You might also like

- Schaum's Outline of Principles of Accounting I, Fifth EditionFrom EverandSchaum's Outline of Principles of Accounting I, Fifth EditionRating: 5 out of 5 stars5/5 (3)

- Political LawDocument227 pagesPolitical Lawcarlavillanueva80% (5)

- Job Order Costing HandoutsDocument8 pagesJob Order Costing HandoutsHannah Jane Arevalo LafuenteNo ratings yet

- VIRGEN MILAGROSA UNIVERSITY COST ACCOUNTING QUIZDocument4 pagesVIRGEN MILAGROSA UNIVERSITY COST ACCOUNTING QUIZMary Joanne Tapia33% (3)

- Handbook of Frauds Scams and Swindles PDFDocument414 pagesHandbook of Frauds Scams and Swindles PDFswathivishnuNo ratings yet

- 12 Accounting For OverheadDocument14 pages12 Accounting For OverheadSea Jean Paloma67% (3)

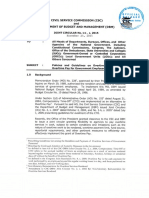

- CSC-DBM Guidelines On OvertimeDocument8 pagesCSC-DBM Guidelines On OvertimeVincent Bautista100% (2)

- CostDocument161 pagesCostMae Namoc67% (6)

- Job Order Costing Chapter 5 SummaryDocument16 pagesJob Order Costing Chapter 5 SummaryMico Duñas CruzNo ratings yet

- Cost & Managerial Accounting II EssentialsFrom EverandCost & Managerial Accounting II EssentialsRating: 4 out of 5 stars4/5 (1)

- Cost Accounting & Control Midterm ExaminationDocument7 pagesCost Accounting & Control Midterm ExaminationFerb CruzadaNo ratings yet

- Asset Recognition and Operating Assets: Fourth EditionDocument55 pagesAsset Recognition and Operating Assets: Fourth EditionAyush JainNo ratings yet

- CH 06Document39 pagesCH 06JOEMAR LEGRESONo ratings yet

- 05 Job Order Costing-1Document15 pages05 Job Order Costing-1RodelLaborNo ratings yet

- Political-Law-Reviewer San Beda PDFDocument95 pagesPolitical-Law-Reviewer San Beda PDFCharlie Pein96% (45)

- Bsa 2103-Cost Accounting and Control Midterm Departmental Exam Reviewer Multiple ChoiceDocument17 pagesBsa 2103-Cost Accounting and Control Midterm Departmental Exam Reviewer Multiple ChoiceFerb CruzadaNo ratings yet

- Comprehensive Exam A: Cost Accounting SolutionsDocument30 pagesComprehensive Exam A: Cost Accounting Solutionsakeila3100% (1)

- COMPREHENSIVE EXAMINATION A REVIEWDocument28 pagesCOMPREHENSIVE EXAMINATION A REVIEWJoshua GibsonNo ratings yet

- Cost AccountingDocument16 pagesCost AccountingKezia SantosidadNo ratings yet

- The Ledger & Trial BalanceDocument4 pagesThe Ledger & Trial BalanceJohn Marvin Delacruz Renacido80% (5)

- Assign 1 Engagement LetterDocument7 pagesAssign 1 Engagement LetterZoe Moran100% (1)

- Job Order Costing QuizDocument5 pagesJob Order Costing Quizxenoyew100% (1)

- The Pursuit of New Product Development: The Business Development ProcessFrom EverandThe Pursuit of New Product Development: The Business Development ProcessNo ratings yet

- Bsa 2103 Cost Accounting and ControlDocument17 pagesBsa 2103 Cost Accounting and ControlshaylieeeNo ratings yet

- Factory Overhead: Planned, Actual, and Applied: Multiple ChoiceDocument16 pagesFactory Overhead: Planned, Actual, and Applied: Multiple ChoiceCassandra Dianne Ferolino Macado100% (1)

- Optimizing Factory Performance: Cost-Effective Ways to Achieve Significant and Sustainable ImprovementFrom EverandOptimizing Factory Performance: Cost-Effective Ways to Achieve Significant and Sustainable ImprovementNo ratings yet

- 05.job Order Costing PDFDocument15 pages05.job Order Costing PDFArden GenesNo ratings yet

- Job Order Costing Chapter 5 Multiple Choice QuestionsDocument28 pagesJob Order Costing Chapter 5 Multiple Choice QuestionsJewel Anne RentumaNo ratings yet

