You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Basu and Dutta Accountancy Book Class 12 SolutionsDocument14 pagesBasu and Dutta Accountancy Book Class 12 SolutionsGourab Gorai23% (30)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Scheme Infants 2 Term 1Document47 pagesScheme Infants 2 Term 1api-478347207100% (2)

- Doku - Pub Zach Weinersmith Polystate v7Document73 pagesDoku - Pub Zach Weinersmith Polystate v7TommyNo ratings yet

- Singapore High Speed Rail Project 2017Document14 pagesSingapore High Speed Rail Project 2017Jigisha VasaNo ratings yet

- People V RapezaDocument41 pagesPeople V RapezaCathy BelgiraNo ratings yet

- Kahoat - Reshaping Medical SalesDocument4 pagesKahoat - Reshaping Medical SalesJatin KanatheNo ratings yet

- Development Plan: Jawaharlal Nehru Architecture and Fine Arts UniversityDocument13 pagesDevelopment Plan: Jawaharlal Nehru Architecture and Fine Arts Universityrenikunta varshiniNo ratings yet

- Beauchamp Thomas Understanding Teacher IdentityDocument16 pagesBeauchamp Thomas Understanding Teacher IdentityOswaldo Cabrera100% (1)

- Maximizing Your InfluenceDocument1 pageMaximizing Your InfluenceHosamKusbaNo ratings yet

- Car Modification and Accessories Business Plan Executive SummaryDocument9 pagesCar Modification and Accessories Business Plan Executive Summaryjunaidjavaid99No ratings yet

- HRM Jury Assignment - Part 1.case StudyDocument7 pagesHRM Jury Assignment - Part 1.case StudyNAMITHA KINo ratings yet

- Gems and Jewelry Industry: International Marketing inDocument13 pagesGems and Jewelry Industry: International Marketing inshilpichakravartyNo ratings yet

- Eapp Quarter 2 Module 3 (Jenny Mae D. Otto Grade 12 Abm-Yen)Document12 pagesEapp Quarter 2 Module 3 (Jenny Mae D. Otto Grade 12 Abm-Yen)Jenny Mae OttoNo ratings yet

- TimelineDocument2 pagesTimelinefranchesca latido100% (3)

- The 10th HouseDocument7 pagesThe 10th HouseRavindra LeleNo ratings yet

- Quirico Ungab Vs Vicente CusiDocument2 pagesQuirico Ungab Vs Vicente Cusiange ManagaytayNo ratings yet

- Mid Term Defense Updated SlidesDocument31 pagesMid Term Defense Updated SlidesRojash ShahiNo ratings yet

- Sarahdhobhany Resume PDFDocument1 pageSarahdhobhany Resume PDFAnonymous Uz535ScEMVNo ratings yet

- Long Quiz - TNCTDocument2 pagesLong Quiz - TNCTEditha ArabeNo ratings yet

- Udemy Business - The Skills That Will Define The Future of HRDocument24 pagesUdemy Business - The Skills That Will Define The Future of HRJimmy ChangNo ratings yet

- GDS Knowledge - InternDocument6 pagesGDS Knowledge - InternAbhishekNo ratings yet

- CV Muhammad Imran Riaz 1 P A G e MobiSerDocument3 pagesCV Muhammad Imran Riaz 1 P A G e MobiSerAmna Khan YousafzaiNo ratings yet

- MRS. Erlinda M. Ko, RN, BSNDocument5 pagesMRS. Erlinda M. Ko, RN, BSNPrince MonNo ratings yet

- Passed CGPA-7.2: Rohit Kumar Singh At-Plot-28 Vasundhara Vihar Society Iit Gate Kalyanpur Kanpur PIN-208017 (U.P)Document2 pagesPassed CGPA-7.2: Rohit Kumar Singh At-Plot-28 Vasundhara Vihar Society Iit Gate Kalyanpur Kanpur PIN-208017 (U.P)Rohit Singh100% (1)

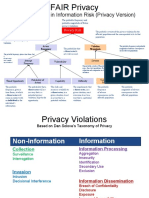

- Factor Analysis in Information Risk (Privacy Version)Document8 pagesFactor Analysis in Information Risk (Privacy Version)Otgonbayar TsengelNo ratings yet

- Ahsan Khan: Career ObjectiveDocument3 pagesAhsan Khan: Career ObjectivenomanNo ratings yet

- ITE182 Syllabus AY2020-2021 2ndsemDocument6 pagesITE182 Syllabus AY2020-2021 2ndsemLucman AbdulrachmanNo ratings yet

- Unit 2 Vocabulary-Đã NénDocument30 pagesUnit 2 Vocabulary-Đã NénThảo EmNo ratings yet

- History of Installation Art-Arh4472C: The Art Institute of FT Lauderdale Course SyllabusDocument3 pagesHistory of Installation Art-Arh4472C: The Art Institute of FT Lauderdale Course SyllabusLily FakhreddineNo ratings yet

- MSC Circ 1111Document36 pagesMSC Circ 1111Vincent Paul SantosNo ratings yet