You might also like

- Hancock (2010-03) Momentum - A Contrarian Case For Following The HerdDocument13 pagesHancock (2010-03) Momentum - A Contrarian Case For Following The HerddrummondjacobNo ratings yet

- Is Economic Growth Good For InvestorsDocument13 pagesIs Economic Growth Good For InvestorsdpbasicNo ratings yet

- A2 AQB Crim Typo ProfilingDocument2 pagesA2 AQB Crim Typo Profilingscientist7No ratings yet

- Adam Button Secrets To TradingDocument13 pagesAdam Button Secrets To TradingelenabaciuNo ratings yet

- 2013 Picking NewslettersDocument24 pages2013 Picking NewslettersganeshtskNo ratings yet

- Forecasting Nike's Sales Using Facebook DataDocument10 pagesForecasting Nike's Sales Using Facebook Datascher1234No ratings yet

- Screener Setup - GersteinDocument86 pagesScreener Setup - Gersteinsreekesh unnikrishnanNo ratings yet

- Hedge Fund StrategiesDocument13 pagesHedge Fund StrategiesptselvakumarNo ratings yet

- Prudential M5 Mock PaperDocument22 pagesPrudential M5 Mock PaperAshNo ratings yet

- Rocking Wall Street: Four Powerful Strategies That will Shake Up the Way You Invest, Build Your Wealth And Give You Your Life BackFrom EverandRocking Wall Street: Four Powerful Strategies That will Shake Up the Way You Invest, Build Your Wealth And Give You Your Life BackRating: 1 out of 5 stars1/5 (1)

- In Your Best Interest: The Ultimate Guide to the Canadian Bond MarketFrom EverandIn Your Best Interest: The Ultimate Guide to the Canadian Bond MarketRating: 5 out of 5 stars5/5 (3)

- Student Research Project: Prepared byDocument31 pagesStudent Research Project: Prepared byPuneet SinghNo ratings yet

- Paul Tudor Jones InsightsDocument2 pagesPaul Tudor Jones InsightsJanNo ratings yet

- Adaptive Asset AllocationDocument14 pagesAdaptive Asset AllocationQuasiNo ratings yet

- Fading MomentumDocument31 pagesFading MomentumChristopher OlsonNo ratings yet

- Time Series MomentumDocument23 pagesTime Series MomentumpercysearchNo ratings yet

- Lifespan Investing: Building the Best Portfolio for Every Stage of Your LifeFrom EverandLifespan Investing: Building the Best Portfolio for Every Stage of Your LifeNo ratings yet

- Diversified Pitchbook 2015Document14 pagesDiversified Pitchbook 2015Tempest SpinNo ratings yet

- Technical ResearchDocument30 pagesTechnical Researchamit_idea1No ratings yet

- Linkage Analysis: Modus Operandi, Ritual, and Signature in Serial Sexual CrimeDocument12 pagesLinkage Analysis: Modus Operandi, Ritual, and Signature in Serial Sexual CrimeMuhamad FaizinNo ratings yet

- BYND ReversalDocument12 pagesBYND ReversalRavi RamanNo ratings yet

- The Disciplined Trader ScheduleDocument11 pagesThe Disciplined Trader Schedulemara saleNo ratings yet

- The Money Supply and Inflation PPT at Bec DomsDocument49 pagesThe Money Supply and Inflation PPT at Bec DomsBabasab Patil (Karrisatte)No ratings yet

- Timing Techniques for Commodity Futures Markets: Effective Strategy and Tactics for Short-Term and Long-Term TradersFrom EverandTiming Techniques for Commodity Futures Markets: Effective Strategy and Tactics for Short-Term and Long-Term TradersNo ratings yet

- Inflation Money Supply and Economic GrowthDocument13 pagesInflation Money Supply and Economic GrowthHassan Md RabiulNo ratings yet

- Finance Psychology: How To Begin Thinking Like A Professional Trader (This Workbook About Behavioral Finance Is All You Need To Be Successful In Trading)From EverandFinance Psychology: How To Begin Thinking Like A Professional Trader (This Workbook About Behavioral Finance Is All You Need To Be Successful In Trading)Rating: 5 out of 5 stars5/5 (3)

- The Australian Share Market - A History of DeclinesDocument12 pagesThe Australian Share Market - A History of DeclinesNick RadgeNo ratings yet