- Job Order 2Document15 pagesJob Order 2Ace LimpinNo ratings yet

- Chapter 5 Job Order Costing: Multiple ChoiceDocument16 pagesChapter 5 Job Order Costing: Multiple ChoiceRandy AsnorNo ratings yet

- Job-order Costing ExplainedDocument6 pagesJob-order Costing ExplainedJennielyn GalutanNo ratings yet

- 12 Factory Overhead - Planned, Actual - AppliedDocument13 pages12 Factory Overhead - Planned, Actual - AppliedAANo ratings yet

- Dokumen - Tips - 12 Factory Overhead Planned Actual AppliedDocument13 pagesDokumen - Tips - 12 Factory Overhead Planned Actual AppliedDenny Kridex OmolonNo ratings yet

- C5 (MC) - Cost Accounting by Carter (Part1)Document4 pagesC5 (MC) - Cost Accounting by Carter (Part1)AkiNo ratings yet

- Cost Accounting Quiz 3Document10 pagesCost Accounting Quiz 3Saeym SegoviaNo ratings yet

- Cost AccountingDocument9 pagesCost AccountinghiroxhereNo ratings yet

- Test Bank Business Environment and Concepts 2Document69 pagesTest Bank Business Environment and Concepts 2Sky SoronoiNo ratings yet

- Cost Accounting Chapter 12: Factory Overhead Multiple Choice QuestionsDocument17 pagesCost Accounting Chapter 12: Factory Overhead Multiple Choice QuestionsBeatrice TehNo ratings yet

- Instruments Payable at A Bank PDFDocument2 pagesInstruments Payable at A Bank PDFAlondra Joan MararacNo ratings yet

- Faith Job Costing ProblemsDocument10 pagesFaith Job Costing Problemsfaith olaNo ratings yet

- Job Costing Overhead RatesDocument5 pagesJob Costing Overhead RatesDaniella Mae ElipNo ratings yet

- CosthuliDocument7 pagesCosthulikmarisseeNo ratings yet

- Mock Exam 1 - Chapters 1 - 4Document8 pagesMock Exam 1 - Chapters 1 - 4Thomas Matheny100% (1)

- Stat Cost MGT Midterms RevisedDocument7 pagesStat Cost MGT Midterms Revisedjoneth.duenasNo ratings yet

- Answers Homework # 15 Cost MGMT 4Document7 pagesAnswers Homework # 15 Cost MGMT 4Raman ANo ratings yet

- Prelim Mas 1-TestDocument16 pagesPrelim Mas 1-TestChrisNo ratings yet

- Comp ExamsDocument28 pagesComp ExamsTomoko KatoNo ratings yet

- Popquizch4Au11 182nlk8Document3 pagesPopquizch4Au11 182nlk8PrincessNo ratings yet

- Standard Costing: Incorporating Standards Into The Accounting RecordsDocument24 pagesStandard Costing: Incorporating Standards Into The Accounting RecordsLaurenz Simon Manalili100% (1)

- MANUFACTURING COST REVIEWDocument12 pagesMANUFACTURING COST REVIEWJuan Dela CruzNo ratings yet

- Job Costing Chapter 4 Key ConceptsDocument8 pagesJob Costing Chapter 4 Key Conceptsangelbear2577100% (1)

- Job Order Assignment PDFDocument3 pagesJob Order Assignment PDFAnne Marie100% (1)

- This Study Resource WasDocument4 pagesThis Study Resource WasNhel AlvaroNo ratings yet

- University of Caloocan City Cost Accounting & Control Quiz No. 1Document8 pagesUniversity of Caloocan City Cost Accounting & Control Quiz No. 1Mikha SemañaNo ratings yet

- Answers Homework # 16 Cost MGMT 5Document7 pagesAnswers Homework # 16 Cost MGMT 5Raman ANo ratings yet

- Bsa 2202 SCM PrelimDocument17 pagesBsa 2202 SCM PrelimKezia SantosidadNo ratings yet

- Cost Accounting Concepts ExplainedDocument6 pagesCost Accounting Concepts ExplainedAdrian SaplalaNo ratings yet

- 1Document3 pages1Sunshine Vee0% (1)

- Reviewer 2Document21 pagesReviewer 2nicolearetano417No ratings yet

- 05.16.2023 ASSIGNMENT Activity Problem With Theories-Process Costing and JOB Order Costing - With ANSWER KEYDocument11 pages05.16.2023 ASSIGNMENT Activity Problem With Theories-Process Costing and JOB Order Costing - With ANSWER KEYAngel Cil RuleteNo ratings yet

- Cost Concept Exercises PDFDocument2 pagesCost Concept Exercises PDFAina OracionNo ratings yet

