You might also like

- ACCUFOX-ENTERPRISES - PC Jewellers Franchise - 1 StoreDocument5 pagesACCUFOX-ENTERPRISES - PC Jewellers Franchise - 1 StoreJai PhookanNo ratings yet

- BWR A- & BWR A2+ Ratings Assigned to Megha Engineering & Infrastructures LtdDocument3 pagesBWR A- & BWR A2+ Ratings Assigned to Megha Engineering & Infrastructures Ltdvivekpatel1234No ratings yet

- Ajanta Soya 13may2021Document7 pagesAjanta Soya 13may2021praveen kumarNo ratings yet

- Brickwork assigns BWR BB- rating to Asquare Food & BeveragesDocument6 pagesBrickwork assigns BWR BB- rating to Asquare Food & BeveragesTanmay GuptaNo ratings yet

- Microlite Indsutries 30may2020Document3 pagesMicrolite Indsutries 30may2020utkarsh kumarNo ratings yet

- Hindustan - Associates - 4 Tanishq Stores in UPDocument5 pagesHindustan - Associates - 4 Tanishq Stores in UPJai PhookanNo ratings yet

- Yashodhara Super Speciality Hospital Private LimitedDocument6 pagesYashodhara Super Speciality Hospital Private LimitedAvinash ShelkeNo ratings yet

- Faridabad Steel Mongers Rating RationaleDocument4 pagesFaridabad Steel Mongers Rating RationaleShamNo ratings yet

- Avenue Supermarts LimitedDocument6 pagesAvenue Supermarts LimitedAvinash GollaNo ratings yet

- DR Datson Labs 22mar2021Document5 pagesDR Datson Labs 22mar2021office88kolNo ratings yet

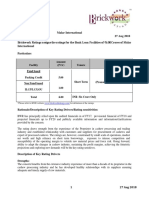

- BWR A4 Rating for Malar International's Rs.6 Cr Bank Loan FacilitiesDocument4 pagesBWR A4 Rating for Malar International's Rs.6 Cr Bank Loan FacilitiesNalla ThambiNo ratings yet

- S. Jogani Exports Private LimitedDocument6 pagesS. Jogani Exports Private Limitedarc14consultantNo ratings yet

- JSSI Hydraulics Credit RatingDocument2 pagesJSSI Hydraulics Credit RatingVibhu SinghNo ratings yet

- Incred Financial Services Limited Press+ReleaseDocument7 pagesIncred Financial Services Limited Press+ReleaseGautam MehtaNo ratings yet

- A One Steel Alloys 10may2021Document7 pagesA One Steel Alloys 10may2021L KNo ratings yet

- Sri Kauvery Medical Care 11 01 24Document10 pagesSri Kauvery Medical Care 11 01 24mskumar01992No ratings yet

- Welspun-Specialty-Solutions-4Nov2019 BrickworkDocument7 pagesWelspun-Specialty-Solutions-4Nov2019 BrickworkPuneet367No ratings yet

- RBL BANK's Valuation - Perception or Reality Check?: TH TH TH TH THDocument2 pagesRBL BANK's Valuation - Perception or Reality Check?: TH TH TH TH THHARSHIT AHUJA PGP 2021-23 BatchNo ratings yet

- Sri - Shyam - Jewellers - Tanishq Franchise 1 StoreDocument4 pagesSri - Shyam - Jewellers - Tanishq Franchise 1 StoreJai PhookanNo ratings yet

- Sri Someshwara - R-27022017 PDFDocument6 pagesSri Someshwara - R-27022017 PDFAjith KumarNo ratings yet

- Anoop Oswal Hosiery Final NoteDocument35 pagesAnoop Oswal Hosiery Final Notetejasj171484No ratings yet

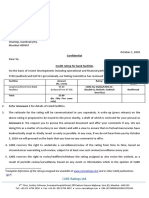

- Credit Rating LetterDocument10 pagesCredit Rating LetterMAHI LADNo ratings yet

- RATING RATIONALE FOR DEREWALA INDUSTRIES LTDDocument6 pagesRATING RATIONALE FOR DEREWALA INDUSTRIES LTDMukul SoniNo ratings yet

- Y-Wildcraft-India-18Oct 2022Document8 pagesY-Wildcraft-India-18Oct 2022PratyushNo ratings yet

- Pondy Oxides and Chemicals 22apr2019Document6 pagesPondy Oxides and Chemicals 22apr2019DarshanNo ratings yet

- RBI Policy - Key Challenges For The Banking SectorDocument4 pagesRBI Policy - Key Challenges For The Banking SectorRekha LohiaNo ratings yet

