer As of February 29 2016Document1 pageSEC Accredited Asset Valuer As of February 29 2016Gean Pearl IcaoNo ratings yet

- Multiple Choice: Full File at Https://testbankuniv - eu/International-Economics-12th-Edition-Salvatore-Test-BankDocument9 pagesMultiple Choice: Full File at Https://testbankuniv - eu/International-Economics-12th-Edition-Salvatore-Test-BankalliNo ratings yet

- China-Pakistan Economic Corridor Challenges Opportunities and The Way ForwardDocument5 pagesChina-Pakistan Economic Corridor Challenges Opportunities and The Way ForwardMahrukh ChohanNo ratings yet

- Renewal CSWIPDocument11 pagesRenewal CSWIPG Prabhakar RajuNo ratings yet

- Animal Farm by George OrwellDocument5 pagesAnimal Farm by George OrwellDavid A. Malin Jr.100% (1)

- LOLIMSA Carmel2012 EssaludSoftware CompetitivenessDocument5 pagesLOLIMSA Carmel2012 EssaludSoftware Competitivenessjulioqt007No ratings yet

- Kilimo Kwanza Resolution - FinalDocument2 pagesKilimo Kwanza Resolution - FinalVincs KongNo ratings yet

- Schedul 25 Nov 23Document1 pageSchedul 25 Nov 23CloudyNo ratings yet

- TAMP BriefingDocument17 pagesTAMP Briefingdragon 999999100% (1)

- (Handbooks in Economics 1) Kenneth J. Arrow, A.K. Sen, Kotaro Suzumura (Eds.) - Handbook of Social Choice and Welfare, Volume 1 (Handbooks in Economics) - North-Holland (2002) PDFDocument647 pages(Handbooks in Economics 1) Kenneth J. Arrow, A.K. Sen, Kotaro Suzumura (Eds.) - Handbook of Social Choice and Welfare, Volume 1 (Handbooks in Economics) - North-Holland (2002) PDFLeonardo FerreiraNo ratings yet

- BRANCH ACCOUNTS - Assignment SolutionsDocument9 pagesBRANCH ACCOUNTS - Assignment SolutionsNaveen C GowdaNo ratings yet

- RCTDocument323 pagesRCTjeevithaNo ratings yet

- GX Cip GPLG 2016 PDFDocument54 pagesGX Cip GPLG 2016 PDFAbhijeetNo ratings yet

- LIMITS OF AN AGENT'S AUTHORITYDocument2 pagesLIMITS OF AN AGENT'S AUTHORITYLeo Joselito Estoque BonoNo ratings yet

- TD Ameritrade TRADEKEEPER PROFIT-LOSS FOR 2004 TRADES and 2017 FULTON STOCK January 9, 2017Document18 pagesTD Ameritrade TRADEKEEPER PROFIT-LOSS FOR 2004 TRADES and 2017 FULTON STOCK January 9, 2017Stan J. CaterboneNo ratings yet

- Img 0009 PDFDocument1 pageImg 0009 PDFLyna Kiki NaibahoNo ratings yet

- HRM - Labour UnrestDocument20 pagesHRM - Labour Unrestvishal shivkar100% (2)

- Visit Report: Page 1 of 26Document26 pagesVisit Report: Page 1 of 26OğuzcanYazarNo ratings yet

- CBRE National Industrial Market UpdateDocument10 pagesCBRE National Industrial Market Updatebaquang2910No ratings yet

- Morocco: Morocco Ranks 67th Among The 132 Economies Featured in The GII 2022Document14 pagesMorocco: Morocco Ranks 67th Among The 132 Economies Featured in The GII 2022HATIM KHALIDNo ratings yet