You might also like

- Financial Inclusion for Micro, Small, and Medium Enterprises in Kazakhstan: ADB Support for Regional Cooperation and Integration across Asia and the Pacific during Unprecedented Challenge and ChangeFrom EverandFinancial Inclusion for Micro, Small, and Medium Enterprises in Kazakhstan: ADB Support for Regional Cooperation and Integration across Asia and the Pacific during Unprecedented Challenge and ChangeNo ratings yet

- 6-A-Card - Concpet Paper For Usaid 9 Nov 2016-FinalDocument6 pages6-A-Card - Concpet Paper For Usaid 9 Nov 2016-FinalGyanendra SinghNo ratings yet

- Danish Muzzafar Amjadkhan Ali Ammar Maitla Inam-Ul Haque RanaDocument21 pagesDanish Muzzafar Amjadkhan Ali Ammar Maitla Inam-Ul Haque RanaChiken BurgerNo ratings yet

- A Report On Trends in Banking & Retail BankingDocument5 pagesA Report On Trends in Banking & Retail BankingJyothi SahuNo ratings yet

- Agency BankingDocument4 pagesAgency BankingASHEHU SANI100% (1)

- What Is An Agent Bank?Document6 pagesWhat Is An Agent Bank?hossain al fuad tusharNo ratings yet

- Icici and YahooDocument12 pagesIcici and YahooPavan AhujaNo ratings yet

- Innovation in Banking SectorDocument6 pagesInnovation in Banking SectorKashishNo ratings yet

- 13 - Conclusion and SuggestionsDocument4 pages13 - Conclusion and SuggestionsjothiNo ratings yet

- UPI For Feature Phones - Blog - BhavyaDocument5 pagesUPI For Feature Phones - Blog - BhavyaBhavya SolankiNo ratings yet

- Guidelines On Mobile Financial ServicesDocument4 pagesGuidelines On Mobile Financial ServicesAhsan ZamanNo ratings yet

- Capital First Limited ProjectDocument74 pagesCapital First Limited Projectbiranchi behera100% (1)

- Agent BankingDocument7 pagesAgent BankingNaymur Rahman100% (1)

- Operating Circular For RuPay Credit Cards Linked To UPIDocument4 pagesOperating Circular For RuPay Credit Cards Linked To UPIakshay_blitzNo ratings yet

- Team 121 ProposalDocument9 pagesTeam 121 ProposalRozin CeausescuNo ratings yet

- Payment Card August 31Document104 pagesPayment Card August 31girishchanduNo ratings yet

- 19bbl098, 19bbl110 - Law On Corporate FinanceDocument7 pages19bbl098, 19bbl110 - Law On Corporate FinanceBhumihar Shubham TejasNo ratings yet

- Introduction To Financial InclusionDocument9 pagesIntroduction To Financial Inclusionmahaseth2008100% (1)

- Why People Should Shift Towards The Digital Bank?Document3 pagesWhy People Should Shift Towards The Digital Bank?sarthak25No ratings yet

- How Has Digital Lending ImpactedDocument11 pagesHow Has Digital Lending ImpactedrofirheinNo ratings yet

- What Is A Textile Recycling Business?Document4 pagesWhat Is A Textile Recycling Business?LAVANYA KOTHANo ratings yet

- Mobile Banking Products and Rural India: An Evaluation: Peter JohnDocument5 pagesMobile Banking Products and Rural India: An Evaluation: Peter JohnkarthickNo ratings yet

- Convergence of Mobile Banking, Financial Inclusion and Consumer Protection-TrendDocument3 pagesConvergence of Mobile Banking, Financial Inclusion and Consumer Protection-TrendCiocoiu Vlad AndreiNo ratings yet

- Utilizing Technology and Innovation in Agri Enterprise Financing - 062121Document11 pagesUtilizing Technology and Innovation in Agri Enterprise Financing - 062121Romnick Pascua TuboNo ratings yet

- Micro BankingDocument6 pagesMicro BankingPratik SavaliaNo ratings yet

- Important RationalsDocument37 pagesImportant RationalsSalil JoshiNo ratings yet

- Financing and Developing PACSDocument3 pagesFinancing and Developing PACSSadaf KushNo ratings yet

- Module - Business Correspondent and FacilitatorDocument80 pagesModule - Business Correspondent and FacilitatorVaibhavNo ratings yet

- CXGO Report Financial Inclusion June 2018Document17 pagesCXGO Report Financial Inclusion June 2018Meygantara Faozal HNo ratings yet

- NABARDDocument40 pagesNABARDJesse LarsenNo ratings yet

- Bangladesh Bank Guidelines On Mobile BankingDocument11 pagesBangladesh Bank Guidelines On Mobile BankingIshtiaq Oni RahmanNo ratings yet

- Banking Industry-Final Report Group 18Document14 pagesBanking Industry-Final Report Group 18Pranav KumarNo ratings yet

- What Is A Kisan Credit Card?Document5 pagesWhat Is A Kisan Credit Card?bhaskar sarmaNo ratings yet

