You might also like

- Pack 6 Books in 1 - Flash Cards Pictures and Words English Spanish: 400 Cards - Spanish vocabulary learning flash cards with pictures for beginnersFrom EverandPack 6 Books in 1 - Flash Cards Pictures and Words English Spanish: 400 Cards - Spanish vocabulary learning flash cards with pictures for beginnersNo ratings yet

- HCMF Investor Letter October 2009 FINALDocument24 pagesHCMF Investor Letter October 2009 FINALAbsolute Return100% (1)

- What Is Really Killing The Irish EconomyDocument1 pageWhat Is Really Killing The Irish EconomyLuis Riestra Delgado100% (1)

- Gerald CorcoranDocument9 pagesGerald CorcoranMarketsWikiNo ratings yet

- "Planning Your Financial Future": Mangala Boyagoda 26 October 2010Document71 pages"Planning Your Financial Future": Mangala Boyagoda 26 October 2010Inde Pendent LkNo ratings yet

- Global Commodity Prices, Monetary Transmission, and Exchange Rate Pass-Through in The Pacific IslandsDocument16 pagesGlobal Commodity Prices, Monetary Transmission, and Exchange Rate Pass-Through in The Pacific IslandslukeniaNo ratings yet

- FMG China Fund - PresentationDocument15 pagesFMG China Fund - PresentationSusan AllenNo ratings yet

- November 2008 Update: Why Are Electricity Prices in RTOs Increasingly Expensive?Document8 pagesNovember 2008 Update: Why Are Electricity Prices in RTOs Increasingly Expensive?RobertMcCulloughNo ratings yet

- Florida's September Employment Figures Released: Charlie Crist Cynthia R. LorenzoDocument16 pagesFlorida's September Employment Figures Released: Charlie Crist Cynthia R. LorenzoMichael AllenNo ratings yet

- Florida's July Employment Figures Released: Charlie Crist Cynthia R. LorenzoDocument16 pagesFlorida's July Employment Figures Released: Charlie Crist Cynthia R. LorenzoMichael AllenNo ratings yet

- Russia 2010 Worth A Tactical Look: An Investor's Guide To The Risks and Opportunities in 2010Document21 pagesRussia 2010 Worth A Tactical Look: An Investor's Guide To The Risks and Opportunities in 2010jamesdb1No ratings yet

- Florida's November Employment Figures ReleasedDocument16 pagesFlorida's November Employment Figures ReleasedMichael AllenNo ratings yet

- Update On IDFC Arbitrage FundDocument6 pagesUpdate On IDFC Arbitrage FundGNo ratings yet

- Research Speak - 16-04-2010Document12 pagesResearch Speak - 16-04-2010A_KinshukNo ratings yet

- Florida's August Employment Figures Released: Charlie Crist Cynthia R. LorenzoDocument16 pagesFlorida's August Employment Figures Released: Charlie Crist Cynthia R. LorenzoMichael AllenNo ratings yet

- Derivatives in IndiaDocument21 pagesDerivatives in IndiaShajupaulNo ratings yet

- Florida's October Employment Figures Released: TallahasseeDocument16 pagesFlorida's October Employment Figures Released: TallahasseeMichael AllenNo ratings yet

- The Week That Just Passed March 12, 2010Document4 pagesThe Week That Just Passed March 12, 2010WallstreetableNo ratings yet

- Livestock Price Volatility: Eric BelascoDocument15 pagesLivestock Price Volatility: Eric BelascoGlen YNo ratings yet

- 23) Sacramento, CA: Figure 157: Year/Year Change in Existing Home Prices - Sacramento, CADocument11 pages23) Sacramento, CA: Figure 157: Year/Year Change in Existing Home Prices - Sacramento, CAsacrealstatsNo ratings yet

- Presentation To Macquarie Corporate Day in Singapore & Hong KongDocument54 pagesPresentation To Macquarie Corporate Day in Singapore & Hong KongnigelburkeNo ratings yet

- Florida's June Employment Figures Released: Governor DirectorDocument16 pagesFlorida's June Employment Figures Released: Governor DirectorMichael AllenNo ratings yet

- EPCA Seminar: Olefins Outlook: 9 October 2020Document13 pagesEPCA Seminar: Olefins Outlook: 9 October 2020Aswin KondapallyNo ratings yet

