You might also like

- Sebi Takeover Code: Trigger Point For Making Open Offer by "Public AnnouncementDocument4 pagesSebi Takeover Code: Trigger Point For Making Open Offer by "Public AnnouncementgauravkolNo ratings yet

- Takeover CodeDocument9 pagesTakeover CodecitunairNo ratings yet

- MACR-05 - SEBI Takeover CodeDocument29 pagesMACR-05 - SEBI Takeover CodeVivek KuchhalNo ratings yet

- Substantial Acquisition of Shares & Takeovers Regulations, 2011Document18 pagesSubstantial Acquisition of Shares & Takeovers Regulations, 2011Ravi JaiswalNo ratings yet

- Takeover CodeDocument27 pagesTakeover CodeacmrameshNo ratings yet

- Presentation ON Takeovers: Ragini Chokshi & AssociatesDocument34 pagesPresentation ON Takeovers: Ragini Chokshi & Associatesvivian j thomasNo ratings yet

- Promoters' Contribution-1Document13 pagesPromoters' Contribution-1Manali RanaNo ratings yet

- Legal Aspect of M&aDocument7 pagesLegal Aspect of M&apranavnickNo ratings yet

- Top 3 SEBI Orders Under The Takeover Code in The Year 2017Document11 pagesTop 3 SEBI Orders Under The Takeover Code in The Year 2017dhruv vashisthNo ratings yet

- Buy-Back Process Under Companies Act & RulesDocument8 pagesBuy-Back Process Under Companies Act & Rulesdevendra bankarNo ratings yet

- Sast Regulations, 2011Document28 pagesSast Regulations, 2011Ekansh TiwariNo ratings yet

- Procedures of Mergers and Acquisition in IndiaDocument10 pagesProcedures of Mergers and Acquisition in IndiaVignesh KymalNo ratings yet

- Buyback of Shares Vis-A-Vis M&aDocument21 pagesBuyback of Shares Vis-A-Vis M&aDrRajesh GanatraNo ratings yet

- ProvisionsDocument18 pagesProvisionsSimpy BharotNo ratings yet

- SEBI Guidelines For Public IssueDocument28 pagesSEBI Guidelines For Public IssueSuraj KumarNo ratings yet

- ProspectusDocument26 pagesProspectusLogesh JanagarajNo ratings yet

- 4 5817600036418093605 PDFDocument4 pages4 5817600036418093605 PDFNaga ChandraNo ratings yet

- 6 CLSP ProspectusDocument5 pages6 CLSP ProspectusSyed Mujtaba HassanNo ratings yet

- Advanced Financial Accounting: An Outlook On The Process and The How It Was Implemented byDocument9 pagesAdvanced Financial Accounting: An Outlook On The Process and The How It Was Implemented byNishant AjitsariaNo ratings yet

- Companies Act 2013Document15 pagesCompanies Act 2013biplav2uNo ratings yet

- SEBI (ICDR) Regulations ChecklistDocument18 pagesSEBI (ICDR) Regulations ChecklistbkpforgauravNo ratings yet

- Issue of WarrantsDocument1 pageIssue of WarrantsDhruvi KothariNo ratings yet

- Right of First Refusal To Significant Holders. The Company Hereby Grants To Each InvestorDocument11 pagesRight of First Refusal To Significant Holders. The Company Hereby Grants To Each InvestorshirdhiNo ratings yet

- SEBI Takeover Regulation 2011Document9 pagesSEBI Takeover Regulation 2011Himanshu AggarwalNo ratings yet

- BuybackDocument3 pagesBuybackroutraykhushbooNo ratings yet

- Sebi Mergers & Acquisitions: Eira KochharDocument26 pagesSebi Mergers & Acquisitions: Eira Kochhareira kNo ratings yet

- Supplementary Paper 13Document9 pagesSupplementary Paper 13Ram2289No ratings yet

- Buy Back Regulation 2018Document15 pagesBuy Back Regulation 2018Ranjana YadavNo ratings yet

- Takeover CodeDocument20 pagesTakeover CodeMahimna KandpalNo ratings yet

- Buy Back of SecuritiesDocument5 pagesBuy Back of SecuritiesRishi ShrivastavaNo ratings yet

- SEBI Regulation 2009Document68 pagesSEBI Regulation 2009Anil KingNo ratings yet

- CH 6 Takeover Strategies and PracticeDocument64 pagesCH 6 Takeover Strategies and PracticeHaritika ChhatwalNo ratings yet

- Accounts I ProjectDocument6 pagesAccounts I ProjectUrvi ShahNo ratings yet

- 6 Updates Buy Back of SecDocument14 pages6 Updates Buy Back of SecsanathgowdaNo ratings yet

