You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- BiologyDocument3 pagesBiologyquratulainNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Physics: 1. Physical Quantities and MeasurementDocument2 pagesPhysics: 1. Physical Quantities and MeasurementKashifntcNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Dawn Word List.Document29 pagesDawn Word List.Rai AhsanNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- ChemistryDocument3 pagesChemistryYasir WazirNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Essay Live Like Flower FrangranceDocument2 pagesEssay Live Like Flower FrangranceKashifntcNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Spread of Coronavirus (Covid-19) .Document1 pageThe Spread of Coronavirus (Covid-19) .KashifntcNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Essay Live Like Flower FrangranceDocument2 pagesEssay Live Like Flower FrangranceKashifntcNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- 5th ScienceWorksheetDocument2 pages5th ScienceWorksheetKashifntcNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Grade 6th EnglishDocument3 pagesGrade 6th EnglishKashifntcNo ratings yet

- Homework CLASS 1Document2 pagesHomework CLASS 1KashifntcNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Class 1Document3 pagesClass 1KashifntcNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Gwadar To Quetta Route With KilometerDocument1 pageGwadar To Quetta Route With KilometerKashifntcNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Memorize Class 1 PDFDocument1 pageMemorize Class 1 PDFKashifntcNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- 6th Computer .Week#8 DoneDocument3 pages6th Computer .Week#8 DoneKashifntcNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Grade 1Document2 pagesGrade 1KashifntcNo ratings yet

- 5th ScienceWorksheetDocument2 pages5th ScienceWorksheetKashifntcNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- 6th Computer - WEEK#7 Done (Solved)Document3 pages6th Computer - WEEK#7 Done (Solved)KashifntcNo ratings yet

- 6th Computer Worksheet .WEEK1Document3 pages6th Computer Worksheet .WEEK1KashifntcNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- 6th Computer Worksheet .WEEK1Document3 pages6th Computer Worksheet .WEEK1KashifntcNo ratings yet

- Public Procurement Rules 2004Document17 pagesPublic Procurement Rules 2004Muhammad Ali QureshiNo ratings yet

- Classification of Things Chapter 6Document4 pagesClassification of Things Chapter 6KashifntcNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- 6th COMPUTER WRKSHEET - WEEK4Document5 pages6th COMPUTER WRKSHEET - WEEK4KashifntcNo ratings yet

- Chem 10th Class (3nd WK) Work SheetDocument2 pagesChem 10th Class (3nd WK) Work SheetKashifntcNo ratings yet

- Entrepreneurship Project On Fast Food RestaurantDocument23 pagesEntrepreneurship Project On Fast Food RestaurantKashifntc100% (1)

- Entrepreneurship Project On Fast Food RestaurantDocument23 pagesEntrepreneurship Project On Fast Food RestaurantKashifntc100% (1)

- SignificanceDocument13 pagesSignificanceKashifntcNo ratings yet

- Research DesignDocument10 pagesResearch DesignBalaji N92% (13)

- Entrepreneurship Plastic Recycling ProjectDocument19 pagesEntrepreneurship Plastic Recycling ProjectKashifntcNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Islamic Vs Modern BONDDocument18 pagesIslamic Vs Modern BONDPakassignmentNo ratings yet

- Rosc Aa EthiopiaDocument24 pagesRosc Aa EthiopiaKenn Mwangii100% (2)

- Guide To P2P Lending - InfographicDocument1 pageGuide To P2P Lending - InfographicPrime Meridian Capital ManagementNo ratings yet

- Pay Slip FormatDocument10 pagesPay Slip FormatKarthik Kumar PNo ratings yet

- George Soros, S SecretsDocument21 pagesGeorge Soros, S Secretscorneliusflavius7132No ratings yet

- Greg - Speicher Ways To Improve Your Investment Process PDFDocument37 pagesGreg - Speicher Ways To Improve Your Investment Process PDFRajeev BahugunaNo ratings yet

- ATRAM Global Technology Feeder Fund Fact Sheet Jan 2020Document2 pagesATRAM Global Technology Feeder Fund Fact Sheet Jan 2020anton clementeNo ratings yet