- Innovations in Insurance SectorDocument34 pagesInnovations in Insurance SectorKashishNo ratings yet

- Project Report "Banking System" in India Introduction of BankingDocument27 pagesProject Report "Banking System" in India Introduction of BankingShruti GargNo ratings yet

- Final E-Banking Concept PaperDocument9 pagesFinal E-Banking Concept PaperGerlie Ann MendozaNo ratings yet

- Unit 5 Andhra Pradesh.Document18 pagesUnit 5 Andhra Pradesh.Charu ModiNo ratings yet

- 7 Ps of Microfinance in Rural IndiaDocument2 pages7 Ps of Microfinance in Rural IndiaVaibhav Wadhwa0% (1)

- Types of Payment Systems and InstrumentsDocument6 pagesTypes of Payment Systems and Instrumentstushar guptaNo ratings yet

- DD-Digital ProductsDocument58 pagesDD-Digital ProductsFaded JadedNo ratings yet

- Growth of Consumer Financing in PakistanDocument7 pagesGrowth of Consumer Financing in Pakistannimra khaliqNo ratings yet

- Drivers and Technology - MOBDocument4 pagesDrivers and Technology - MOBSehgal AnkitNo ratings yet

- Banking Project: Name-Sanika Patil Class - Fybcom Div-B ROLL NO - 216Document15 pagesBanking Project: Name-Sanika Patil Class - Fybcom Div-B ROLL NO - 216sanika patilNo ratings yet

- Study of Mobiles WalletsDocument42 pagesStudy of Mobiles WalletsVijay TendolkarNo ratings yet

- Thesis On Kisan Credit CardDocument8 pagesThesis On Kisan Credit Cardquaobiikd100% (1)

- Need For MicrofinanceDocument52 pagesNeed For MicrofinancePrasad KumarNo ratings yet

- Cust - Support - 2023 - REPORT - 1687583135 2023-06-24 05 - 05 - 41Document19 pagesCust - Support - 2023 - REPORT - 1687583135 2023-06-24 05 - 05 - 41Sohail ShaikhNo ratings yet

- Microfinance-Financial Intermediation (Students Notes)Document4 pagesMicrofinance-Financial Intermediation (Students Notes)MIRADOR ACCOUNTANTS KENYANo ratings yet

- Financial InclusionDocument28 pagesFinancial InclusionrajjinonuNo ratings yet

- Retail BankingDocument6 pagesRetail Bankingtejasvgahlot05No ratings yet

- Indian Banking Industry-Customer Satisfaction & PreferencesDocument12 pagesIndian Banking Industry-Customer Satisfaction & PreferencesakankaroraNo ratings yet

- Jan Dhan Yojana Article Full PDFDocument4 pagesJan Dhan Yojana Article Full PDFAmitanshu VishalNo ratings yet

- Project Report "Banking System" in India Introduction of BankingDocument9 pagesProject Report "Banking System" in India Introduction of BankingmanishteensNo ratings yet

- Agent BankingDocument5 pagesAgent BankingAnik SarkarNo ratings yet

- Standup & Mudra India2Document13 pagesStandup & Mudra India2anandrathiraj25No ratings yet

- Jan Dhan Yojana Article Full PDFDocument4 pagesJan Dhan Yojana Article Full PDFAmit KumarNo ratings yet

- Mobile BankingDocument44 pagesMobile Bankingpraveen_rautelaNo ratings yet

- T R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)From EverandT R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)No ratings yet

- Agent Banking Uganda Handbook: A simple guide to starting and running a profitable agent banking business in UgandaFrom EverandAgent Banking Uganda Handbook: A simple guide to starting and running a profitable agent banking business in UgandaNo ratings yet

- Story Splitting Cheat SheetDocument1 pageStory Splitting Cheat Sheetrvijaysubs_764835048No ratings yet

- DFS AgMechanization Aug2017Document69 pagesDFS AgMechanization Aug2017KaziNasirUddinOlyNo ratings yet

- IELTS Research Reports Order Form June07Document3 pagesIELTS Research Reports Order Form June07KaziNasirUddinOlyNo ratings yet

- The Hacker CrackdownDocument238 pagesThe Hacker Crackdownapi-19927444No ratings yet

- AVR Instruction SetDocument150 pagesAVR Instruction SetHugo LoureiroNo ratings yet

- ATmega8 UCDocument308 pagesATmega8 UCemail2suryazNo ratings yet

- SRPDocument6 pagesSRPnaturaleletric8231No ratings yet

- Long Term GoalsDocument1 pageLong Term GoalsKaziNasirUddinOlyNo ratings yet

- ABBRDocument2 pagesABBRRuijia ZengNo ratings yet

- Candidate Contact Information: Election and Information ServicesDocument13 pagesCandidate Contact Information: Election and Information ServicesnmpaccNo ratings yet

- Hotels List in AhmedabadDocument18 pagesHotels List in Ahmedabadreena sharmaNo ratings yet

- Top 100 City Destinations - EuromonitorDocument94 pagesTop 100 City Destinations - EuromonitorIndex.hr100% (3)

