You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- ST5 Pu 15 PDFDocument30 pagesST5 Pu 15 PDFPolelarNo ratings yet

- ST7 Pu 15 PDFDocument82 pagesST7 Pu 15 PDFPolelarNo ratings yet

- ST6 Pu 15 PDFDocument60 pagesST6 Pu 15 PDFPolelarNo ratings yet

- ST8 Pu 15 PDFDocument58 pagesST8 Pu 15 PDFPolelarNo ratings yet

- Sa5 Pu 15 PDFDocument52 pagesSa5 Pu 15 PDFPolelarNo ratings yet

- ST4 Pu 15 PDFDocument106 pagesST4 Pu 15 PDFPolelarNo ratings yet

- Ca1 Pu 15 PDFDocument30 pagesCa1 Pu 15 PDFPolelar0% (1)

- Sa4 Pu 15 PDFDocument9 pagesSa4 Pu 15 PDFPolelarNo ratings yet

- ST2 Pu 15 PDFDocument26 pagesST2 Pu 15 PDFPolelarNo ratings yet

- Ca3 Pu 15 PDFDocument10 pagesCa3 Pu 15 PDFPolelarNo ratings yet

- Sa1 Pu 15 PDFDocument78 pagesSa1 Pu 15 PDFPolelarNo ratings yet

- Sa2 Pu 14 PDFDocument150 pagesSa2 Pu 14 PDFPolelarNo ratings yet

- Sa2 Pu 15 PDFDocument108 pagesSa2 Pu 15 PDFPolelarNo ratings yet

- CT7 Pu 15 PDFDocument8 pagesCT7 Pu 15 PDFPolelarNo ratings yet

- ST4 Pu 14 PDFDocument10 pagesST4 Pu 14 PDFPolelarNo ratings yet

- Sa5 Pu 14 PDFDocument102 pagesSa5 Pu 14 PDFPolelarNo ratings yet

- ST8 Pu 14 PDFDocument42 pagesST8 Pu 14 PDFPolelarNo ratings yet

- ST2 Pu 14 PDFDocument26 pagesST2 Pu 14 PDFPolelarNo ratings yet

- ST9 Pu 14 PDFDocument6 pagesST9 Pu 14 PDFPolelarNo ratings yet

- ST7 Pu 14 PDFDocument84 pagesST7 Pu 14 PDFPolelarNo ratings yet

- Sa6 Pu 14 PDFDocument118 pagesSa6 Pu 14 PDFPolelarNo ratings yet

- Sa1 Pu 14 PDFDocument212 pagesSa1 Pu 14 PDFPolelarNo ratings yet

- ST5 Pu 14 PDFDocument12 pagesST5 Pu 14 PDFPolelarNo ratings yet

- ST6 Pu 14 PDFDocument60 pagesST6 Pu 14 PDFPolelarNo ratings yet

- Sa3 Pu 14 PDFDocument114 pagesSa3 Pu 14 PDFPolelarNo ratings yet

- Sa4 Pu 14 PDFDocument36 pagesSa4 Pu 14 PDFPolelarNo ratings yet

- Subject CA2: CMP Upgrade 2013/14Document7 pagesSubject CA2: CMP Upgrade 2013/14PolelarNo ratings yet

- R.C. Sproul and Greg Bahnsen Debate - Greg Bahnsen's IntroductionDocument2 pagesR.C. Sproul and Greg Bahnsen Debate - Greg Bahnsen's IntroductionPolelarNo ratings yet

- Ca3 Pu 14 PDFDocument16 pagesCa3 Pu 14 PDFPolelarNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

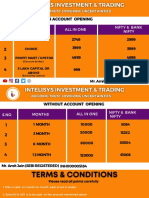

- Intelisys Pricing PlanDocument5 pagesIntelisys Pricing PlanregsNo ratings yet

- E Receipt For State Bank Collect Payment: 13731 Suryansh .Tiwari Ug GN Mme Btech Hall3 156 Suryansh@Iitk - Ac.In 55890 0Document1 pageE Receipt For State Bank Collect Payment: 13731 Suryansh .Tiwari Ug GN Mme Btech Hall3 156 Suryansh@Iitk - Ac.In 55890 0Abhishek KulkarniNo ratings yet