- IBA SQ-Out Singapore 2014 (VFP)Document6 pagesIBA SQ-Out Singapore 2014 (VFP)verna_goh_shileiNo ratings yet

- Initial Public OfferingDocument9 pagesInitial Public OfferingAnji UpparaNo ratings yet

- FI Warrant - Quebec - FormDocument16 pagesFI Warrant - Quebec - FormMarkogarciamtzNo ratings yet

- The ICDR Regulations Act, 2009Document11 pagesThe ICDR Regulations Act, 2009Twinkle KillaNo ratings yet

- SEBI Takeover Code - UpdatedDocument24 pagesSEBI Takeover Code - UpdatedSagarNo ratings yet

- Buy Back of SharesDocument7 pagesBuy Back of SharesChandan Kumar TripathyNo ratings yet

- Section 42, The Companies Act, 2013Document4 pagesSection 42, The Companies Act, 2013Damon SalvatoreNo ratings yet

- Securities and Exchange Commission of Pakistan: Statutory Notifications (S.R.O.) Government of PakistanDocument9 pagesSecurities and Exchange Commission of Pakistan: Statutory Notifications (S.R.O.) Government of PakistanjeddyammarNo ratings yet

- Procedural Checklist For Buyback of Shares by An Unlisted CompanyDocument8 pagesProcedural Checklist For Buyback of Shares by An Unlisted CompanyRamji SukumarNo ratings yet

- Prospectus, Allotment of Securities and Private Placement Co Act 2013 BGDocument5 pagesProspectus, Allotment of Securities and Private Placement Co Act 2013 BGachuthan100% (1)

- Sebi Issue of Capital and DisclosureDocument37 pagesSebi Issue of Capital and DisclosureDev Kum AgnishNo ratings yet

- Qualified Institutional Placement QIP ProcedureDocument5 pagesQualified Institutional Placement QIP ProcedurerohanbhawsarNo ratings yet

- CMS PPT 2Document9 pagesCMS PPT 2rashi bakshNo ratings yet

- 7 ProspectusDocument8 pages7 ProspectusVarun BhomiaNo ratings yet

- Buy Back of SharesDocument3 pagesBuy Back of SharesNagalakshmi ChagantiNo ratings yet

- Buy Back of Shares Under The Companies Act, 1956 - An InsightDocument4 pagesBuy Back of Shares Under The Companies Act, 1956 - An InsightHrdk DveNo ratings yet

- Delinquent SubscriptionDocument3 pagesDelinquent SubscriptionAudrey BienNo ratings yet

- Buy Back of SharesDocument32 pagesBuy Back of SharesSiddhant Raj PandeyNo ratings yet

- SEBI (Substantial Acquisition of Shares and Takeovers) Regulations, 2011 - Some Key FeaturesDocument6 pagesSEBI (Substantial Acquisition of Shares and Takeovers) Regulations, 2011 - Some Key FeaturesJimlee DasNo ratings yet

- Legal Aspects M & ADocument15 pagesLegal Aspects M & ATwinkal chakradhari100% (1)

- Sebi (Icdr), 2018Document63 pagesSebi (Icdr), 2018Vedant KshatriyaNo ratings yet

- Public Issue Rules 2015Document10 pagesPublic Issue Rules 2015tusher pepolNo ratings yet

- FI Subscription Agreement - Mexico - v4Document14 pagesFI Subscription Agreement - Mexico - v4rrCarvalloNo ratings yet

- Crowdfunding on SteroidsFrom EverandCrowdfunding on SteroidsRating: 3 out of 5 stars3/5 (1)

- General Solicitation under New Rule 506: Crowd Funding on SteroidsFrom EverandGeneral Solicitation under New Rule 506: Crowd Funding on SteroidsRating: 5 out of 5 stars5/5 (1)

- Merger & Acquisition, JV StrategiesDocument26 pagesMerger & Acquisition, JV StrategiesRohit SutharNo ratings yet

- RM Gtu TheoryDocument4 pagesRM Gtu TheoryAtibAhmedNo ratings yet

- Mutual FundDocument10 pagesMutual FundSimmi KhuranaNo ratings yet

- Presentation Slides: Contemporary Strategy Analysis: Concepts, Techniques, ApplicationsDocument11 pagesPresentation Slides: Contemporary Strategy Analysis: Concepts, Techniques, ApplicationsAbhishek EshwarNo ratings yet

- Chapter 3 Money Management StrategyDocument28 pagesChapter 3 Money Management StrategyRohit SutharNo ratings yet

- Chapter-1 Indian Contract Act 1872Document100 pagesChapter-1 Indian Contract Act 1872aahana77No ratings yet

- Security Analysis and Portfolio ManagementDocument14 pagesSecurity Analysis and Portfolio ManagementRohit SutharNo ratings yet