- Bandy NAAIM PaperDocument30 pagesBandy NAAIM Paperkanteron6443No ratings yet

- UntitledDocument138 pagesUntitledMiguel BenitesNo ratings yet

- Street Smart - User ManualDocument466 pagesStreet Smart - User Manualjose58No ratings yet

- Commodity Trader's Almanac 2012: For Active Traders of Futures, Forex, Stocks and ETFsFrom EverandCommodity Trader's Almanac 2012: For Active Traders of Futures, Forex, Stocks and ETFsNo ratings yet

- Forex FlashcardsDocument63 pagesForex Flashcardssting74100% (2)

- Trade Policy Update: A View From The Business CommunityDocument53 pagesTrade Policy Update: A View From The Business CommunityNational Press FoundationNo ratings yet

- Guppy Multiple Moving AverageDocument6 pagesGuppy Multiple Moving AverageBudi MulyonoNo ratings yet

- 6560 LectureDocument36 pages6560 Lectureapi-3699305100% (1)

- Kothari 2009Document33 pagesKothari 2009ya_nuNo ratings yet

- The Most Enlightening Technical Analysis Seminar, Advanced Market Timing Experts Workshop 2011Document8 pagesThe Most Enlightening Technical Analysis Seminar, Advanced Market Timing Experts Workshop 2011Golden NetworkingNo ratings yet

- IM - Executive RIM Whitepaper - Gens and Associates - V - Fall 2012 EditionDocument19 pagesIM - Executive RIM Whitepaper - Gens and Associates - V - Fall 2012 Editionpedrovsky702No ratings yet

- Comparative Analysis of Various Financial Institution in The Market 2011Document120 pagesComparative Analysis of Various Financial Institution in The Market 2011Binay TiwariNo ratings yet

- Mankiw's Macroeconomic Models Ch14Document15 pagesMankiw's Macroeconomic Models Ch14SamNo ratings yet

- Siegal CAPEDocument10 pagesSiegal CAPEJeffrey WilliamsNo ratings yet

- Which Shorts Are Informed?Document48 pagesWhich Shorts Are Informed?greg100% (1)

- 00.top 7 Books To Learn Technical AnalysisDocument5 pages00.top 7 Books To Learn Technical Analysisca812000No ratings yet

- GMI Global Panel BookDocument29 pagesGMI Global Panel BookEira SolidorNo ratings yet

- Portfolio Management Theory and Technical Analysis Lecture NotesDocument39 pagesPortfolio Management Theory and Technical Analysis Lecture NotesSam VakninNo ratings yet

- The 4macd SystemDocument5 pagesThe 4macd Systemfrog manNo ratings yet

- E-Mini Chart UpdateDocument3 pagesE-Mini Chart UpdateZerohedge100% (1)

- Ibd 20151218Document49 pagesIbd 20151218gnanda1987No ratings yet

- Subprime Mortgage CrisisDocument35 pagesSubprime Mortgage CrisisVineet GuptaNo ratings yet

- Get Your Free Covered Call CalculatorDocument5 pagesGet Your Free Covered Call CalculatorafaefNo ratings yet

- Market Technician No 45Document20 pagesMarket Technician No 45ppfahd100% (2)

- DOTS Guppy QuickStartDocument23 pagesDOTS Guppy QuickStartaldhosutra100% (1)

- Japanese Cloud Charts Ichimoku Kinko Hyo: Véronique Lashinski, CMT Newedge USA, LLCDocument52 pagesJapanese Cloud Charts Ichimoku Kinko Hyo: Véronique Lashinski, CMT Newedge USA, LLCpankaj thakurNo ratings yet

- Oil Shocks To Stock ReturnDocument46 pagesOil Shocks To Stock ReturnJose Mayer SinagaNo ratings yet

- Catalogue V 22Document20 pagesCatalogue V 22percysearchNo ratings yet

- Portfolio Allocation For The Active TraderDocument17 pagesPortfolio Allocation For The Active TraderXavier DaviasNo ratings yet

- Bulkowski's ForecastDocument9 pagesBulkowski's Forecastw_fibNo ratings yet

- Investor Demand For Sell-Side Research: Lawrence@haas - Berkeley.eduDocument57 pagesInvestor Demand For Sell-Side Research: Lawrence@haas - Berkeley.eduBhuwanNo ratings yet