- CRD Foods 8apr2020Document6 pagesCRD Foods 8apr2020samudragupta05No ratings yet

- Investigation On The Flow Behaviour of ADocument6 pagesInvestigation On The Flow Behaviour of ANikhil GuptaNo ratings yet

- SRC Chemicals Private LimitedDocument8 pagesSRC Chemicals Private Limitedgcgary87No ratings yet

- Poddar Diamonds Limited-09-29-2017Document4 pagesPoddar Diamonds Limited-09-29-2017tridev kant tripathiNo ratings yet

- Y-Wildcraft-India-18Oct 2022Document8 pagesY-Wildcraft-India-18Oct 2022PratyushNo ratings yet

- Maha Durga Charitable Trust: Summary of Rated Instruments Instrument Rated Amount (Rs. Crore) Rating ActionDocument6 pagesMaha Durga Charitable Trust: Summary of Rated Instruments Instrument Rated Amount (Rs. Crore) Rating ActionNeeraj_Kumar_AgrawalNo ratings yet

- Kutch Chemical Industries BankLoan 222Cr Revision Rationale 9may2016Document2 pagesKutch Chemical Industries BankLoan 222Cr Revision Rationale 9may2016JatinBansalNo ratings yet

- The Bombay Dyeing & Manufacturing Company LimitedDocument5 pagesThe Bombay Dyeing & Manufacturing Company LimitedvaishnaviNo ratings yet

- Best Finance Corporation Limited: Facilities/Instruments Amount (Rs. Crore) Rating Rating ActionDocument5 pagesBest Finance Corporation Limited: Facilities/Instruments Amount (Rs. Crore) Rating Rating ActionKarthikeyan RK SwamyNo ratings yet

- Shiv Health Foods Llp-RU-12-06-2023Document12 pagesShiv Health Foods Llp-RU-12-06-2023Rituraj solankiNo ratings yet

- SBI Will Slash RatesDocument2 pagesSBI Will Slash RatesChetan PanchamiaNo ratings yet

- Hinduja Healthcare 29dec2020Document8 pagesHinduja Healthcare 29dec2020Bijay MehtaNo ratings yet

- Samunnati Rating Rationale b764561b41Document8 pagesSamunnati Rating Rationale b764561b41PratyushNo ratings yet

- Ujjivan Small Finance Bank LimitedDocument5 pagesUjjivan Small Finance Bank LimitedSaurav KumarNo ratings yet

- Maruti Suzuki Kizashi Marketing PlanDocument8 pagesMaruti Suzuki Kizashi Marketing Planniranjan bhagatNo ratings yet

- PresentationSUMMARY (A)Document2 pagesPresentationSUMMARY (A)Rakib HasanNo ratings yet

- RBL Bank AR - 2020Document156 pagesRBL Bank AR - 2020anil1820No ratings yet

- BWR assigns BBB rating to Manikaran PowerDocument2 pagesBWR assigns BBB rating to Manikaran PowerCA Rakesh JhaNo ratings yet

- Corporate-Finance-AM-STDocument5 pagesCorporate-Finance-AM-STAash RedmiNo ratings yet

- Bhuwalka and Sons Private LimitedDocument4 pagesBhuwalka and Sons Private LimiteddoctorsabeehNo ratings yet

- Procedure of Credit RatingDocument57 pagesProcedure of Credit RatingMilon SultanNo ratings yet

- Milkfood Ltd. Bank Loan Rating Downgraded to BBB- on Revenue DeclineDocument7 pagesMilkfood Ltd. Bank Loan Rating Downgraded to BBB- on Revenue DeclineUthay UthayNo ratings yet

- Motisons IPONoteDocument4 pagesMotisons IPONotefirozalam841227No ratings yet

- Wockhardt LimitedDocument8 pagesWockhardt LimitedKumar SatyakamNo ratings yet

- Price Waterhouse & Co Chartered Accountants LLPDocument8 pagesPrice Waterhouse & Co Chartered Accountants LLPSuraj KumarNo ratings yet

- IPO - RBZ Jewellers 1Document3 pagesIPO - RBZ Jewellers 1Ravi DiyoraNo ratings yet

- Microfinance Private LimitedDocument5 pagesMicrofinance Private LimitedsantoshbsantuNo ratings yet

- Chromachemie Laboratory Private LimitedDocument7 pagesChromachemie Laboratory Private Limitedkrushna.maneNo ratings yet

- Shilchar_Technologies_LimitedDocument5 pagesShilchar_Technologies_Limitedjaikumar608jainNo ratings yet

- EarningUpdatesPresentation BBL 30092021 PDFDocument29 pagesEarningUpdatesPresentation BBL 30092021 PDFsuman sheikhNo ratings yet