- Case 2 AuditDocument8 pagesCase 2 AuditReinhard BosNo ratings yet

- Finacc 3 Question Set BDocument9 pagesFinacc 3 Question Set BEza Joy ClaveriasNo ratings yet

- The Banker & Customer Relationship in IndiaDocument85 pagesThe Banker & Customer Relationship in IndiaNeed Notknow50% (2)

- ACCM343 Advanced Accounting 2011 by Guerrero PeraltaDocument218 pagesACCM343 Advanced Accounting 2011 by Guerrero PeraltaHujaype Abubakar80% (10)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- VP Institutional Asset Management in Washington DC Resume Lisa DrazinDocument3 pagesVP Institutional Asset Management in Washington DC Resume Lisa DrazinLisaDrazinNo ratings yet

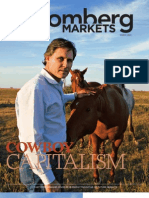

- Salem Abraham - Bloomberg Markets Mag Article - Mar09Document8 pagesSalem Abraham - Bloomberg Markets Mag Article - Mar09jk_rentzkeNo ratings yet

- LAWS3113 Lecture 2 - Maxims of EquityDocument7 pagesLAWS3113 Lecture 2 - Maxims of EquityThoughts of a Law StudentNo ratings yet

- Assetvilla Insurance Marketing LLP: A Summer Internship Project (SIP) Done inDocument45 pagesAssetvilla Insurance Marketing LLP: A Summer Internship Project (SIP) Done indevak shelarNo ratings yet

- Certified Accounting Technician Examination Advanced Level Paper T9 (SGP)Document14 pagesCertified Accounting Technician Examination Advanced Level Paper T9 (SGP)springnet2011No ratings yet

- Solutions To End-Of-Chapter ProblemsDocument22 pagesSolutions To End-Of-Chapter ProblemsKalyani GogoiNo ratings yet

- Opinin Denying Motion To DismissDocument29 pagesOpinin Denying Motion To DismissForeclosure FraudNo ratings yet

- Reasons Why Businesses FailDocument10 pagesReasons Why Businesses FailJay PatelNo ratings yet

- How To Buy and Sell StockDocument9 pagesHow To Buy and Sell StockwaelNo ratings yet

- Financial Ratio Analysis Aldar UpdatedDocument36 pagesFinancial Ratio Analysis Aldar UpdatedHasanNo ratings yet

- Management Accounting - HCA16ge - Ch21Document63 pagesManagement Accounting - HCA16ge - Ch21Corliss Ko100% (1)

- 8th Grade Intensive - Topic 1Document96 pages8th Grade Intensive - Topic 1Ravvi GanesanNo ratings yet

- Maxims of EquityDocument10 pagesMaxims of EquityAzra Athirah Abdul JalilNo ratings yet

- Institutional Support For New VenturesDocument8 pagesInstitutional Support For New VenturesAdeem AshrafiNo ratings yet

- Presentation On Liabilities Under Securities Law 28.11.2011Document51 pagesPresentation On Liabilities Under Securities Law 28.11.2011Vidya AdsuleNo ratings yet

- BRC (Company Law - Group 6)Document13 pagesBRC (Company Law - Group 6)UditaNo ratings yet

- Atkins 2014Document188 pagesAtkins 2014rajeshNo ratings yet

- Understanding The Theory: Phase 1: Growth Through CreativityDocument3 pagesUnderstanding The Theory: Phase 1: Growth Through CreativitySri NivasanNo ratings yet

- FINDocument16 pagesFINAnbang Xiao50% (2)

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!From EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Rating: 4.5 out of 5 stars4.5/5 (14)

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindFrom EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindRating: 5 out of 5 stars5/5 (231)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)From EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Rating: 4.5 out of 5 stars4.5/5 (13)

- A Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineFrom EverandA Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineNo ratings yet

- Getting to Yes: How to Negotiate Agreement Without Giving InFrom EverandGetting to Yes: How to Negotiate Agreement Without Giving InRating: 4 out of 5 stars4/5 (652)

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet