You might also like

- Assumptions - : Cash Flow From Operations $ 0Document4 pagesAssumptions - : Cash Flow From Operations $ 0Krish HegdeNo ratings yet

- Foreign Exchange Hedging Strategies at GDocument11 pagesForeign Exchange Hedging Strategies at GGautam BindlishNo ratings yet

- Case Music MartDocument23 pagesCase Music MartDarwin Dionisio Clemente75% (4)

- 1CKCDocument44 pages1CKCsema2210100% (1)

- Music Mart SolutionDocument6 pagesMusic Mart SolutionStranger Sinha50% (2)

- Dispensers of California Case AnalysisDocument10 pagesDispensers of California Case AnalysisAvinash Singh100% (1)

- Problem 4-4 Dindorf CompanyDocument5 pagesProblem 4-4 Dindorf Companymelati50% (4)

- Lone Pine Cafe-CaseDocument28 pagesLone Pine Cafe-CaseNadya Rizkita100% (2)

- Maynard CompanyDocument5 pagesMaynard CompanyNikitha Andrea SaldanhaNo ratings yet

- Case Baron CoburgDocument8 pagesCase Baron CoburgDarwin Dionisio Clemente100% (2)

- Solution For Lone Pine Cafe CaseDocument5 pagesSolution For Lone Pine Cafe CaseShammika Krishna75% (4)

- Case 2-2 Music Mart Balance Sheet 1 OctDocument5 pagesCase 2-2 Music Mart Balance Sheet 1 OctAnubhav Jha100% (3)

- 01 Ribbons N' Bows - SolutionDocument4 pages01 Ribbons N' Bows - SolutionShivam Kanojia100% (2)

- Accounting-Lone Pine Cafe CaseDocument28 pagesAccounting-Lone Pine Cafe CaseMuadz Akbar100% (1)

- Case Study 4 3 Copies ExpressDocument7 pagesCase Study 4 3 Copies Expressamitsemt100% (2)

- Maynard Company (A) : EXHIBIT 1 Account BalancesDocument2 pagesMaynard Company (A) : EXHIBIT 1 Account Balancesriya lakhotiaNo ratings yet

- CASE 4-1 PC DepotDocument7 pagesCASE 4-1 PC Depotkimhyunna75% (4)

- Case 2-3 Lone Pine Café (A)Document15 pagesCase 2-3 Lone Pine Café (A)Cynthia Anggi Maulina100% (1)

- Accounting:Text and Cases 2-1 & 2-3Document3 pagesAccounting:Text and Cases 2-1 & 2-3Mon Louie Ferrer100% (5)

- Child Welfare QuizDocument2 pagesChild Welfare Quizapi-253825198No ratings yet

- Octane Service StationDocument8 pagesOctane Service StationKalyan Kumar83% (6)

- Problem 3-1Document2 pagesProblem 3-1Omar CirunayNo ratings yet

- Case Report - Grenell FarmDocument5 pagesCase Report - Grenell Farmajsibal100% (1)

- ACCOUNTING STERN CORPORATION (A) AnswerDocument4 pagesACCOUNTING STERN CORPORATION (A) AnswerPradina RachmadiniNo ratings yet

- QED Electronics - Problem 3.7Document1 pageQED Electronics - Problem 3.7ivanyongforexNo ratings yet

- Overhauling Air Compressor On ShipsDocument12 pagesOverhauling Air Compressor On ShipsTun Lin Naing100% (3)

- Case 3.1Document2 pagesCase 3.1Sandeep Agrawal100% (6)

- Investment DetectiveDocument5 pagesInvestment DetectiveNadya Rizkita100% (1)

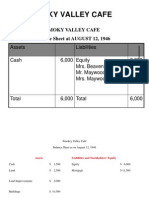

- Smoky Valley CafeDocument3 pagesSmoky Valley Cafemohit_namanNo ratings yet

- Case 5 Joan Holtz Answer KeyDocument5 pagesCase 5 Joan Holtz Answer KeyVira CastroNo ratings yet

- Dispensers of CaliforniaDocument4 pagesDispensers of CaliforniaShweta GautamNo ratings yet

