You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Entity Formation Checklist GuideDocument15 pagesEntity Formation Checklist GuideKevinNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- QL Ncpeonne PDFDocument210 pagesQL Ncpeonne PDFLiftRanger100% (2)

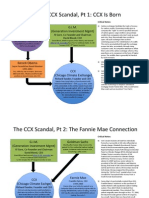

- CCX Scandal, Chicago Carbon ExchangeDocument4 pagesCCX Scandal, Chicago Carbon ExchangeKim HedumNo ratings yet

- Dealing With Student LoansDocument17 pagesDealing With Student LoansFredPahssenNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Sample Answer Foreclosure Defense New JerseyDocument15 pagesSample Answer Foreclosure Defense New Jerseyjorg100% (2)

- Chapter 3 - Classification of BanksDocument8 pagesChapter 3 - Classification of BanksShasharu Fei-fei LimNo ratings yet

- Valuation Report FormatDocument2 pagesValuation Report FormatPallu Chopra100% (3)

- Annuities Examples in Retirement Planning.... DDDDDocument9 pagesAnnuities Examples in Retirement Planning.... DDDDattaullahNo ratings yet

- Combined Closing Statement - 5Document2 pagesCombined Closing Statement - 5FRANKLYN TRONCONo ratings yet

- A Study of Current Scenario of Cyber Security Practices and Measures: Literature ReviewDocument8 pagesA Study of Current Scenario of Cyber Security Practices and Measures: Literature ReviewattaullahNo ratings yet

- Egypt PEST AnalysisDocument34 pagesEgypt PEST AnalysisAhmed M. Ezzat58% (26)

- CA Foreclosure Law - Civil Code 2924Document44 pagesCA Foreclosure Law - Civil Code 2924api-22112682No ratings yet

- Pascual v. Ramos - G.R. No. 144712Document2 pagesPascual v. Ramos - G.R. No. 144712eiram23No ratings yet

- 49 - 3 - A LiteratureDocument10 pages49 - 3 - A LiteratureattaullahNo ratings yet

- RP Tip Print NewDocument6 pagesRP Tip Print NewattaullahNo ratings yet

- Stock Market .... of India and ChinaDocument36 pagesStock Market .... of India and ChinaattaullahNo ratings yet

- Products Endorsements: MicromaxDocument1 pageProducts Endorsements: MicromaxattaullahNo ratings yet

- GST in IndiaDocument27 pagesGST in IndiarajanraorajanNo ratings yet

- DBMS functions guideDocument23 pagesDBMS functions guideattaullahNo ratings yet

- Assignment 2 of EthicsDocument9 pagesAssignment 2 of EthicsattaullahNo ratings yet

- Steel Industry PESTEL Analysis .AssingmentDocument17 pagesSteel Industry PESTEL Analysis .Assingmentattaullah33% (3)

- Ecomagination SolutionsDocument15 pagesEcomagination SolutionsattaullahNo ratings yet

- ObliconDocument16 pagesObliconDante EscuderoNo ratings yet

- Credit Insurance AaaaaDocument21 pagesCredit Insurance AaaaaRohit GuptaNo ratings yet

- Bai SalamDocument18 pagesBai SalamAli Rehman NaqiNo ratings yet

- Housing Loan Suggestions and ChallengesDocument4 pagesHousing Loan Suggestions and Challengesmariyam fathimaNo ratings yet

- Right To SubrogationDocument5 pagesRight To SubrogationAanchal KashyapNo ratings yet

- Sample Exercise - Draft A Share Pledge AgreementDocument3 pagesSample Exercise - Draft A Share Pledge AgreementSHK_1234No ratings yet

- Introduction To Taxation Student GuideDocument25 pagesIntroduction To Taxation Student GuideRevankar B R ShetNo ratings yet

- Maar, Discount Rate, Interest RateDocument2 pagesMaar, Discount Rate, Interest RateMalik HarrisNo ratings yet

- De Lucia Commercial Bank ManagementDocument395 pagesDe Lucia Commercial Bank Managementha nguyenNo ratings yet

- Modes and Tenure of LandDocument2 pagesModes and Tenure of LandSanket AiyaNo ratings yet

- IPC Sample Moot ProblemDocument1 pageIPC Sample Moot ProblemRakesh SahuNo ratings yet

- Pre ShipmentDocument8 pagesPre ShipmentRajesh ShahNo ratings yet

- 2018 Buyer Bios Profiles of Recent Home Buyers and Sellers 11-02-2018Document23 pages2018 Buyer Bios Profiles of Recent Home Buyers and Sellers 11-02-2018National Association of REALTORS®100% (1)

- Free ConsentDocument33 pagesFree ConsentsangeethamadanNo ratings yet

- The First State Bank and Trust Company of Guthrie, Oklahoma v. Sand Springs State Bank of Sand Springs, Oklahoma, 528 F.2d 350, 1st Cir. (1976)Document6 pagesThe First State Bank and Trust Company of Guthrie, Oklahoma v. Sand Springs State Bank of Sand Springs, Oklahoma, 528 F.2d 350, 1st Cir. (1976)Scribd Government DocsNo ratings yet

- Notice: Customhouse Broker License Cancellation, Suspension, Etc.: Gawi, Peter, Et Al.Document2 pagesNotice: Customhouse Broker License Cancellation, Suspension, Etc.: Gawi, Peter, Et Al.Justia.comNo ratings yet

- Nims Corrected Brief005!23!2019Document81 pagesNims Corrected Brief005!23!2019RussinatorNo ratings yet

- Chapter 09: Mortgage Markets: Page 1Document19 pagesChapter 09: Mortgage Markets: Page 1AS SANo ratings yet

- Canara BankDocument2 pagesCanara Banklinsonjohny34No ratings yet

- Assignment Notes PayableDocument3 pagesAssignment Notes PayableLourdios EdullantesNo ratings yet