- 02.02.2024 Accounting Cycle For A Manufacturing Company1Document34 pages02.02.2024 Accounting Cycle For A Manufacturing Company1Dennis N. IndigNo ratings yet

- Bac 202Document51 pagesBac 202Brian MutuaNo ratings yet

- Revision Week 1. Questions. Question 1. Cost of Goods Manufactured, Cost of Goods Sold, Income Statement. (A)Document5 pagesRevision Week 1. Questions. Question 1. Cost of Goods Manufactured, Cost of Goods Sold, Income Statement. (A)Sujib BarmanNo ratings yet

- CA 04 - Job Order CostingDocument17 pagesCA 04 - Job Order CostingJoshua UmaliNo ratings yet

- ACC 231 Pre TestDocument4 pagesACC 231 Pre TestM ANo ratings yet

- Recent Jurisprudence Legal EthicsDocument29 pagesRecent Jurisprudence Legal Ethicsmarge carreonNo ratings yet

- Republic of The Philippines Manila en BancDocument220 pagesRepublic of The Philippines Manila en BancArya StarkNo ratings yet

- 27 Legaspi Vs Civil Service Commission 150 SCRA 530Document5 pages27 Legaspi Vs Civil Service Commission 150 SCRA 530Ritz Angelica AlejandroNo ratings yet

- Cases PERSONS C5-14Document49 pagesCases PERSONS C5-14Arya StarkNo ratings yet

- G.R. No. 208566 1Document28 pagesG.R. No. 208566 1Arya StarkNo ratings yet

- GR 187167 Magallona V Exec SecretaryDocument30 pagesGR 187167 Magallona V Exec SecretaryArya StarkNo ratings yet

- Top Provisions in CIVIL LAW IDocument5 pagesTop Provisions in CIVIL LAW IsanNo ratings yet

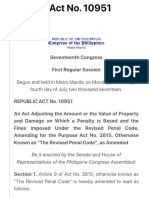

- Republic Act No. 10951Document80 pagesRepublic Act No. 10951Arya StarkNo ratings yet

- G.R. No. L-63915 2Document16 pagesG.R. No. L-63915 2Arya StarkNo ratings yet

- G.R. No. 103144Document27 pagesG.R. No. 103144Arya StarkNo ratings yet

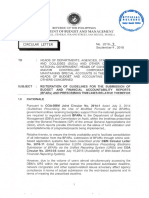

- CL No2018 9Document4 pagesCL No2018 9jojeNo ratings yet

- Oposa V Factoran, GR No. 101083, July 30, 1993, On The State's Responsibility To Protect The Right To Live in A Healthy EnvironmentDocument23 pagesOposa V Factoran, GR No. 101083, July 30, 1993, On The State's Responsibility To Protect The Right To Live in A Healthy EnvironmentRex Lagunzad FloresNo ratings yet

- New - JMC - Dbm-Ccc-Dilg No. 2015 - 01 Tagging Climate Change Expenditures PDFDocument29 pagesNew - JMC - Dbm-Ccc-Dilg No. 2015 - 01 Tagging Climate Change Expenditures PDFArya StarkNo ratings yet

- 1tfice of The I3reoibent of The Vbilippineg Alatatan"ang: y Ji% 5125 JAN 202IDDocument8 pages1tfice of The I3reoibent of The Vbilippineg Alatatan"ang: y Ji% 5125 JAN 202IDArya StarkNo ratings yet

- DBM Amends BED Formats for PREXC-Based BudgetingDocument11 pagesDBM Amends BED Formats for PREXC-Based BudgetinggbenjielizonNo ratings yet

- 01 Glossary of Terms December 2002Document20 pages01 Glossary of Terms December 2002Tracy KayeNo ratings yet

- PSA 230 RedraftedDocument15 pagesPSA 230 RedraftedSteven Wilson PauliteNo ratings yet

- Philippine Standards On Auditing 220 RedraftedDocument20 pagesPhilippine Standards On Auditing 220 RedraftedJayNo ratings yet

- Philippine Standards On Auditing 220 RedraftedDocument20 pagesPhilippine Standards On Auditing 220 RedraftedJayNo ratings yet

- PSA 100 - Philippine Framework For Assurance EngagementDocument26 pagesPSA 100 - Philippine Framework For Assurance EngagementHezekiah Reginalde Recta100% (1)

- PSA 210 RedraftedDocument40 pagesPSA 210 RedraftedVal Benedict MedinaNo ratings yet

- PSA 210 RedraftedDocument40 pagesPSA 210 RedraftedVal Benedict MedinaNo ratings yet

