You might also like

- (Jon Louis Bentley) Programming PearlsDocument195 pages(Jon Louis Bentley) Programming PearlsIndrama PurbaNo ratings yet

- Excel Modelling 1Document5 pagesExcel Modelling 1Indrama PurbaNo ratings yet

- DA4139 Level III CFA Mock Exam 1 AfternoonDocument31 pagesDA4139 Level III CFA Mock Exam 1 AfternoonIndrama Purba100% (1)

- DA4139 Level II CFA Mock Exam 1 AfternoonDocument34 pagesDA4139 Level II CFA Mock Exam 1 AfternoonIndrama Purba100% (1)

- A2 GermanDocument6 pagesA2 GermanIndrama Purba100% (1)

- Aol Time WarnerDocument5 pagesAol Time WarnerIndrama PurbaNo ratings yet

- Accretion Dilution Model SampleDocument25 pagesAccretion Dilution Model SampleIndrama PurbaNo ratings yet

- Valuation Extra DamodaranDocument44 pagesValuation Extra DamodaranIndrama PurbaNo ratings yet

- Weekly Operations Report TemplateDocument19 pagesWeekly Operations Report TemplateIndrama Purba100% (1)

- Marcelo Dos SantosDocument42 pagesMarcelo Dos SantosIndrama PurbaNo ratings yet

- Corporate Model Template Long-DataDocument274 pagesCorporate Model Template Long-DataIndrama PurbaNo ratings yet

- 06 06 Football Field Walmart Model Valuation BeforeDocument47 pages06 06 Football Field Walmart Model Valuation BeforeIndrama Purba0% (1)

- Issues To Keep in Mind in Cross-Border ValuationDocument12 pagesIssues To Keep in Mind in Cross-Border ValuationIndrama PurbaNo ratings yet

- Decision Matrix: Alternatives Criteria WeightDocument4 pagesDecision Matrix: Alternatives Criteria WeightIndrama PurbaNo ratings yet

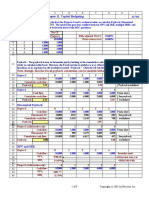

- Part 1. Worksheet For Chapter 11, Capital BudgetingDocument9 pagesPart 1. Worksheet For Chapter 11, Capital BudgetingIndrama PurbaNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5795)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Management Consulting in The US Industry ReportDocument37 pagesManagement Consulting in The US Industry ReportDeepankur MalikNo ratings yet

- Tamkeen - Final IA Report - HR Process-EnglishDocument37 pagesTamkeen - Final IA Report - HR Process-EnglishHarsh JainNo ratings yet

- Offshore Africa - July - 2020 PDFDocument44 pagesOffshore Africa - July - 2020 PDFNorvinyeLorlortorYekoNo ratings yet

- Telecom Analytics SolutionsDocument12 pagesTelecom Analytics Solutionsdivya2882No ratings yet

- Koss Corporation Fraud Case Analysis FinalDocument28 pagesKoss Corporation Fraud Case Analysis FinalMarianeNo ratings yet

- Resume Book: Columbia Healthcare and Pharmaceutical Management ProgramDocument44 pagesResume Book: Columbia Healthcare and Pharmaceutical Management ProgramJohn Mathias100% (2)

- Capacity BuildingDocument28 pagesCapacity BuildingMichael Earl MitchellNo ratings yet

- Benchmarking Study: Comparison of Performance in The E&P Upstream BusinessDocument17 pagesBenchmarking Study: Comparison of Performance in The E&P Upstream BusinessDeepesh PathakNo ratings yet

- PWC AnrDocument2 pagesPWC AnrKumar GauravNo ratings yet

- Corporate Governance in Ford Motor CompanyDocument14 pagesCorporate Governance in Ford Motor CompanyLarisa Samciuc100% (3)

- Nicholas Provenzano ResumeDocument2 pagesNicholas Provenzano Resumeapi-272201993No ratings yet

- The PWC Audit - 011704 PresentationDocument34 pagesThe PWC Audit - 011704 PresentationSohail AusafNo ratings yet

- The Impact of Forensic Accounting On Financial Performance of Investment FirmsDocument5 pagesThe Impact of Forensic Accounting On Financial Performance of Investment Firmsfelipe100% (1)

- PWC - Risk Apetite FrameworkDocument28 pagesPWC - Risk Apetite Frameworkchujiyo100% (1)

- The US Foodservice Accounting FraudDocument14 pagesThe US Foodservice Accounting FraudAnant Agarwal0% (1)

- PWC Family Business Survey 2010-2011Document52 pagesPWC Family Business Survey 2010-2011ausldNo ratings yet

- PWC - AcceleratorDocument29 pagesPWC - AcceleratorgerardkokNo ratings yet

- PWC News Alert 6 August 2019 Gift Received by An IndividualDocument3 pagesPWC News Alert 6 August 2019 Gift Received by An IndividualsachingnNo ratings yet

- Library Closures Third Report of Session 2012-13 (Vol. 2) - DCMIDocument306 pagesLibrary Closures Third Report of Session 2012-13 (Vol. 2) - DCMILJ's infoDOCKET0% (1)

- Reading 03 PDFDocument4 pagesReading 03 PDFPhương NguyễnNo ratings yet

- PWC Team 14 PresentationDocument10 pagesPWC Team 14 PresentationChandler ScottNo ratings yet

- PWC Graduate Recruitment BrochureDocument8 pagesPWC Graduate Recruitment Brochurejay_pNo ratings yet

- (2006) SGHC 146Document63 pages(2006) SGHC 146Chye Ming Tuck JonathanNo ratings yet

- The Business Developer's Playbook - Relationship Selling Principles and The Dna of Dialogue Selling (PDFDrive)Document161 pagesThe Business Developer's Playbook - Relationship Selling Principles and The Dna of Dialogue Selling (PDFDrive)mahmoud massoud100% (1)

- Customer Analytics Apr13Document2 pagesCustomer Analytics Apr13g3072No ratings yet

- AB INT May 2015Document68 pagesAB INT May 2015toushigaNo ratings yet

- PWC Global Fintech Report 2019Document29 pagesPWC Global Fintech Report 2019Hoàng Châu Trần ĐoànNo ratings yet

- Construction Authority, Singapore 5 Days (June 2008)Document13 pagesConstruction Authority, Singapore 5 Days (June 2008)Raghavendra NaduvinamaniNo ratings yet

- Tejendrasinh Gohil: TH THDocument7 pagesTejendrasinh Gohil: TH THSureshArigelaNo ratings yet

- Shobhit Saxena - CSTR - SabenaDocument6 pagesShobhit Saxena - CSTR - SabenaShobhit SaxenaNo ratings yet