You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- HINDUNILVR: Hindustan Unilever LimitedDocument1 pageHINDUNILVR: Hindustan Unilever LimitedShyam SunderNo ratings yet

- Financial Results For Dec 31, 2013 (Result)Document4 pagesFinancial Results For Dec 31, 2013 (Result)Shyam Sunder0% (1)

- Mutual Fund Holdings in DHFLDocument7 pagesMutual Fund Holdings in DHFLShyam SunderNo ratings yet

- JUSTDIAL Mutual Fund HoldingsDocument2 pagesJUSTDIAL Mutual Fund HoldingsShyam SunderNo ratings yet

- Financial Results For September 30, 2013 (Result)Document2 pagesFinancial Results For September 30, 2013 (Result)Shyam SunderNo ratings yet

- Financial Results, Limited Review Report For December 31, 2015 (Result)Document4 pagesFinancial Results, Limited Review Report For December 31, 2015 (Result)Shyam SunderNo ratings yet

- Settlement Order in Respect of Bikaner Wooltex Pvt. Limited in The Matter of Sangam Advisors LimitedDocument2 pagesSettlement Order in Respect of Bikaner Wooltex Pvt. Limited in The Matter of Sangam Advisors LimitedShyam SunderNo ratings yet

- Order of Hon'ble Supreme Court in The Matter of The SaharasDocument6 pagesOrder of Hon'ble Supreme Court in The Matter of The SaharasShyam SunderNo ratings yet

- PR - Exit Order in Respect of Spice & Oilseeds Exchange Limited (Soel)Document1 pagePR - Exit Order in Respect of Spice & Oilseeds Exchange Limited (Soel)Shyam SunderNo ratings yet

- Financial Results & Limited Review Report For Sept 30, 2015 (Standalone) (Result)Document4 pagesFinancial Results & Limited Review Report For Sept 30, 2015 (Standalone) (Result)Shyam SunderNo ratings yet

- Settlement Order in Respect of R.R. Corporate Securities LimitedDocument2 pagesSettlement Order in Respect of R.R. Corporate Securities LimitedShyam SunderNo ratings yet

- Financial Results For June 30, 2013 (Audited) (Result)Document2 pagesFinancial Results For June 30, 2013 (Audited) (Result)Shyam SunderNo ratings yet

- Exit Order in Respect of The Spice and Oilseeds Exchange Limited, SangliDocument5 pagesExit Order in Respect of The Spice and Oilseeds Exchange Limited, SangliShyam SunderNo ratings yet

- Standalone Financial Results, Auditors Report For March 31, 2016 (Result)Document5 pagesStandalone Financial Results, Auditors Report For March 31, 2016 (Result)Shyam SunderNo ratings yet

- Financial Results & Limited Review Report For June 30, 2015 (Standalone) (Result)Document3 pagesFinancial Results & Limited Review Report For June 30, 2015 (Standalone) (Result)Shyam SunderNo ratings yet

- Financial Results For June 30, 2014 (Audited) (Result)Document3 pagesFinancial Results For June 30, 2014 (Audited) (Result)Shyam SunderNo ratings yet

- Standalone Financial Results For March 31, 2016 (Result)Document11 pagesStandalone Financial Results For March 31, 2016 (Result)Shyam SunderNo ratings yet

- Financial Results For Mar 31, 2014 (Result)Document2 pagesFinancial Results For Mar 31, 2014 (Result)Shyam SunderNo ratings yet

- Standalone Financial Results, Limited Review Report For September 30, 2016 (Result)Document4 pagesStandalone Financial Results, Limited Review Report For September 30, 2016 (Result)Shyam SunderNo ratings yet

- Standalone Financial Results, Limited Review Report For December 31, 2016 (Result)Document5 pagesStandalone Financial Results, Limited Review Report For December 31, 2016 (Result)Shyam SunderNo ratings yet

- Standalone Financial Results For September 30, 2016 (Result)Document3 pagesStandalone Financial Results For September 30, 2016 (Result)Shyam SunderNo ratings yet

- PDF Processed With Cutepdf Evaluation EditionDocument3 pagesPDF Processed With Cutepdf Evaluation EditionShyam SunderNo ratings yet

- Standalone Financial Results For June 30, 2016 (Result)Document2 pagesStandalone Financial Results For June 30, 2016 (Result)Shyam SunderNo ratings yet

- Standalone Financial Results, Limited Review Report For June 30, 2016 (Result)Document3 pagesStandalone Financial Results, Limited Review Report For June 30, 2016 (Result)Shyam SunderNo ratings yet

- Standalone Financial Results, Limited Review Report For September 30, 2016 (Result)Document4 pagesStandalone Financial Results, Limited Review Report For September 30, 2016 (Result)Shyam SunderNo ratings yet

- Standalone Financial Results, Limited Review Report For December 31, 2016 (Result)Document3 pagesStandalone Financial Results, Limited Review Report For December 31, 2016 (Result)Shyam SunderNo ratings yet

- Standalone Financial Results, Limited Review Report For June 30, 2016 (Result)Document4 pagesStandalone Financial Results, Limited Review Report For June 30, 2016 (Result)Shyam SunderNo ratings yet

- Investor Presentation For December 31, 2016 (Company Update)Document27 pagesInvestor Presentation For December 31, 2016 (Company Update)Shyam SunderNo ratings yet