- BIS Microsoft Dynamics NAV 2009 Vs NAV 2016Document20 pagesBIS Microsoft Dynamics NAV 2009 Vs NAV 2016mohit1990dodwalNo ratings yet

- Https WWW - Cimb.bizchannel - Com.my Corp Front Transactioninquiry - Do Action Doprint PDFDocument1 pageHttps WWW - Cimb.bizchannel - Com.my Corp Front Transactioninquiry - Do Action Doprint PDFSyed HanafieNo ratings yet

- Public Notice 02 - 2020Document4 pagesPublic Notice 02 - 2020samartha1181No ratings yet

- Sco En590 Cif Plattprice Aswpkr Validity1 31jul2023Document3 pagesSco En590 Cif Plattprice Aswpkr Validity1 31jul2023almaroj alzarqaa100% (1)

- Concepts & Conventions in AccountingDocument5 pagesConcepts & Conventions in Accountingpratz dhakateNo ratings yet

- Nokia Airscale Bts Radio Module Overview: Before We BeginDocument46 pagesNokia Airscale Bts Radio Module Overview: Before We BeginJesus Rafael BastardoNo ratings yet

- Medical Benefits SummaryDocument1 pageMedical Benefits SummaryJanet Zimmerman McNicholNo ratings yet

- Saint Louis University Health Sciences Education Union at Saint Louis University Medical CenterDocument2 pagesSaint Louis University Health Sciences Education Union at Saint Louis University Medical CenterSlusom WebNo ratings yet

- ZoroDocument5 pagesZoroxaiNo ratings yet

- 1548840809911Document8 pages1548840809911GULAB CHANDERNo ratings yet

- Group BrochureDocument9 pagesGroup BrochureSuanjana BiswasNo ratings yet

- Jurnal Pendukung Topik Penelitian - Audit Eks PDFDocument22 pagesJurnal Pendukung Topik Penelitian - Audit Eks PDFAngel HambaliNo ratings yet

- Bay LesDocument29 pagesBay LesViji LakshmiNo ratings yet

- 06 - 2100013699816 - 1364964451 - 20231021 - 1 - Yee Lien Stationery and Trading Co (Mobile)Document7 pages06 - 2100013699816 - 1364964451 - 20231021 - 1 - Yee Lien Stationery and Trading Co (Mobile)polly.ylstationeryNo ratings yet

- SSD ProjectDocument8 pagesSSD ProjectDebjit GangulyNo ratings yet

- Management Accounting: Roll No. Total No. of Pages: 02 Total No. of Questions: 07 - 5)Document2 pagesManagement Accounting: Roll No. Total No. of Pages: 02 Total No. of Questions: 07 - 5)sumanNo ratings yet

- TENDER RFX NO. 2122100065 Supply of Skilled Manpower Services For Works in Generation DivisionDocument3 pagesTENDER RFX NO. 2122100065 Supply of Skilled Manpower Services For Works in Generation Divisionxafajat881No ratings yet

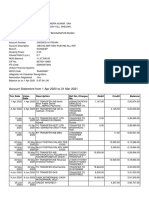

- Account Statement From 1 Apr 2020 To 31 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument3 pagesAccount Statement From 1 Apr 2020 To 31 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceAbhay RajNo ratings yet

- Miranda Mckinney: 70 Huckleberry Lane, Ashville, AL 35953 (205) 532-3980Document2 pagesMiranda Mckinney: 70 Huckleberry Lane, Ashville, AL 35953 (205) 532-3980Chesil Zin Del ValleNo ratings yet

- Datasheet - Cisco Unified Contact Center ExpressDocument9 pagesDatasheet - Cisco Unified Contact Center ExpressNurdheen PeringattilNo ratings yet

- Hsa Compliant Gap Plan: Level-Funded Gap Coverage For Groups With High Deductible Health Insurance PlansDocument2 pagesHsa Compliant Gap Plan: Level-Funded Gap Coverage For Groups With High Deductible Health Insurance PlansamazonrecieptsNo ratings yet

- Organizational Structure of Retail Firm Dr. Anitha PrasadDocument26 pagesOrganizational Structure of Retail Firm Dr. Anitha Prasadanithaprasad100% (2)

- M1 - Introduction To BFSIDocument14 pagesM1 - Introduction To BFSIGeorge BernardNo ratings yet

- NOTESDocument4 pagesNOTESFarrukhsgNo ratings yet

- Your Vi Bill: Rs 299.00 Rs 310.00 Rs 0.00 Rs 299.00 Rs 338.00Document2 pagesYour Vi Bill: Rs 299.00 Rs 310.00 Rs 0.00 Rs 299.00 Rs 338.00Rahul KumarNo ratings yet

- Statement On Standard Auditing Practices (SAP) 24 Audit Considerations Relating To Entities Using Service OrganisationsDocument4 pagesStatement On Standard Auditing Practices (SAP) 24 Audit Considerations Relating To Entities Using Service OrganisationsRishabh GuptaNo ratings yet