You might also like

- Bond Prices and Interest RatesDocument27 pagesBond Prices and Interest RatesKoyakuNo ratings yet

- Chapter 3 Interest RateDocument15 pagesChapter 3 Interest RateEhab HosnyNo ratings yet

- The Role of Interest Rates and Money in the Keynesian SystemDocument20 pagesThe Role of Interest Rates and Money in the Keynesian SystemAlmasNo ratings yet

- Chapter 4. Present and Future ValueDocument43 pagesChapter 4. Present and Future ValueGirmay AbrhaNo ratings yet

- Managerial Finance chp5Document13 pagesManagerial Finance chp5Linda Mohammad FarajNo ratings yet

- Chapter 2: How Interest Rates Are DeterminedDocument62 pagesChapter 2: How Interest Rates Are DeterminedAykaNo ratings yet

- Corporate Finance Concepts and Valuation TechniquesDocument52 pagesCorporate Finance Concepts and Valuation TechniquesMD Hafizul Islam HafizNo ratings yet

- Lecture 7 9Document106 pagesLecture 7 9Nguyễn Thúy KiềuNo ratings yet

- BFW2140 Lecture Week 2: Corporate Financial Mathematics IDocument33 pagesBFW2140 Lecture Week 2: Corporate Financial Mathematics Iaa TANNo ratings yet

- Lecture 2Document21 pagesLecture 2Samantha YuNo ratings yet

- FINA2010 Financial Management: Lecture 3: Time Value of MoneyDocument62 pagesFINA2010 Financial Management: Lecture 3: Time Value of MoneymoonNo ratings yet

- FE Review - EconomyDocument26 pagesFE Review - EconomylonerstarNo ratings yet

- Time Value of Money - TVMDocument21 pagesTime Value of Money - TVMTh'bo Muzorewa ChizyukaNo ratings yet

- Time Value of Money Explained in 40 CharactersDocument78 pagesTime Value of Money Explained in 40 Charactersneha_baid_167% (3)

- Chapter 3 FMDocument79 pagesChapter 3 FMHananNo ratings yet

- Chapter 4 FinalDocument139 pagesChapter 4 FinaltomyidosaNo ratings yet

- Financial Markets QuestionsDocument54 pagesFinancial Markets QuestionsMathias VindalNo ratings yet

- Valuation of Cash Flows: Chapter 3.1-3.3Document66 pagesValuation of Cash Flows: Chapter 3.1-3.3harshnvicky123No ratings yet

- Fidelia Agatha - 2106715765 - Summary & Problem MK - Pertemuan Ke-4Document12 pagesFidelia Agatha - 2106715765 - Summary & Problem MK - Pertemuan Ke-4Fidelia AgathaNo ratings yet

- Introduction to Time Value of Money ConceptsDocument45 pagesIntroduction to Time Value of Money ConceptsAnkit DwivediNo ratings yet

- Lecture 3 - Time Value of MoneyDocument22 pagesLecture 3 - Time Value of MoneyJason LuximonNo ratings yet

- Midterm RevisionDocument27 pagesMidterm RevisionTrang CaoNo ratings yet

- Engineering Economics CH 2Document81 pagesEngineering Economics CH 2karim kobeissiNo ratings yet

- Module 2Document60 pagesModule 2lizNo ratings yet

- Strategic Capital Group Workshop #4: Bond ValuationDocument29 pagesStrategic Capital Group Workshop #4: Bond ValuationUniversity Securities Investment TeamNo ratings yet

- Intuition Behind The Present Value RuleDocument34 pagesIntuition Behind The Present Value RuleAbhishek MishraNo ratings yet

- L3 Future Value, Present Value & Compund InterestDocument5 pagesL3 Future Value, Present Value & Compund InterestvivianNo ratings yet

- InvLecture - W10-11 Capital BudgettingDocument264 pagesInvLecture - W10-11 Capital BudgettingJuan Camilo Gómez RobayoNo ratings yet

- L1 Fixed Income Markets (v2)Document44 pagesL1 Fixed Income Markets (v2)Kruti BhattNo ratings yet

- Bond FundamentalsDocument19 pagesBond FundamentalsInstiRevenNo ratings yet

- Time Value of MoneyDocument73 pagesTime Value of MoneyZeenat NoorNo ratings yet

- Exercises For Revision With SolutionDocument4 pagesExercises For Revision With SolutionThùy LinhhNo ratings yet

- Engineering Economics Lect 2Document31 pagesEngineering Economics Lect 2Furqan ChaudhryNo ratings yet

- The Time Value of MoneyDocument39 pagesThe Time Value of MoneyAbhinav JainNo ratings yet

- Fixed IncomeDocument36 pagesFixed IncomeAnkit ShahNo ratings yet

- Techniques of Asset/liability Management: Futures, Options, and SwapsDocument43 pagesTechniques of Asset/liability Management: Futures, Options, and SwapsSushmita BarlaNo ratings yet