- Bikaji Foods International LimitedDocument7 pagesBikaji Foods International Limitedadhyan kashyapNo ratings yet

- PacraDocument6 pagesPacraJunaid KhalidNo ratings yet

- Professional Profile Saurav Sethia 21-22Document2 pagesProfessional Profile Saurav Sethia 21-22utkarsh singhNo ratings yet

- Rolls-Royce Motorcars Range Product Overview Brochure - RoW PDFDocument76 pagesRolls-Royce Motorcars Range Product Overview Brochure - RoW PDFDEVESH BHOLENo ratings yet

- Data Monitor Report - Soft DrinksDocument26 pagesData Monitor Report - Soft DrinksKhushi SawlaniNo ratings yet

- Adani AR 2019-20Document220 pagesAdani AR 2019-20DEVESH BHOLENo ratings yet

- A Short History of Corruption, Destruction and Criminal ActivityDocument16 pagesA Short History of Corruption, Destruction and Criminal ActivityDEVESH BHOLENo ratings yet

- Ijsrp p5658 PDFDocument6 pagesIjsrp p5658 PDFDEVESH BHOLENo ratings yet

- Bata India Annual 2013Document140 pagesBata India Annual 2013Aditya ChauhanNo ratings yet

- SMB University 120307 Networking Fundamentals PDFDocument38 pagesSMB University 120307 Networking Fundamentals PDFJacques Giard100% (1)

- 1009 4980Document5 pages1009 4980DEVESH BHOLENo ratings yet

- Mobile Phone Bangla KeypadDocument6 pagesMobile Phone Bangla KeypadDEVESH BHOLENo ratings yet

- Coal Industry PDFDocument10 pagesCoal Industry PDFVineet SharmaNo ratings yet

- Simplex MethodDocument16 pagesSimplex MethodShantanu Dutta100% (1)

- Perception of Brand Positioning of Aje Big Cola: Chaleeporn LeampriboonDocument2 pagesPerception of Brand Positioning of Aje Big Cola: Chaleeporn LeampriboonDEVESH BHOLENo ratings yet

- Nse PDFDocument104 pagesNse PDFVicky VaioNo ratings yet

- Ambit BataIndia Initiation DistributionhaslittlePowerleft 09dec2015Document36 pagesAmbit BataIndia Initiation DistributionhaslittlePowerleft 09dec2015DEVESH BHOLENo ratings yet

- Ijsrp p5658 PDFDocument6 pagesIjsrp p5658 PDFDEVESH BHOLENo ratings yet

- Coke PPAHDocument5 pagesCoke PPAHOscar PettersNo ratings yet

- Research Report Fortis Healthcare LTDDocument13 pagesResearch Report Fortis Healthcare LTDDEVESH BHOLENo ratings yet

- Coke IPDocument99 pagesCoke IPAmit SarkarNo ratings yet

- Oracle 12c TOC PDFDocument18 pagesOracle 12c TOC PDFDEVESH BHOLE100% (1)

- En16 Ar SecDocument244 pagesEn16 Ar SecDEVESH BHOLENo ratings yet

- 636122917776478561 (1)Document52 pages636122917776478561 (1)DEVESH BHOLENo ratings yet

- Win a Trip to Adopt a Giraffe with BIG ColaDocument2 pagesWin a Trip to Adopt a Giraffe with BIG ColaDEVESH BHOLENo ratings yet

- 20th Annual Report 2015 16 - Opt PDFDocument300 pages20th Annual Report 2015 16 - Opt PDFDEVESH BHOLENo ratings yet

- Advertisement Financial Results 310314Document1 pageAdvertisement Financial Results 310314DEVESH BHOLENo ratings yet

- Colorbond Steel Colours For Your Home Colour Chart PDFDocument4 pagesColorbond Steel Colours For Your Home Colour Chart PDFDEVESH BHOLENo ratings yet

- 4 ColoursDocument4 pages4 ColoursDEVESH BHOLENo ratings yet

- TX Star Plus HandbookDocument86 pagesTX Star Plus HandbookDEVESH BHOLENo ratings yet

- Gly Star Plus H LabelDocument72 pagesGly Star Plus H LabelDEVESH BHOLENo ratings yet

- Manual Potenciometro ThermoDocument299 pagesManual Potenciometro ThermoDiegoMzaNo ratings yet

- Superior Healthplan (Superior) Star+Plus Medicare-Medicaid Plan (MMP) 2017 Provider & Pharmacy Directory InformationDocument11 pagesSuperior Healthplan (Superior) Star+Plus Medicare-Medicaid Plan (MMP) 2017 Provider & Pharmacy Directory InformationDEVESH BHOLENo ratings yet