- Case Forest City Tennis ClubDocument9 pagesCase Forest City Tennis ClubAhmedNiaz100% (1)

- Case 4 2Document5 pagesCase 4 2Marjorie Morada67% (3)

- Lewis Corporation Assignment Case 6-2 KTMDocument7 pagesLewis Corporation Assignment Case 6-2 KTMSudeep ShahNo ratings yet

- Problem 2-2: J.L. Gregory CompanyDocument5 pagesProblem 2-2: J.L. Gregory CompanyKAPIL MBA 2021-23 (Delhi)No ratings yet

- Atlas of Pollen and Spores and Their Parent Taxa of MT Kilimanjaro and Tropical East AfricaDocument86 pagesAtlas of Pollen and Spores and Their Parent Taxa of MT Kilimanjaro and Tropical East AfricaEdilson Silva100% (1)

- Lone Pine CafeDocument4 pagesLone Pine CafeRahul TiwariNo ratings yet

- 2-1 Maynard Company (A)Document1 page2-1 Maynard Company (A)Tarry Berry75% (4)

- Waltham Oil and Lube WorkingsDocument5 pagesWaltham Oil and Lube WorkingsGaurav Sahu100% (1)

- Activity Exemplar - Emails For The Release PlanDocument4 pagesActivity Exemplar - Emails For The Release PlanMartinAlexisGonzálezVidal100% (1)

- Maynard Company (A & B)Document9 pagesMaynard Company (A & B)akashnathgarg0% (1)

- XXXXXDocument38 pagesXXXXXGarrett HughesNo ratings yet

- Marion Boats Assignment 2 LatestDocument2 pagesMarion Boats Assignment 2 LatestRakesh SkaiNo ratings yet

- Income Statements 2010Document10 pagesIncome Statements 2010Shivam GoelNo ratings yet

- Maria Hernandez Chemalite and Thumbs Up Case Study FinancialsDocument7 pagesMaria Hernandez Chemalite and Thumbs Up Case Study FinancialsTara AkinteweNo ratings yet

- Lewis Corporation Case 6-2 - Group 5Document8 pagesLewis Corporation Case 6-2 - Group 5Om Prakash100% (1)

- Waltham Oil Lube Centre Inc - FinalDocument10 pagesWaltham Oil Lube Centre Inc - Finalerarun2267% (3)

- Primus Case SolutionDocument28 pagesPrimus Case SolutionNadya Rizkita100% (1)

- Campus PizzeriaDocument12 pagesCampus PizzeriaSHIVAM SRIVASTAVANo ratings yet

- Problem CH 11 Alfi Dan Yessy AKT 18-MDocument4 pagesProblem CH 11 Alfi Dan Yessy AKT 18-MAna Kristiana100% (1)

- Capital Budgeting DCFDocument38 pagesCapital Budgeting DCFNadya Rizkita100% (4)

- Case 4-4 Waltham Oil & Lube Center, Inc.: $40,000 Deposit With NationalDocument5 pagesCase 4-4 Waltham Oil & Lube Center, Inc.: $40,000 Deposit With NationalCyd Marie VictorianoNo ratings yet

- Lone Pine CafeDocument13 pagesLone Pine CafeCynthia Anggi Maulina100% (1)

- Lone Pine Cafe QuestionDocument2 pagesLone Pine Cafe QuestionSahil JainNo ratings yet

- Lone Pine Cafe SolutionDocument5 pagesLone Pine Cafe SolutionRitu ChhipaNo ratings yet

- Case Study 4 - 3 Copies ExpressDocument8 pagesCase Study 4 - 3 Copies ExpressJZ0% (1)

- Waltham Oil and Lube CentreDocument5 pagesWaltham Oil and Lube CentreAnirudh Singh0% (2)

- Case 9-2 Innovative Engineering CoDocument4 pagesCase 9-2 Innovative Engineering CoFaizal PradhanaNo ratings yet

- WCM QuestionsDocument5 pagesWCM QuestionsBhavin BaxiNo ratings yet

- Maria HernandezDocument2 pagesMaria HernandezUjwal Suri100% (1)