- 2023 Time Value of MoneyDocument81 pages2023 Time Value of Moneylynthehunkyapple205No ratings yet

- Time Value of Money-PowerpointDocument83 pagesTime Value of Money-Powerpointhaljordan313No ratings yet

- Principles of Managerial Finance Chapter 5 Time Value of MoneyDocument45 pagesPrinciples of Managerial Finance Chapter 5 Time Value of MoneyJoshNo ratings yet

- The Keynesian System (Money, Interest and Income)Document59 pagesThe Keynesian System (Money, Interest and Income)Almas100% (1)

- CFDocument11 pagesCFPreetesh ChoudhariNo ratings yet

- 7.2 Bond ValuationDocument59 pages7.2 Bond ValuationAlperen KaragozNo ratings yet

- Lecture 02dm Time Value of MoneyDocument42 pagesLecture 02dm Time Value of Moneylja92No ratings yet

- CF - 04Document54 pagesCF - 04Нндн Н'No ratings yet

- Chapter 5 and 6 Bond Characteristics and PricingDocument29 pagesChapter 5 and 6 Bond Characteristics and PricingSamantha YuNo ratings yet

- TVM: Calculating Present and Future ValuesDocument60 pagesTVM: Calculating Present and Future ValuesZain AbbasNo ratings yet

- Power Notes: Bonds Payable and Investments in BondsDocument38 pagesPower Notes: Bonds Payable and Investments in BondsiVONo ratings yet

- Understanding Interest RatesDocument19 pagesUnderstanding Interest RatesAmsalu WalelignNo ratings yet

- The Concepts of Return and Value-Explained-PppDocument48 pagesThe Concepts of Return and Value-Explained-PppJcharlesvNo ratings yet

- Bonds and Their ValuationDocument41 pagesBonds and Their ValuationRenz Ian DeeNo ratings yet

- Time Value of MoneyDocument47 pagesTime Value of MoneyPrashant JhakarwarNo ratings yet

- WK13-14 Valuation and Rates of ReturnDocument49 pagesWK13-14 Valuation and Rates of ReturnJAEZAR PHILIP GRAGASINNo ratings yet

- Engineering Economics Lect 3Document43 pagesEngineering Economics Lect 3Furqan ChaudhryNo ratings yet

- Compound Interest, Future Value, and Present Value: - When Money Is Borrowed, The Amount Borrowed Is Known As TheDocument41 pagesCompound Interest, Future Value, and Present Value: - When Money Is Borrowed, The Amount Borrowed Is Known As ThetwinklenoorNo ratings yet

- Timevalueofmoney 160502121318Document30 pagesTimevalueofmoney 160502121318S BALAJI VH10788No ratings yet

- Chapter 6 NotesDocument6 pagesChapter 6 NoteshannahandrearosarioNo ratings yet

- Chapter 3.1Document47 pagesChapter 3.1Aschenaki MebreNo ratings yet

- Time Value of MoneyDocument17 pagesTime Value of Moneyyolanda monikaNo ratings yet

- Econ Course 202 Academy SayDocument909 pagesEcon Course 202 Academy SayKoyakuNo ratings yet

- Example Example: (5.5) : Continuation of (5.4)Document22 pagesExample Example: (5.5) : Continuation of (5.4)KoyakuNo ratings yet

- Current Labor MarketDocument42 pagesCurrent Labor MarketKoyakuNo ratings yet

- Wage Determination: Collective BargainingDocument46 pagesWage Determination: Collective BargainingKoyakuNo ratings yet

- Investment and The Stock Market: Stock Capital Same Same StockDocument32 pagesInvestment and The Stock Market: Stock Capital Same Same StockKoyakuNo ratings yet

- Determination of The Optimal Capital InvestmentDocument34 pagesDetermination of The Optimal Capital InvestmentKoyakuNo ratings yet

- Shifts of The Curve: Price Level Money Supply ExogenousDocument28 pagesShifts of The Curve: Price Level Money Supply ExogenousKoyakuNo ratings yet

- Money: Assets PaymentDocument25 pagesMoney: Assets PaymentKoyakuNo ratings yet

- Learning ObjectivesDocument33 pagesLearning ObjectivesKoyakuNo ratings yet

- Saving and Wealth Over The Life Cycle: Income High Low Short Long Together Constant ConstantDocument29 pagesSaving and Wealth Over The Life Cycle: Income High Low Short Long Together Constant ConstantKoyakuNo ratings yet

- Consumption: Disposable IncomeDocument49 pagesConsumption: Disposable IncomeKoyakuNo ratings yet

- Market For Goods in The Classical Model: Lower Discourages EncouragesDocument28 pagesMarket For Goods in The Classical Model: Lower Discourages EncouragesKoyakuNo ratings yet

- The Determination of Equilibrium Output in A Graph: Building Output Fiscal Policy Income Production Equal IncomeDocument33 pagesThe Determination of Equilibrium Output in A Graph: Building Output Fiscal Policy Income Production Equal IncomeKoyakuNo ratings yet

