You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- List of Registered Independent Sales OrganizationsDocument53 pagesList of Registered Independent Sales Organizationscdill70100% (1)

- Phil Guaranty v. CIR DigestsDocument2 pagesPhil Guaranty v. CIR Digestspinkblush717100% (1)

- Summer Training ReportDocument71 pagesSummer Training Reportbanti kumar50% (2)

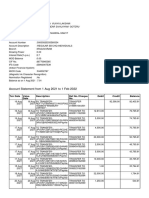

- Statement of AccountDocument1 pageStatement of AccountGopal AiranNo ratings yet

- A Study ON "360 Performance Appraisal" Icici Prudential PVT LTDDocument13 pagesA Study ON "360 Performance Appraisal" Icici Prudential PVT LTDbagyaNo ratings yet

- Exam Review - Chapters 4, 5, 6: Key Terms and Concepts To KnowDocument21 pagesExam Review - Chapters 4, 5, 6: Key Terms and Concepts To KnowDanica De VeraNo ratings yet

- Export Finance: Presented By: Tamanna M.FTECH 2010-12 NIFT, GandhinagarDocument19 pagesExport Finance: Presented By: Tamanna M.FTECH 2010-12 NIFT, Gandhinagartamanna88No ratings yet

- Tata Steel 09 Balance SheetDocument1 pageTata Steel 09 Balance SheetGoNo ratings yet

- A Study of Bank Audit ProcessDocument61 pagesA Study of Bank Audit ProcessSunil PawarNo ratings yet

- Malaysian citizens sought for Pan Borneo Highway rolesDocument15 pagesMalaysian citizens sought for Pan Borneo Highway rolesPolycarp Danson SigaiNo ratings yet

- Uday Kotak Letter PDFDocument3 pagesUday Kotak Letter PDFGurjeevNo ratings yet

- Compensation List PDFDocument7 pagesCompensation List PDFThe South Texas JournalNo ratings yet

- P.) UNIT 16 Cold Hard CashDocument36 pagesP.) UNIT 16 Cold Hard CashShalizzam SapuanNo ratings yet

- LC Business Overseas BranchesDocument202 pagesLC Business Overseas BranchesSumalNo ratings yet

- Auditing and Assurance Services A Systematic Approach 10th Edition Messier Test BankDocument54 pagesAuditing and Assurance Services A Systematic Approach 10th Edition Messier Test Banka742835559No ratings yet

- 3799 - 4000Document404 pages3799 - 4000DrPraveen Kumar TyagiNo ratings yet

- BSP Circular 1107Document7 pagesBSP Circular 1107Maya Julieta Catacutan-EstabilloNo ratings yet

- Fleet Bank HistoryDocument24 pagesFleet Bank HistoryScutty StarkNo ratings yet

- Icpu Registration FormDocument1 pageIcpu Registration FormGhulam AbbasNo ratings yet

- Ghana CHRAJ Investigation Report On MP Car LoansDocument26 pagesGhana CHRAJ Investigation Report On MP Car LoansKwakuazarNo ratings yet

- Abagon Company (Caselette)Document3 pagesAbagon Company (Caselette)Jodi Ann Echavia Alvarez0% (2)

- Incoterms, Export Process Guide for Importers & ExportersDocument2 pagesIncoterms, Export Process Guide for Importers & ExporterskanzulimanNo ratings yet

- Acceptance Letter After OfferDocument2 pagesAcceptance Letter After OfferRshar5No ratings yet

- Clinical Trials Insurance Proposal FormDocument8 pagesClinical Trials Insurance Proposal FormNamrathaNo ratings yet

- This Is The Sample Illustration Issued by HDFC Life Insurance Company LimitedDocument2 pagesThis Is The Sample Illustration Issued by HDFC Life Insurance Company Limitedsaurabh sumanNo ratings yet

- Master Policy Bond SPGIDocument17 pagesMaster Policy Bond SPGIDARSHAN ROYGAGANo ratings yet

- Certified Payment Processing SpecialistDocument5 pagesCertified Payment Processing SpecialistaNo ratings yet

- Implied Authority of A Partner: A Comparative Study: Assistant Professor of LawDocument20 pagesImplied Authority of A Partner: A Comparative Study: Assistant Professor of LawHimanshuNo ratings yet

- R DJVFuh 3 Ri LB 7 Ep RDocument13 pagesR DJVFuh 3 Ri LB 7 Ep RKondayya JuttigaNo ratings yet

- Abenson Summer Exclusives - Promo Mechanics PDFDocument2 pagesAbenson Summer Exclusives - Promo Mechanics PDFBon Alexis GuatatoNo ratings yet