- Case1 1,1 2,2 1,2 2,2 3,3 1,3 2,4 1,4 2,5 1 pb2 6,3 9Document20 pagesCase1 1,1 2,2 1,2 2,2 3,3 1,3 2,4 1,4 2,5 1 pb2 6,3 9amyth_dude_9090100% (2)

- Ram Traders - NidhiDocument5 pagesRam Traders - NidhinidhidNo ratings yet

- Cash Flow StatementDocument4 pagesCash Flow StatementRavina Singh100% (1)

- Grennell Farm SolutionDocument6 pagesGrennell Farm SolutionMichael TorresNo ratings yet

- Lone - Pine - Cafe - Case - Study Final XXDocument25 pagesLone - Pine - Cafe - Case - Study Final XXRamesh SinghNo ratings yet

- Lone Pine CafeDocument16 pagesLone Pine CafeJayraj KhuntiNo ratings yet

- Lone Pine CafeDocument16 pagesLone Pine CafeJayraj KhuntiNo ratings yet

- Basic Concepts of Accounting (Balance Sheet)Document12 pagesBasic Concepts of Accounting (Balance Sheet)badtzmaru0506No ratings yet

- Prepare A Balance Sheet For The Lone Pine Café As of November 2, 2009Document2 pagesPrepare A Balance Sheet For The Lone Pine Café As of November 2, 2009Lynnard Philip PanesNo ratings yet

- Case Study On "The Lone Pine Cafe": Guided by Dr. Ashish MehtaDocument30 pagesCase Study On "The Lone Pine Cafe": Guided by Dr. Ashish MehtaParmvir SinghNo ratings yet

- BD21060 Aman Assignment3Document3 pagesBD21060 Aman Assignment3Aman KundraBD21060No ratings yet

- Denah KiniDocument1 pageDenah KiniNadya RizkitaNo ratings yet

- Label BiruDocument1 pageLabel BiruNadya RizkitaNo ratings yet

- LaporanmagangDocument46 pagesLaporanmagangNadya RizkitaNo ratings yet

- LaporanmagangDocument46 pagesLaporanmagangNadya RizkitaNo ratings yet

- Resource Allocation and Negotiation ProblemsDocument2 pagesResource Allocation and Negotiation ProblemsNadya RizkitaNo ratings yet

- Risk FinalDocument26 pagesRisk FinalNadya Rizkita100% (1)

- Conclusion: Nadya Rizkita Putri ADocument10 pagesConclusion: Nadya Rizkita Putri ANadya RizkitaNo ratings yet

- BasfDocument4 pagesBasfHimanshuNo ratings yet

- KBLIDocument4 pagesKBLINadya RizkitaNo ratings yet

- Porter Consumer BehaviorDocument1 pagePorter Consumer BehaviorNadya RizkitaNo ratings yet

- Euro Land Case SolutionDocument12 pagesEuro Land Case SolutionNadya RizkitaNo ratings yet

- CASE Krakatau Steel (A)Document20 pagesCASE Krakatau Steel (A)Ariq LoupiasNo ratings yet

- Decision Making: Biases in Probability AssessmentDocument7 pagesDecision Making: Biases in Probability AssessmentNadya RizkitaNo ratings yet

- Case 2 DCF Analysis - Sindikat 2 (Final - Rev)Document22 pagesCase 2 DCF Analysis - Sindikat 2 (Final - Rev)Nadya RizkitaNo ratings yet

- Investment - LeasingDocument5 pagesInvestment - LeasingNadya RizkitaNo ratings yet

- Real EstateDocument32 pagesReal EstateNadya Rizkita100% (1)

- Group 2 - Note On Real Estate InvestmentDocument32 pagesGroup 2 - Note On Real Estate InvestmentNadya RizkitaNo ratings yet

- Primus Investment1Document83 pagesPrimus Investment1Nadya RizkitaNo ratings yet

- DCF AnalysisDocument2 pagesDCF Analysisanon_822236593No ratings yet

- HDYWTCAGDocument29 pagesHDYWTCAGNadya RizkitaNo ratings yet

- WaccDocument33 pagesWaccAnkitNo ratings yet

- Case Selecting SupplierDocument4 pagesCase Selecting SupplierNadya RizkitaNo ratings yet

