You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Federal Reserve Routing Numbers and Bank DetailsDocument19 pagesFederal Reserve Routing Numbers and Bank DetailsPaul926875% (4)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Plaintiff's Opposition To US Bank DemurrerDocument19 pagesPlaintiff's Opposition To US Bank DemurrerCameron Totten100% (4)

- AMortizationDocument17 pagesAMortizationdela rosaNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- CMBSDocument115 pagesCMBSDesiderio Perez MayoNo ratings yet

- NHMFC Foreclosed Properties Housing Fair Aadhf05242019Document10 pagesNHMFC Foreclosed Properties Housing Fair Aadhf05242019Luis S Alvarez Jr67% (3)

- RES 3200 Chapter 5 Adjustable and Floating Rate Mortgage LoansDocument12 pagesRES 3200 Chapter 5 Adjustable and Floating Rate Mortgage LoansbaorunchenNo ratings yet

- Assignment Subprime MortgageDocument6 pagesAssignment Subprime MortgagemypinkladyNo ratings yet

- Missouri Association of Counties PACE ArticleDocument2 pagesMissouri Association of Counties PACE Article2391136No ratings yet

- Missouri Municipal Review Pace ArticleDocument2 pagesMissouri Municipal Review Pace Article2391136No ratings yet

- 7.22.10 PACE Banking CommitteeDocument28 pages7.22.10 PACE Banking Committee2391136No ratings yet

- NRDC ComplaintDocument23 pagesNRDC Complaint2391136No ratings yet

- Property Taxes On Owner-Occupied Housing, by State 2008Document10 pagesProperty Taxes On Owner-Occupied Housing, by State 20082391136No ratings yet

- AG Letter To PresidentDocument2 pagesAG Letter To President2391136No ratings yet

- CA Fhfa SuitDocument32 pagesCA Fhfa Suit2391136No ratings yet

- PHJW PACE White Paper 5.28.10 (Final)Document23 pagesPHJW PACE White Paper 5.28.10 (Final)2391136No ratings yet

- Fannie Mae Letter 052710-1Document2 pagesFannie Mae Letter 052710-12391136No ratings yet

- Recovery Through Retrofit ReportDocument14 pagesRecovery Through Retrofit Report2391136No ratings yet

- Promissory Note - Katherine Rose Frias - April 20, 2021Document5 pagesPromissory Note - Katherine Rose Frias - April 20, 2021khate friasNo ratings yet

- Memorandum of AgreementDocument2 pagesMemorandum of AgreementRalph AnitoNo ratings yet

- SEC Info - American Home Mortgage Assets Trust 2006-2-424B5 - On 7-7-06Document345 pagesSEC Info - American Home Mortgage Assets Trust 2006-2-424B5 - On 7-7-06scribdrichk100% (1)

- Office of The Punong Barangay: Agreement To PayDocument4 pagesOffice of The Punong Barangay: Agreement To PayBarangay CatoNo ratings yet

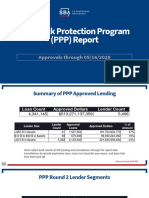

- PPP ReportDocument7 pagesPPP ReportBrittany EtheridgeNo ratings yet

- REG AB Static Pool & Structural Diagrams of Flow of FundsDocument22 pagesREG AB Static Pool & Structural Diagrams of Flow of FundsCarrieonicNo ratings yet

- ExhibithDocument21 pagesExhibithlarry-612445No ratings yet

- Maybank vs Tarrosa Spouses: Prescription of foreclosure actionDocument6 pagesMaybank vs Tarrosa Spouses: Prescription of foreclosure actionGab EstiadaNo ratings yet

- Affidavit (Mortgagee Bank) DHSUDDocument2 pagesAffidavit (Mortgagee Bank) DHSUDRodrigo MartinNo ratings yet

- Bank-In Dawhkan Atrangin Ka Loan An Reject..??: Pu Mapuia Hannah-I PaDocument1 pageBank-In Dawhkan Atrangin Ka Loan An Reject..??: Pu Mapuia Hannah-I PaPascal ChhakchhuakNo ratings yet

- 4-FAB Billing Statement Due Apr. 1, 2019 OCRDocument3 pages4-FAB Billing Statement Due Apr. 1, 2019 OCRlarry-612445No ratings yet

- Angel investor loan terms for startupDocument6 pagesAngel investor loan terms for startupxinNo ratings yet

- Teachers Demand Letters Division of Surigao del NorteDocument13 pagesTeachers Demand Letters Division of Surigao del NorteLex AmarieNo ratings yet

- Pike County Properties Sold ListDocument20 pagesPike County Properties Sold ListSheera LaineNo ratings yet

- Toyota Credit ApplicationDocument1 pageToyota Credit ApplicationCode JonNo ratings yet

- EXHIBIT A....... TP Inc V Bank of America NA/PRLAP/Jonathan JoynerDocument9 pagesEXHIBIT A....... TP Inc V Bank of America NA/PRLAP/Jonathan JoynerJames RimesNo ratings yet

- 12Document8 pages12Ishaq EssaNo ratings yet

- Home Loan Options Ebook EnglishDocument21 pagesHome Loan Options Ebook EnglishAbdul Wadood GharsheenNo ratings yet

- Long-Term Social Impacts and Financial Costs of Foreclosure On Families and Communities of ColorDocument49 pagesLong-Term Social Impacts and Financial Costs of Foreclosure On Families and Communities of ColorJH_CarrNo ratings yet

- An Unsavory Slice of SubprimeDocument3 pagesAn Unsavory Slice of SubprimeMuhammad MssNo ratings yet

- Irma - Nip Dan TMTDocument169 pagesIrma - Nip Dan TMTumeno umeniNo ratings yet

- Last Pay Certificate: No: No: L.F.FORM No.52Document1 pageLast Pay Certificate: No: No: L.F.FORM No.52JayaMadhavNo ratings yet

- C++ Loan ProgramDocument3 pagesC++ Loan ProgramNathan Kondor0% (2)