You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Công nghệ Hybrid trên xe KIA Optima 2011Document306 pagesCông nghệ Hybrid trên xe KIA Optima 2011auhut100% (3)

- Business History of Latin AmericaDocument257 pagesBusiness History of Latin AmericaDaniel Alejandro Alzate100% (2)

- 2018 Case and Course Outline in Banking Laws - Dean DivinaDocument14 pages2018 Case and Course Outline in Banking Laws - Dean DivinaA.A DizonNo ratings yet

- PaystubDocument1 pagePaystubscalesjacob1997No ratings yet

- 5supreet SakshiDocument13 pages5supreet SakshietikaNo ratings yet

- Abstract Sustainable Renewable Energy Development Program (Suredep) Through Gender Power Upstreaming For Bicol Region (Phase I) .Docx - 0Document1 pageAbstract Sustainable Renewable Energy Development Program (Suredep) Through Gender Power Upstreaming For Bicol Region (Phase I) .Docx - 0Norlijun V. HilutinNo ratings yet

- Liu Shaoqi - How To Be A Good CommunistDocument2 pagesLiu Shaoqi - How To Be A Good CommunistAnonymous MWc2SnBb100% (1)

- Tugas ToeflDocument3 pagesTugas ToeflIkaa NurNo ratings yet

- CH IIDocument8 pagesCH IISaso M. KordyNo ratings yet

- Alexander Scriabin's MysteriumDocument24 pagesAlexander Scriabin's MysteriumHeitor MarangoniNo ratings yet

- 002 PDFDocument59 pages002 PDFKristine Lapada TanNo ratings yet

- Insha Spreadsheet Marketing Contact DataDocument14 pagesInsha Spreadsheet Marketing Contact DataAbhishek SinghNo ratings yet

- Facts About FASBDocument8 pagesFacts About FASBvssvaraprasadNo ratings yet

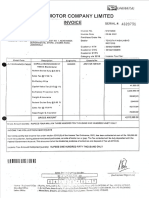

- Toyota InvoiceDocument1 pageToyota InvoiceRita SJNo ratings yet

- Amazon Merch Tax Information Interview PDFDocument3 pagesAmazon Merch Tax Information Interview PDFVishal KumarNo ratings yet

- Global Finance Graduate Programme, Novo NordiskDocument1 pageGlobal Finance Graduate Programme, Novo NordiskMylinh VuNo ratings yet

- 2000 Upsc PrelimsDocument38 pages2000 Upsc PrelimsAmritpal BhagatNo ratings yet

- The Multiplier Effect in SingaporeDocument6 pagesThe Multiplier Effect in SingaporeMichael LohNo ratings yet

- EC201 Tutorial Exercise 3 SolutionDocument6 pagesEC201 Tutorial Exercise 3 SolutionPriyaDarshani100% (1)

- Service Management: SMG 301 Spring 2015Document10 pagesService Management: SMG 301 Spring 2015Aboubakr SoultanNo ratings yet

- Status of Solid Waste Management in The Philippines: Alicia L. Castillo " Suehiro Otoma University of Kitakyushu, JapanDocument3 pagesStatus of Solid Waste Management in The Philippines: Alicia L. Castillo " Suehiro Otoma University of Kitakyushu, JapanPrietos KyleNo ratings yet

- Sea-Land Services, Inc. vs. Court of Appeals (April 30, 2001)Document5 pagesSea-Land Services, Inc. vs. Court of Appeals (April 30, 2001)Che Poblete CardenasNo ratings yet

- Qei 18193271Document3 pagesQei 18193271Hernan RomeroNo ratings yet

- Financial Times Europe August 222020Document46 pagesFinancial Times Europe August 222020HoangNo ratings yet

- Apm E170Document130 pagesApm E170FigueiredoNo ratings yet

- Environmental ImpactDocument2 pagesEnvironmental ImpactAadhan AviniNo ratings yet

- Labour Unrest at Honda MotorcyclesDocument7 pagesLabour Unrest at Honda MotorcyclesMayuri Das0% (1)

- State Wise Installed Capacity As On 30.06.2019Document2 pagesState Wise Installed Capacity As On 30.06.2019Bhom Singh NokhaNo ratings yet

- I Defenition of Currency 2Document17 pagesI Defenition of Currency 2HAPSAH HARIANTINo ratings yet

- Print Out 13Document1 pagePrint Out 13Taliyow AlowNo ratings yet