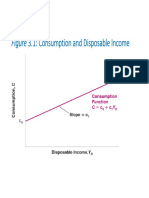

- Figure 3.1: Consumption and Disposable IncomeDocument33 pagesFigure 3.1: Consumption and Disposable IncomeKoyakuNo ratings yet

- Money Demand Function: Increase Increases Reduces Increase Increases Reduces One For OneDocument30 pagesMoney Demand Function: Increase Increases Reduces Increase Increases Reduces One For OneKoyakuNo ratings yet

- The Government Sector: - Income Taxes and Automatic StabilizersDocument44 pagesThe Government Sector: - Income Taxes and Automatic StabilizersKoyakuNo ratings yet

- Borrowing Constraints: - SameDocument29 pagesBorrowing Constraints: - SameKoyakuNo ratings yet

- Fins 3616 Chapter 4Document5 pagesFins 3616 Chapter 4Iris LauNo ratings yet

- Money SupplyDocument8 pagesMoney Supplyladankur23No ratings yet

- PS7 Primera ParteDocument5 pagesPS7 Primera PartethomasNo ratings yet

- Assessing Economic Condition Chapter 3Document43 pagesAssessing Economic Condition Chapter 3Zeeshan AfzalNo ratings yet

- Inflation: Prices On The RiseDocument1 pageInflation: Prices On The RiseMicheleFontanaNo ratings yet

- Final Project TybmsDocument57 pagesFinal Project TybmsAnkit Chaurasiya50% (2)

- Notes NismDocument182 pagesNotes NismMCQ NISMNo ratings yet

- Quantity Theory of MoneyDocument10 pagesQuantity Theory of Moneyrabia liaqatNo ratings yet

- Sources of FinanceDocument32 pagesSources of FinanceVikas RajNo ratings yet

- Instructional Module: Republic of The Philippines Nueva Vizcaya State University Bayombong, Nueva VizcayaDocument29 pagesInstructional Module: Republic of The Philippines Nueva Vizcaya State University Bayombong, Nueva VizcayaAISLINENo ratings yet

- How Billionaires Build Wealth and LegacyDocument36 pagesHow Billionaires Build Wealth and LegacyRich Diaz100% (24)

- Notes To Consolidated Financial Statements: Department of EducationDocument65 pagesNotes To Consolidated Financial Statements: Department of EducationEmosNo ratings yet

- Chapter 17 Summary Principles of MacroeconomicsDocument9 pagesChapter 17 Summary Principles of MacroeconomicsOLFA ALOUININo ratings yet

- Engineering EconomicsDocument161 pagesEngineering EconomicsggrNo ratings yet

- Report On Interest Rates in NepalDocument12 pagesReport On Interest Rates in NepalRupesh Shah100% (2)

- Henex New Letter 19 NOv 2022Document21 pagesHenex New Letter 19 NOv 2022Vivek AgNo ratings yet

- Hospitality Financial Management Ch.3-Current Asset ManagementDocument14 pagesHospitality Financial Management Ch.3-Current Asset ManagementMuhammad Salihin Jaafar0% (1)

- RBI Format ROI PC PDFDocument9 pagesRBI Format ROI PC PDFmohana sundaram pNo ratings yet

- Module 5Document14 pagesModule 5Sittie Nihaya MangondayaNo ratings yet

- The Mathematics of FinanceDocument29 pagesThe Mathematics of FinanceSherie LynneNo ratings yet

- Market Insight Credit Strategies End CycleDocument4 pagesMarket Insight Credit Strategies End CycledhyakshaNo ratings yet

- Central Banks Take Extreme Action To Stave Off Deflation: The Long Game Tall Tales Candidate of ChangeDocument32 pagesCentral Banks Take Extreme Action To Stave Off Deflation: The Long Game Tall Tales Candidate of ChangestefanoNo ratings yet

- Topic 4 Mathematics of FinanceDocument66 pagesTopic 4 Mathematics of FinanceAndrew PillayNo ratings yet

- Relationship Between Inflation and Price of CommodityDocument41 pagesRelationship Between Inflation and Price of CommoditydhruvgujaratiNo ratings yet

- Central Bank Functions and Interest RatesDocument19 pagesCentral Bank Functions and Interest RatesNiranjan KumavatNo ratings yet

- Mercial PaperDocument39 pagesMercial PaperArjun Khunt100% (1)

- 10 InclassDocument50 pages10 InclassTNo ratings yet

- 8765511.1 1 CostofBorrowingPackage 20201230 095517HPMZWDocument7 pages8765511.1 1 CostofBorrowingPackage 20201230 095517HPMZWsabNo ratings yet

- Time Value of Money - Engineering Economics.Document59 pagesTime Value of Money - Engineering Economics.Quach Nguyen100% (4)

- TIME VALUE OF MONEY EXPLAINEDDocument17 pagesTIME VALUE OF MONEY EXPLAINEDArafatNo ratings yet