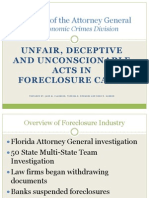

- Florida Attorney General Fraudclosure Report - Unfair, Deceptive and Unconscionable Acts in Foreclosure CasesDocument98 pagesFlorida Attorney General Fraudclosure Report - Unfair, Deceptive and Unconscionable Acts in Foreclosure CasesForeclosure Fraud100% (12)

- Comparison of Unit Link Products Performance in IndonesiaDocument17 pagesComparison of Unit Link Products Performance in IndonesiaFitria HasanahNo ratings yet

- TBChap 007Document101 pagesTBChap 007wannaflynowNo ratings yet

- RREEF Investment Outlook 8-10Document15 pagesRREEF Investment Outlook 8-10dealjunkieblog9676No ratings yet

- Banking TheoryDocument299 pagesBanking TheoryMohammedNo ratings yet

- Portfolio RiskDocument24 pagesPortfolio RiskABC DEFNo ratings yet

- Brian Windsor CalculationDocument12 pagesBrian Windsor CalculationprakashNo ratings yet

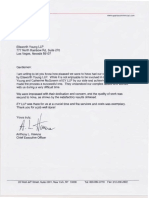

- Exhibits For First LetterDocument34 pagesExhibits For First Letterapi-359234129No ratings yet

- Butterfly Spread Profit Table for Seminar 9 – Problem 3Document11 pagesButterfly Spread Profit Table for Seminar 9 – Problem 3Raghuveer ChandraNo ratings yet

- Silkair Singapore Vs CirDocument15 pagesSilkair Singapore Vs Circode4saleNo ratings yet

- Leverage and Pip ValueDocument4 pagesLeverage and Pip ValueSanjayNo ratings yet

- 2018 CafmoDocument8 pages2018 CafmovilchizableNo ratings yet

- RBI Banking Awareness CapsuleDocument118 pagesRBI Banking Awareness CapsuleAbhishek Choudhary100% (1)

- LME trading calendar comparison 2018-2021Document2 pagesLME trading calendar comparison 2018-2021Rasmi RanjanNo ratings yet

- BSG PowerPoint Presentation - V1.5Document41 pagesBSG PowerPoint Presentation - V1.5Henry PamaNo ratings yet

- Partnership 2Document64 pagesPartnership 2Anis AlwaniNo ratings yet

- Raschke 0203 SFODocument4 pagesRaschke 0203 SFONandeshsinha75% (4)

- AIIBDocument142 pagesAIIBanon_761044641No ratings yet

- G.R. No. 205469 Bpi Family Savings Bank, Inc., Petitioner, St. Michael Medical Center, Inc., Respondent. Decision Perlas-Bernabe, J.Document61 pagesG.R. No. 205469 Bpi Family Savings Bank, Inc., Petitioner, St. Michael Medical Center, Inc., Respondent. Decision Perlas-Bernabe, J.Apling DincogNo ratings yet

- Manual Quick TrailingDocument2 pagesManual Quick TrailingDaniels JackNo ratings yet

- HybridDocument6 pagesHybridFernando SunNo ratings yet

- SFC Fund Manager Code of Conduct Workshop (Clifford Chance - Jan 2018)Document37 pagesSFC Fund Manager Code of Conduct Workshop (Clifford Chance - Jan 2018)Chris W ChanNo ratings yet

- Cardholder Dispute Form V3Document1 pageCardholder Dispute Form V3ShangHidalgoNo ratings yet

- Corporate Powers and Votes RequiredDocument2 pagesCorporate Powers and Votes Requiredrezeile morandarteNo ratings yet

- FINANCIAL PERFORMANCE ANALYSIS OF MACHCHAPUCHHRE BANK AND KUMARI BANK BASED ON CAMELDocument95 pagesFINANCIAL PERFORMANCE ANALYSIS OF MACHCHAPUCHHRE BANK AND KUMARI BANK BASED ON CAMELRajNo ratings yet

- Poly EnsaeDocument139 pagesPoly EnsaeSolo HakunaNo ratings yet

- Solution Manual For Financial Management 13th Edition by TitmanDocument3 pagesSolution Manual For Financial Management 13th Edition by Titmanazif kurnia100% (1)

- Notes On The Art of Short SellingDocument25 pagesNotes On The Art of Short Sellingbamzoo100% (1)

- 8 - An Economic Analysis On Financial StructureDocument18 pages8 - An Economic Analysis On Financial StructurecihtanbioNo ratings yet

- NavitasDocument16 pagesNavitaswikoliawensNo ratings yet