- CME - Comparing E-Minis and ETFs - Sep2012 PDFDocument8 pagesCME - Comparing E-Minis and ETFs - Sep2012 PDFbearsqNo ratings yet

- MHIFU HandoutDocument2 pagesMHIFU HandoutThunder PigNo ratings yet

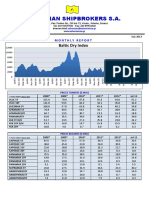

- Athenian-Shipbrokers-July 2013Document18 pagesAthenian-Shipbrokers-July 2013Nguyen Le Thu HaNo ratings yet

- Monetary Review of The Republic of Tajikistan: For January-July 2006Document2 pagesMonetary Review of The Republic of Tajikistan: For January-July 2006ctjsuwll ctjsuwllNo ratings yet

- Oracle Database 11g OverviewDocument46 pagesOracle Database 11g OverviewEddie Awad91% (11)

- Apollo Credit Market Outlook Jul23Document157 pagesApollo Credit Market Outlook Jul23supNo ratings yet

- AS-AD Applications and Data InterpretationDocument2 pagesAS-AD Applications and Data Interpretationalanoud AlmheiriNo ratings yet

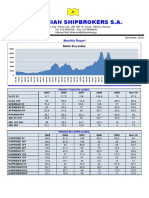

- athenian-shipbrokers-NOV 2010Document17 pagesathenian-shipbrokers-NOV 2010Nguyen Le Thu HaNo ratings yet

- Shipping Companies' Financial Performance Measurement Using Industry Key Performance Indicators Case Study: The Highly Volatile Period 2007 - 2010Document22 pagesShipping Companies' Financial Performance Measurement Using Industry Key Performance Indicators Case Study: The Highly Volatile Period 2007 - 2010Luis Enrique LavayenNo ratings yet

- Special Section 1Document3 pagesSpecial Section 1M.A. ShaikhNo ratings yet

- in Our View,: Vrddhi Capital Investment AdvisorsDocument5 pagesin Our View,: Vrddhi Capital Investment AdvisorsMohit AgarwalNo ratings yet

- Goldman Asia Conviction Call Catch-Up 13sep10Document11 pagesGoldman Asia Conviction Call Catch-Up 13sep10tanmartinNo ratings yet

- Governors Third Quarter Media Brief 2008Document16 pagesGovernors Third Quarter Media Brief 2008Chola MukangaNo ratings yet

- Electric Utility Industry 101: WebinarDocument32 pagesElectric Utility Industry 101: WebinarTechnical karanNo ratings yet

- Unemployment DataDocument2 pagesUnemployment Datakettle1No ratings yet

- Job Losses Since December 2007Document1 pageJob Losses Since December 2007EricFruitsNo ratings yet

- Lanvyl TubesDocument5 pagesLanvyl TubesIshmeet SinghNo ratings yet

- Lecture 2 Case Study McDonald's Dim Sum Bonds "Lovin' It"Document4 pagesLecture 2 Case Study McDonald's Dim Sum Bonds "Lovin' It"Simal ShaikhNo ratings yet

- Assumption and Data Sources:: Kettle1 ResearchDocument5 pagesAssumption and Data Sources:: Kettle1 Researchkettle1No ratings yet

- Gmo - For Whom The Bond TollsDocument8 pagesGmo - For Whom The Bond Tollsfreemind3682No ratings yet

- Southeast Texas Labor StatisticsDocument1 pageSoutheast Texas Labor StatisticsCharlie FoxworthNo ratings yet

- Chinese Airlines - The "Early Bird" For Recovery: China Air Passenger Traffic China Air Freight TrafficDocument1 pageChinese Airlines - The "Early Bird" For Recovery: China Air Passenger Traffic China Air Freight TrafficdaheicuyingNo ratings yet

- September 2010Document1 pageSeptember 2010Stephanie Miller HofmanNo ratings yet

- South Korean Energy Outlook 2015Document13 pagesSouth Korean Energy Outlook 2015Afifa KamilaNo ratings yet

- Outlook For The SMSF SectorDocument13 pagesOutlook For The SMSF SectorRomeoNo ratings yet

- Mar 09 Fact Sheet Class ADocument1 pageMar 09 Fact Sheet Class ADominique PajaresNo ratings yet

- Hondacivic ArDocument2 pagesHondacivic Arapi-3709675No ratings yet

- MEF Analysis UI Claims - March 2020Document2 pagesMEF Analysis UI Claims - March 2020Dave AllenNo ratings yet

- Retail q1 2011Document6 pagesRetail q1 2011avisitoronscribdNo ratings yet

- 2007 GPS Pricing Trends ReportDocument3 pages2007 GPS Pricing Trends Reportlili_pumaNo ratings yet

- Canara Robeco Emerging Equities: February 2018Document25 pagesCanara Robeco Emerging Equities: February 2018gowtham1993eeeNo ratings yet

- Mwo 121010Document10 pagesMwo 121010richardck50No ratings yet

- Profile The Leela Palaces Hotels and ResortsDocument2 pagesProfile The Leela Palaces Hotels and Resortshafshu100% (1)

- Moulinex Catalogue 2016 EnglishDocument25 pagesMoulinex Catalogue 2016 EnglishNoCWNo ratings yet

- IntroductionDocument18 pagesIntroductionteddykeyNo ratings yet

- Cadbury ReportDocument7 pagesCadbury ReportSumeet GuptaNo ratings yet

- Corality ModelOff Sample Answer Hard TimesDocument81 pagesCorality ModelOff Sample Answer Hard TimesserpepeNo ratings yet

- IRS LetterDocument6 pagesIRS LetterHarold HugginsNo ratings yet

- Implementing Strategies: Marketing, Finance/Accounting, R&D, and MIS IssuesDocument39 pagesImplementing Strategies: Marketing, Finance/Accounting, R&D, and MIS IssuesHarvey PeraltaNo ratings yet

- An Investigation of The Determinants of Bank Failure and Distress of Commercial and Merchant Banks in Zimbabwe (2011-2015)Document3 pagesAn Investigation of The Determinants of Bank Failure and Distress of Commercial and Merchant Banks in Zimbabwe (2011-2015)Wayne MhlangaNo ratings yet

- Domar 1946Document12 pagesDomar 1946Stephany SandovalNo ratings yet

- A K Srivastava - Essar PowerDocument13 pagesA K Srivastava - Essar PowerVishal SinghNo ratings yet

- 3rd Floor AgreementDocument15 pages3rd Floor AgreementjyotichatterjeeNo ratings yet

- Development in Wagon FinalDocument133 pagesDevelopment in Wagon Finalkr_abhijeet72356587100% (5)

- Powerpoint Lectures For Principles of Economics, 9E by Karl E. Case, Ray C. Fair & Sharon M. OsterDocument26 pagesPowerpoint Lectures For Principles of Economics, 9E by Karl E. Case, Ray C. Fair & Sharon M. OsterHala TarekNo ratings yet

- Swot Analysis - DHA 1Document15 pagesSwot Analysis - DHA 1Laxmi PriyaNo ratings yet

- International Marketing Chapter 1Document32 pagesInternational Marketing Chapter 1Amir Ali100% (4)

- This Study Resource Was Shared Via: My CoursesDocument6 pagesThis Study Resource Was Shared Via: My CoursesJOHNSON KORAINo ratings yet

- Career Focus WorksheetDocument2 pagesCareer Focus Worksheetapi-369601432No ratings yet

- Africa Renewable Energy Market Poised For A Strong Stride - An Aranca InfographicDocument1 pageAfrica Renewable Energy Market Poised For A Strong Stride - An Aranca Infographicaranca_ipNo ratings yet

- Role of Government in Developing EntrepreneursDocument8 pagesRole of Government in Developing EntrepreneursanishtomanishNo ratings yet

- Kristen's Cookies Co - Mind MapDocument1 pageKristen's Cookies Co - Mind MapAnthony KwoNo ratings yet

- Memorandum of Agreement (MOA) : BetweenDocument2 pagesMemorandum of Agreement (MOA) : BetweenGracee MedinaNo ratings yet

- 26 John DeereDocument215 pages26 John Deerecorsaroleoneminitaur100% (1)

- ToA.1830 - Accounting Changes and Errors - OnlineDocument3 pagesToA.1830 - Accounting Changes and Errors - OnlineJolina ManceraNo ratings yet

- Chicago Garbage Fee CommunicationsDocument10 pagesChicago Garbage Fee CommunicationsDNAinfo ChicagoNo ratings yet

- E F Eng l1 l2 Si 075Document1 pageE F Eng l1 l2 Si 075Simona Bute0% (1)

- Bajaj Finance JP MorganDocument38 pagesBajaj Finance JP MorganNikhilKapoor29No ratings yet

- Weber 31701Document2 pagesWeber 31701Rowan Nuguid ElominaNo ratings yet

- MCO-4 Dec12Document6 pagesMCO-4 Dec12BinayKPNo ratings yet

- Starbucks CaseDocument3 pagesStarbucks CaseKiranNo ratings yet

- CIR vs. CityTrustDocument2 pagesCIR vs. CityTrustRea Jane B. MalcampoNo ratings yet

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 4.5 out of 5 stars4.5/5 (14)

- John D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthFrom EverandJohn D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthRating: 4 out of 5 stars4/5 (20)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisFrom EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisRating: 5 out of 5 stars5/5 (6)

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNFrom Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNRating: 4.5 out of 5 stars4.5/5 (3)

- Ready, Set, Growth hack:: A beginners guide to growth hacking successFrom EverandReady, Set, Growth hack:: A beginners guide to growth hacking successRating: 4.5 out of 5 stars4.5/5 (93)

- These Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 3.5 out of 5 stars3.5/5 (8)

- The 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamFrom EverandThe 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamNo ratings yet

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingFrom EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingRating: 4.5 out of 5 stars4.5/5 (17)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialRating: 4.5 out of 5 stars4.5/5 (32)

- Value: The Four Cornerstones of Corporate FinanceFrom EverandValue: The Four Cornerstones of Corporate FinanceRating: 4.5 out of 5 stars4.5/5 (18)

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursFrom EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursRating: 4.5 out of 5 stars4.5/5 (8)

- Creating Shareholder Value: A Guide For Managers And InvestorsFrom EverandCreating Shareholder Value: A Guide For Managers And InvestorsRating: 4.5 out of 5 stars4.5/5 (8)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- The Merger & Acquisition Leader's Playbook: A Practical Guide to Integrating Organizations, Executing Strategy, and Driving New Growth after M&A or Private Equity DealsFrom EverandThe Merger & Acquisition Leader's Playbook: A Practical Guide to Integrating Organizations, Executing Strategy, and Driving New Growth after M&A or Private Equity DealsNo ratings yet

- Built, Not Born: A Self-Made Billionaire's No-Nonsense Guide for EntrepreneursFrom EverandBuilt, Not Born: A Self-Made Billionaire's No-Nonsense Guide for EntrepreneursRating: 5 out of 5 stars5/5 (13)

- Private Equity and Venture Capital in Europe: Markets, Techniques, and DealsFrom EverandPrivate Equity and Venture Capital in Europe: Markets, Techniques, and DealsRating: 5 out of 5 stars5/5 (1)

- Mind over Money: The Psychology of Money and How to Use It BetterFrom EverandMind over Money: The Psychology of Money and How to Use It BetterRating: 4 out of 5 stars4/5 (24)

- Warren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorFrom EverandWarren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorNo ratings yet

- Financial Risk Management: A Simple IntroductionFrom EverandFinancial Risk Management: A Simple IntroductionRating: 4.5 out of 5 stars4.5/5 (7)

- Product-Led Growth: How to Build a Product That Sells ItselfFrom EverandProduct-Led Growth: How to Build a Product That Sells ItselfRating: 5 out of 5 stars5/5 (1)

- Valley Girls: Lessons From Female Founders in the Silicon Valley and BeyondFrom EverandValley Girls: Lessons From Female Founders in the Silicon Valley and BeyondNo ratings yet

- The Value of a Whale: On the Illusions of Green CapitalismFrom EverandThe Value of a Whale: On the Illusions of Green CapitalismRating: 5 out of 5 stars5/5 (2)

- Finance Secrets of Billion-Dollar Entrepreneurs: Venture Finance Without Venture Capital (Capital Productivity, Business Start Up, Entrepreneurship, Financial Accounting)From EverandFinance Secrets of Billion-Dollar Entrepreneurs: Venture Finance Without Venture Capital (Capital Productivity, Business Start Up, Entrepreneurship, Financial Accounting)Rating: 4 out of 5 stars4/5 (5)