- Civil CodeDocument178 pagesCivil CodeArya StarkNo ratings yet

- PSA 120 Framework of Philippine Standards on AuditingDocument9 pagesPSA 120 Framework of Philippine Standards on AuditingMichael Vincent Buan SuicoNo ratings yet

- PSA 120 Framework of Philippine Standards on AuditingDocument9 pagesPSA 120 Framework of Philippine Standards on AuditingMichael Vincent Buan SuicoNo ratings yet

- IAASB Interim Terms of Reference Aug 2004Document6 pagesIAASB Interim Terms of Reference Aug 2004Daniel TadejaNo ratings yet

- 01 Glossary of Terms December 2002Document20 pages01 Glossary of Terms December 2002Tracy KayeNo ratings yet

- Adjusting entries and financial statements for Praca General ServicesDocument45 pagesAdjusting entries and financial statements for Praca General ServicesKarla pauline BernasNo ratings yet

- Controller Audit Finance Manager in Los Angeles CA Resume Renee RobinsonDocument2 pagesController Audit Finance Manager in Los Angeles CA Resume Renee RobinsonReneeRobinsonNo ratings yet

- Job Costing System for Pisano Company TITLE Accounting Press Job Costing HomeworkDocument2 pagesJob Costing System for Pisano Company TITLE Accounting Press Job Costing HomeworkYogie YaditraNo ratings yet

- Ahlan Nur Salim - Tugas 3Document4 pagesAhlan Nur Salim - Tugas 3Moe ChannelNo ratings yet

- DCW Ltd. - Annual Report - 2004-2005Document44 pagesDCW Ltd. - Annual Report - 2004-2005kayalonthewebNo ratings yet

- AIS Chapter 1Document46 pagesAIS Chapter 1Ma. Elene MagdaraogNo ratings yet

- Bernardo Corporation Statement of Financial Position As of Year 2019 AssetsDocument3 pagesBernardo Corporation Statement of Financial Position As of Year 2019 AssetsJean Marie DelgadoNo ratings yet

- Receipts and PaymentsDocument23 pagesReceipts and Payments강준구No ratings yet

- Audit Knemonics 1Document13 pagesAudit Knemonics 1chandresh100% (1)

- ACN II - Home Assignment 1Document8 pagesACN II - Home Assignment 1Mehrab Hussain ZainNo ratings yet

- Account - Statement - PDF - 1570007079602 - 07 June 2021Document1 pageAccount - Statement - PDF - 1570007079602 - 07 June 2021salman alfarisyNo ratings yet

- Management Advisory Services Review PRELIMDocument5 pagesManagement Advisory Services Review PRELIMSintos Carlos MiguelNo ratings yet

- Auditing Trs by IcapDocument53 pagesAuditing Trs by IcapArif AliNo ratings yet

- FA Assignment - 5 (Group 5)Document3 pagesFA Assignment - 5 (Group 5)Muskan ValbaniNo ratings yet

- AcFn 611-ch VII Revised PDFDocument63 pagesAcFn 611-ch VII Revised PDFtemedebereNo ratings yet

- UTS-Bhs Inggris Akuntansi MalamDocument1 pageUTS-Bhs Inggris Akuntansi MalamAnonymous Fn7Ko5riKT100% (1)

- CA Notes1Document30 pagesCA Notes1jeyoon13No ratings yet

- Coal Project - Scenario - Probabilistic - DCF Vs RO - XDocument284 pagesCoal Project - Scenario - Probabilistic - DCF Vs RO - XMia FebrinaNo ratings yet

- PIA3 A InglesDocument17 pagesPIA3 A Inglesmobbcarlos23No ratings yet

- Homework T1. Fin Account - IntroductionDocument4 pagesHomework T1. Fin Account - IntroductionCrayZeeAlexNo ratings yet

- FABM 1 Answer Sheet Q1 W5Document2 pagesFABM 1 Answer Sheet Q1 W5Florante De LeonNo ratings yet

- Chapter 14 Akun Keuangan TugasDocument2 pagesChapter 14 Akun Keuangan Tugassegeri kecNo ratings yet

- 03 Working With Project TransactionsDocument70 pages03 Working With Project TransactionsKarthik ShriramneniNo ratings yet

- Analytical Procedures Used in The Overall Review StageDocument6 pagesAnalytical Procedures Used in The Overall Review StageQueen ValleNo ratings yet

- CH 11Document55 pagesCH 11Bhavin purohitNo ratings yet

- WendysDocument13 pagesWendysJomariVillanuevaNo ratings yet