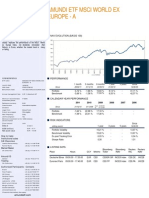

- Amundi Etf Msci World Ex Europe - A - Anglais - Eur - 3163!47!2!3!207 - MDocument2 pagesAmundi Etf Msci World Ex Europe - A - Anglais - Eur - 3163!47!2!3!207 - Mhp24714303No ratings yet

- Trey Glenn DisclosureDocument10 pagesTrey Glenn DisclosureJohn Archibald100% (1)

- Group 3 - Investment Services (Mutual Funds) Industry AnalysisDocument20 pagesGroup 3 - Investment Services (Mutual Funds) Industry AnalysisFERDYANTO TJHAINo ratings yet

- Braun - American Asset Manager CapitalismDocument35 pagesBraun - American Asset Manager Capitalismmannix carneyNo ratings yet

- Annexure I NISM-Series-V-A: Mutual Fund Distributors Certification Examination Objective of The ExaminationDocument2 pagesAnnexure I NISM-Series-V-A: Mutual Fund Distributors Certification Examination Objective of The ExaminationMutual Fund distributionNo ratings yet

- American Bar Association Members, OPERATING NORTHERN TRUSTDocument152 pagesAmerican Bar Association Members, OPERATING NORTHERN TRUSTDUTCH551400No ratings yet

- Investment Perception and Selection Behaviour Towards Mutual FundDocument11 pagesInvestment Perception and Selection Behaviour Towards Mutual FundmmmmmNo ratings yet

- EfficientlyInefficient ExercisesDocument34 pagesEfficientlyInefficient ExerciseswqivvfpwssxhccdznlNo ratings yet

- Merge (1) - Converted - by - AbcdpdfDocument105 pagesMerge (1) - Converted - by - AbcdpdfAnkita RanaNo ratings yet

- Certificate in Securities Ed16Document366 pagesCertificate in Securities Ed16Tim XUNo ratings yet

- Project Report On Mutual FundDocument98 pagesProject Report On Mutual FundPriya MalikNo ratings yet

- Real Estate Tokenization by AkashDocument29 pagesReal Estate Tokenization by AkashProject AtomNo ratings yet

- Alpha Capture Systems: Past, Present, and Future Directions: François-Serge LHABITANTDocument22 pagesAlpha Capture Systems: Past, Present, and Future Directions: François-Serge LHABITANTRobert HuetNo ratings yet

- CGC - 2.2.1 Study - 8FDLaelerDocument7 pagesCGC - 2.2.1 Study - 8FDLaelerCaleb Gonzalez CruzNo ratings yet

- Ishares World Equity Index Fund (Lu) Class n2 Eur Factsheet Lu0852473015 GB en IndividualDocument4 pagesIshares World Equity Index Fund (Lu) Class n2 Eur Factsheet Lu0852473015 GB en IndividualAbduRahman ZakariaNo ratings yet

- 10-Mutual FundsDocument69 pages10-Mutual FundsKartik BhartiaNo ratings yet

- Week 3 ModuleDocument14 pagesWeek 3 ModuleSofia Biangca M. BalderasNo ratings yet

- Investment Environment & Management ProcessDocument10 pagesInvestment Environment & Management ProcessMd Shahbub Alam SonyNo ratings yet

- CISDocument63 pagesCISSuRajUgaAdeNo ratings yet

- A Study On Investors Perception Towards Investment in Mutual FundsDocument56 pagesA Study On Investors Perception Towards Investment in Mutual FundsVishwas DeveeraNo ratings yet

- Artha PediaDocument158 pagesArtha Pediagajen_yadavNo ratings yet

- Project Report of Mutual Fund AnalysisDocument8 pagesProject Report of Mutual Fund AnalysisPrabhatNo ratings yet

- SCRADocument43 pagesSCRAkumar vedanshNo ratings yet

- BF2 - AnswerDocument34 pagesBF2 - AnswerCherielee FabroNo ratings yet

- FIN 4003 Week 7Document3 pagesFIN 4003 Week 7helaneymarshaNo ratings yet

- WARISANPLUS - 5 TahunDocument22 pagesWARISANPLUS - 5 TahunRaffy RazifNo ratings yet

- Consolidated Factsheet 11 2021 151221 191957 211226 154716Document60 pagesConsolidated Factsheet 11 2021 151221 191957 211226 154716ABHISHEK GUPTANo ratings yet

- Bilaspur 28042017Document25 pagesBilaspur 28042017mahanth gowdaNo ratings yet