- Transcript of The Investors / Analysts Con Call (Company Update)Document15 pagesTranscript of The Investors / Analysts Con Call (Company Update)Shyam SunderNo ratings yet

- Standalone Financial Results, Limited Review Report For December 31, 2016 (Result)Document4 pagesStandalone Financial Results, Limited Review Report For December 31, 2016 (Result)Shyam SunderNo ratings yet

- Global Financial ManagementDocument17 pagesGlobal Financial ManagementMamta GroverNo ratings yet

- The Consumer in The European UnionDocument12 pagesThe Consumer in The European UnionLagnajit Ayaskant SahooNo ratings yet

- Artículo para Poster Académico PDFDocument29 pagesArtículo para Poster Académico PDFDarío Guiñez ArenasNo ratings yet

- Break-Even Analysis: Fixed CostsDocument8 pagesBreak-Even Analysis: Fixed CostsDez DLNo ratings yet

- Marxism DissDocument18 pagesMarxism Dissok bloomerNo ratings yet

- Reading 5 Currency Exchange Rates - Understanding Equilibrium ValueDocument17 pagesReading 5 Currency Exchange Rates - Understanding Equilibrium Valuetristan.riolsNo ratings yet

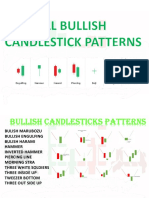

- All Bullish Candlestick Pattern by Optrading00 Telegram Optrading00Document25 pagesAll Bullish Candlestick Pattern by Optrading00 Telegram Optrading00Samitm TamhankarNo ratings yet

- Monetary Policy and Commercial Bank Lending Rates in KenyaDocument67 pagesMonetary Policy and Commercial Bank Lending Rates in KenyaGkou DojkuNo ratings yet

- Option Chain Manual FullDocument29 pagesOption Chain Manual FullProduction 18-22No ratings yet

- Can India Become A $5 Trillion Economy by 2024Document4 pagesCan India Become A $5 Trillion Economy by 2024Atul BishtNo ratings yet

- Economics Xi Unit-1 Chapter Wise Division of Marks Total TotalDocument10 pagesEconomics Xi Unit-1 Chapter Wise Division of Marks Total TotalPuja BhardwajNo ratings yet

- PDF EngDocument14 pagesPDF EngHimanshu SethNo ratings yet

- IMF and High Interest RatesDocument3 pagesIMF and High Interest RatesMIsiNo ratings yet

- Introduction To Finance Markets Investments and Financial Management 15th Edition Melicher Norton Solution ManualDocument19 pagesIntroduction To Finance Markets Investments and Financial Management 15th Edition Melicher Norton Solution ManualberthaNo ratings yet

- Unit 1 - Introduction - What Is Money STUDENTDocument19 pagesUnit 1 - Introduction - What Is Money STUDENTjevanjunior100% (1)

- Attraction of Foreign Investment To Ukraine: Problems and SolutionsDocument8 pagesAttraction of Foreign Investment To Ukraine: Problems and SolutionsHaval A.MamarNo ratings yet

- Cash Reserve Ratio: Economics Project by Ayush Dadawala and Suradnya PatilDocument14 pagesCash Reserve Ratio: Economics Project by Ayush Dadawala and Suradnya PatilSuradnya PatilNo ratings yet

- Introduction To Macroeconomics: Unit 1Document178 pagesIntroduction To Macroeconomics: Unit 1Navraj BhandariNo ratings yet

- Accounting For Real and Nominal Exchange Rate Movements in The Post-Bretton Woods PeriodDocument22 pagesAccounting For Real and Nominal Exchange Rate Movements in The Post-Bretton Woods PeriodStephanie GleasonNo ratings yet

- 6.1.6 PracticeDocument2 pages6.1.6 PracticeKyrieSwervingNo ratings yet

- Division of EconomicsDocument12 pagesDivision of EconomicsJoey, CPANo ratings yet

- David Ricardo's Influence on Economic ThoughtDocument30 pagesDavid Ricardo's Influence on Economic ThoughtBrendan RiceNo ratings yet

- INB 301 - Chapter 8 - Foreign Direct InvestmentDocument16 pagesINB 301 - Chapter 8 - Foreign Direct InvestmentS.M. YAMINUR RAHMANNo ratings yet

- Fiscal Policy Vs Monetary PolicyDocument2 pagesFiscal Policy Vs Monetary PolicyAkash Ray100% (1)

- BusPart B2 ExClassPracWS U3Document6 pagesBusPart B2 ExClassPracWS U3MARYLAND Pedagogical CoordinationNo ratings yet

- Government Programme 2020-2024Document53 pagesGovernment Programme 2020-2024L'express Maurice100% (1)

- Mock 19 HL Paper 1 MarkschemeDocument13 pagesMock 19 HL Paper 1 MarkschemesumitaNo ratings yet

- Mankiw9e Chap01 PDFDocument13 pagesMankiw9e Chap01 PDFCyrus SaadatNo ratings yet

- Provisional Program v2Document12 pagesProvisional Program v2Marios ZepseNo ratings yet

- International Liquidity & SDR and Global RecessionDocument31 pagesInternational Liquidity & SDR and Global Recessiongrigo4uNo ratings yet