- Jntuk Mba 3rd Sem r13 TT Nov 2016Document1 pageJntuk Mba 3rd Sem r13 TT Nov 2016haibye424No ratings yet

- BaselDocument28 pagesBaselKavithaNo ratings yet

- Class 10 BankingDocument3 pagesClass 10 BankingPATASHIMUL GRAM PACHAYATNo ratings yet

- Audit Class Notes EvidenceDocument15 pagesAudit Class Notes EvidencePrince Wayne SibandaNo ratings yet

- Citi Cards Non Perm Res Al Cre Card AppDocument8 pagesCiti Cards Non Perm Res Al Cre Card AppHarish KrishnaNo ratings yet

- Organogram - State Bank of Pakistan: Approved by The Board On October 26, 2020Document1 pageOrganogram - State Bank of Pakistan: Approved by The Board On October 26, 2020Bilal ZaidiNo ratings yet

- Css Challan Form 2022Document1 pageCss Challan Form 2022SairaNo ratings yet

- FAR 3 Sample QuestionsDocument2 pagesFAR 3 Sample Questionsfrancis dungcaNo ratings yet

- Fixed Deposits - November 12 2018Document1 pageFixed Deposits - November 12 2018Tiso Blackstar GroupNo ratings yet

- Exam3 Buscom T F MC Problems FinalDocument23 pagesExam3 Buscom T F MC Problems FinalErico PaderesNo ratings yet

- Pradhan Mantri Vaya Vandana Plan 842 Form PDFDocument6 pagesPradhan Mantri Vaya Vandana Plan 842 Form PDFDesikan100% (1)

- Financial Analysis of Janata Bank LimitedDocument8 pagesFinancial Analysis of Janata Bank LimitedBirendra Dasaudi100% (1)

- Investment Proof Submission Guidelines 2022-23Document17 pagesInvestment Proof Submission Guidelines 2022-23Rajshree SamantrayNo ratings yet

- Week 6-7 Let's Analyze Acc213Document5 pagesWeek 6-7 Let's Analyze Acc213Swetzi CzeshNo ratings yet

- Private Tibetan Language LessonsDocument5 pagesPrivate Tibetan Language LessonsGuilherme PintadoNo ratings yet

- SIMPLE INTEREST & COMPOUND INTEREST - 1st - Chapter PDFDocument6 pagesSIMPLE INTEREST & COMPOUND INTEREST - 1st - Chapter PDFarasuNo ratings yet

- IT Certificate 2020-21 BajajDocument1 pageIT Certificate 2020-21 BajajPushpendra SinghNo ratings yet

- ACC 311 ReviewDocument2 pagesACC 311 ReviewMaricar DimayugaNo ratings yet

- Term Sheet WhiteDocument3 pagesTerm Sheet WhiteholtfoxNo ratings yet

- INTACCT - Online Modules SummaryDocument3 pagesINTACCT - Online Modules SummarysfsdfsdfNo ratings yet

- Indian Financial MarketDocument114 pagesIndian Financial MarketmilindpreetiNo ratings yet

- 5-10 Fa1Document10 pages5-10 Fa1Shahab ShafiNo ratings yet

- Debt To Total Asset RatioDocument13 pagesDebt To Total Asset RatioMjNo ratings yet

- MR Dolphy D'Souza, Partner, E&YDocument4 pagesMR Dolphy D'Souza, Partner, E&YPradeep Singh100% (1)

- Valuation of BondsDocument30 pagesValuation of BondsRuchi SharmaNo ratings yet

- Module Training Internal Audit HISDocument38 pagesModule Training Internal Audit HISarieznavalNo ratings yet

- Review in General Mathematics (Quiz Bee)Document26 pagesReview in General Mathematics (Quiz Bee)cherrie annNo ratings yet

- Int. Acc 1 Chap 2Document7 pagesInt. Acc 1 Chap 2Nicole Anne Santiago SibuloNo ratings yet