- Splitting of Moon Into Two Pieces by Prophet Muhammad (Pbuh)Document9 pagesSplitting of Moon Into Two Pieces by Prophet Muhammad (Pbuh)Esha AimenNo ratings yet

- Payment Item Charges (RM) Discount (RM) Service Tax (RM) Payment Method Final Charges (RM)Document1 pagePayment Item Charges (RM) Discount (RM) Service Tax (RM) Payment Method Final Charges (RM)Md IsmailNo ratings yet

- SUMMATIVE Entrep Q1Document2 pagesSUMMATIVE Entrep Q1ocsapwaketsNo ratings yet

- Reviewer in Gen 001 (P2)Document2 pagesReviewer in Gen 001 (P2)bonellyeyeNo ratings yet

- Tesla Roadster (A) 2014Document25 pagesTesla Roadster (A) 2014yamacNo ratings yet

- Digital Marketing - Scope Opportunities and Challenges - IntechOpen PDFDocument31 pagesDigital Marketing - Scope Opportunities and Challenges - IntechOpen PDFPratsNo ratings yet

- Real Estate in IndiaDocument6 pagesReal Estate in IndiaVikrant KarhadkarNo ratings yet

- Hamlet Greek TragedyDocument21 pagesHamlet Greek TragedyJorge CanoNo ratings yet

- Krok 1 Stomatology: Test Items For Licensing ExaminationDocument28 pagesKrok 1 Stomatology: Test Items For Licensing ExaminationhelloNo ratings yet

- Coronavirus Disease (COVID-19) : Situation Report - 125Document17 pagesCoronavirus Disease (COVID-19) : Situation Report - 125CityNewsTorontoNo ratings yet

- Chraj 1Document6 pagesChraj 1The Independent GhanaNo ratings yet

- Synonyms, Antonyms, Spelling CorrectionsDocument10 pagesSynonyms, Antonyms, Spelling CorrectionsVenkateswara RasupalliNo ratings yet

- Code No.: Etit 401 L T C Paper: Advanced Computer Networks 3 1 4Document4 pagesCode No.: Etit 401 L T C Paper: Advanced Computer Networks 3 1 4Han JeeNo ratings yet

- Rebrand and Relaunch Hydrox CookiesDocument9 pagesRebrand and Relaunch Hydrox CookiesAruba KhanNo ratings yet

- (PRE-TEST) UPCAT Review 2014 - Math Questionnaire-1Document7 pages(PRE-TEST) UPCAT Review 2014 - Math Questionnaire-1Strawberry PancakeNo ratings yet

- Erinnerungsmotive in Wagner's Der Ring Des NibelungenDocument14 pagesErinnerungsmotive in Wagner's Der Ring Des NibelungenLaur MatysNo ratings yet

- 21st CENTURY LIT (ILOCOS DEITIES)Document2 pages21st CENTURY LIT (ILOCOS DEITIES)Louise GermaineNo ratings yet

- Critical Methodology Analysis: 360' Degree Feedback: Its Role in Employee DevelopmentDocument3 pagesCritical Methodology Analysis: 360' Degree Feedback: Its Role in Employee DevelopmentJatin KaushikNo ratings yet

- Baywatch - Tower of PowerDocument20 pagesBaywatch - Tower of Powerkazimkoroglu@hotmail.comNo ratings yet

- Guidelines: VSBK Design OptionDocument60 pagesGuidelines: VSBK Design OptionChrisNo ratings yet

- Greetings From Freehold: How Bruce Springsteen's Hometown Shaped His Life and WorkDocument57 pagesGreetings From Freehold: How Bruce Springsteen's Hometown Shaped His Life and WorkDavid WilsonNo ratings yet

- FijiTimes - June 7 2013Document48 pagesFijiTimes - June 7 2013fijitimescanadaNo ratings yet

- Principles of DTP Design NotesDocument11 pagesPrinciples of DTP Design NotesSHADRACK KIRIMINo ratings yet

- Assessment of The Role of Radio in The Promotion of Community Health in Ogui Urban Area, EnuguDocument21 pagesAssessment of The Role of Radio in The Promotion of Community Health in Ogui Urban Area, EnuguPst W C PetersNo ratings yet