- Fabm2 - Statement of Comprehensive Income (Practice Problems) - Answer KeyDocument3 pagesFabm2 - Statement of Comprehensive Income (Practice Problems) - Answer KeyMounicha Ambayec100% (4)

- 3 - Valuation of Equity Shares - Assignment (26-04-19)Document4 pages3 - Valuation of Equity Shares - Assignment (26-04-19)AakashNo ratings yet

- Berkshire's Corporate Performance vs. The S&P 500Document23 pagesBerkshire's Corporate Performance vs. The S&P 500FirstpostNo ratings yet

- Books of Accounts Double Entry System With Answers by AlagangwencyDocument4 pagesBooks of Accounts Double Entry System With Answers by AlagangwencyHello KittyNo ratings yet

- British Lyceum ChallanDocument1 pageBritish Lyceum ChallanKamran JalilNo ratings yet

- Chapter 4 Uses and Sources of STF and LTFDocument49 pagesChapter 4 Uses and Sources of STF and LTFChristopher Beltran CauanNo ratings yet

- Cost and Benefit Analysis BookDocument361 pagesCost and Benefit Analysis Book9315875729100% (7)

- VPS Form SampleDocument7 pagesVPS Form SampleMuhammad ShariqNo ratings yet

- List of Courses 20-21 - 1Document19 pagesList of Courses 20-21 - 1Why WhyNo ratings yet

- Assignment 2 POF Muhammad Yaseen (48535)Document5 pagesAssignment 2 POF Muhammad Yaseen (48535)Muhammad Yaseen ShiekhNo ratings yet

- Application GuideDocument130 pagesApplication GuideValentin DobchevNo ratings yet

- Module 2 - Risk Management ProcessDocument13 pagesModule 2 - Risk Management ProcessLara Camille CelestialNo ratings yet

- SM1001904 Chapter-5 Caselets PDFDocument4 pagesSM1001904 Chapter-5 Caselets PDFsai bhargavNo ratings yet

- 01 CA Inter Audit Question Bank Part 1 Chapter 0 To Chapter 3Document146 pages01 CA Inter Audit Question Bank Part 1 Chapter 0 To Chapter 3Yash SharmaNo ratings yet

- Accounting Installment LiquidationDocument11 pagesAccounting Installment LiquidationElkie pabia RualNo ratings yet

- Foreign Exchange Rate Sheet: Bulletin November 29, 2021Document1 pageForeign Exchange Rate Sheet: Bulletin November 29, 2021Zeeshan AtharNo ratings yet

- In The Partial Fulfillment of The Requirement For The Award of Degree inDocument17 pagesIn The Partial Fulfillment of The Requirement For The Award of Degree inMohmmedKhayyumNo ratings yet

- Transaction Summary - 10 July 2021 To 6 August 2021: Together We Make A DifferenceDocument2 pagesTransaction Summary - 10 July 2021 To 6 August 2021: Together We Make A Differencebertha kiaraNo ratings yet

- Capital Structure Policy I Ebit-Eps Analysis: Page 1 of 2Document2 pagesCapital Structure Policy I Ebit-Eps Analysis: Page 1 of 2Danzo ShahNo ratings yet

- Learning Objectives: Assets Liabilities + EquityDocument13 pagesLearning Objectives: Assets Liabilities + EquityAira AbigailNo ratings yet

- STD 11 Business Studies ModelDocument2 pagesSTD 11 Business Studies ModelArs BokaroNo ratings yet

- Financial DerivativesDocument31 pagesFinancial DerivativesSyed Roshan JavedNo ratings yet

- Securities Regulation HyposDocument46 pagesSecurities Regulation HyposErin JacksonNo ratings yet

- LJK UkkDocument55 pagesLJK UkkSaepul RohmanNo ratings yet

- Audit of Cash Audit Program For CashDocument5 pagesAudit of Cash Audit Program For CashLyka Mae Palarca IrangNo ratings yet

- Cover LetterDocument2 pagesCover LetterBilal AslamNo ratings yet

- Basic Details: Indian Oil Corporation Eprocurement PortalDocument3 pagesBasic Details: Indian Oil Corporation Eprocurement PortalamitjustamitNo ratings yet

- Junior Accountant RoleDocument1 pageJunior Accountant RoleRICARDO PROMOTIONNo ratings yet

- BUS 330 Exam 1 - Fall 2012 (B) - SolutionDocument14 pagesBUS 330 Exam 1 - Fall 2012 (B) - SolutionTao Chun LiuNo ratings yet

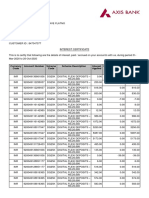

- Interest CertificateDocument2 pagesInterest CertificatesumitNo ratings yet