You might also like

- CPA exam review: Key provisions of the Philippine Accountancy ActDocument12 pagesCPA exam review: Key provisions of the Philippine Accountancy ActJudy Ann ImusNo ratings yet

- Audit Theory QuizzerDocument71 pagesAudit Theory QuizzerKriztleKateMontealtoGelogoNo ratings yet

- Ra 9298 Accountancy Act of 2004Document10 pagesRa 9298 Accountancy Act of 2004Jerome Reyes100% (1)

- RA9298 and Professional Practice of AccountingDocument12 pagesRA9298 and Professional Practice of Accountinglouise carino100% (2)

- Audit Theory - QuizzerDocument36 pagesAudit Theory - QuizzerCharis Marie UrgelNo ratings yet

- QUEZON CITY UNIVERSITY ACCOUNTING EXAMDocument8 pagesQUEZON CITY UNIVERSITY ACCOUNTING EXAMJennifer RasonabeNo ratings yet

- Professional Practice of Accounting With AnswerDocument12 pagesProfessional Practice of Accounting With AnswerRNo ratings yet

- RA 9298 - KEY POINTS ON PHILIPPINE ACCOUNTANCY ACTDocument10 pagesRA 9298 - KEY POINTS ON PHILIPPINE ACCOUNTANCY ACTJyznareth TapiaNo ratings yet

- At Professional Responsibilities and Other Topics With AnswersDocument27 pagesAt Professional Responsibilities and Other Topics With AnswersShielle AzonNo ratings yet

- Quality Control SystemDocument4 pagesQuality Control SystemGlessey Mae Baito LuvidicaNo ratings yet

- CPA Review: Code of Ethics for Professional Accountants in the PhilippinesDocument20 pagesCPA Review: Code of Ethics for Professional Accountants in the PhilippinesJedidiah SmithNo ratings yet

- Internal Control QuizDocument7 pagesInternal Control Quizlouise carino100% (2)

- The Accountancy Profession QuizDocument4 pagesThe Accountancy Profession Quizsharon5lotinoNo ratings yet

- RA 9298 - Powerpoint PresentationDocument60 pagesRA 9298 - Powerpoint PresentationCharrie Grace Pablo100% (3)

- Auditing Theory AuditDocument77 pagesAuditing Theory AuditAdam Smith0% (1)

- Aud EvidenceDocument14 pagesAud EvidenceJadeNo ratings yet

- Auditing Theory Test BankDocument9 pagesAuditing Theory Test BankTricia Mae FernandezNo ratings yet

- Department of Accountancy: Page - 1Document14 pagesDepartment of Accountancy: Page - 1NoroNo ratings yet

- Public and Professional AccountingDocument5 pagesPublic and Professional Accountingemc2_mcvNo ratings yet

- Auditing Theory: (Test Bank) Gerardo S. RoqueDocument82 pagesAuditing Theory: (Test Bank) Gerardo S. RoqueYukiNo ratings yet

- Answer Key: Chapter 06 Audit Planning, Understanding The Client, Assessing Risks, and RespondingDocument25 pagesAnswer Key: Chapter 06 Audit Planning, Understanding The Client, Assessing Risks, and RespondingRalph Santos100% (2)

- The Regulation and Practice of the Accountancy ProfessionDocument14 pagesThe Regulation and Practice of the Accountancy ProfessionRhia Mae Pacelo100% (1)

- Auditing Theory Test BankDocument7 pagesAuditing Theory Test BankjaysonNo ratings yet

- Comprehensive Reviewer: Auditing Theory and Assurance ServicesDocument54 pagesComprehensive Reviewer: Auditing Theory and Assurance ServicesMc Bryan Barlizo100% (2)

- Revenue Receipt Cycle Audit TestsDocument14 pagesRevenue Receipt Cycle Audit TestsMelanie SamsonaNo ratings yet

- AT Quizzer 1 Overview of Auditing Answer Key PDFDocument11 pagesAT Quizzer 1 Overview of Auditing Answer Key PDFKimyMalaya100% (5)

- Audit Chapter 7 MCDocument11 pagesAudit Chapter 7 MCNanon WiwatwongthornNo ratings yet

- Successor Auditor ResponsibilitiesDocument5 pagesSuccessor Auditor ResponsibilitiesVergel MartinezNo ratings yet

- Feu - MakatiDocument15 pagesFeu - MakatiRica RegorisNo ratings yet

- Final Board Simulation - RFBT (With Answer Key)Document14 pagesFinal Board Simulation - RFBT (With Answer Key)Maria Kem Eumague100% (3)

- Attestation Services 2Document8 pagesAttestation Services 2sana olNo ratings yet

- MANAGEMENT ADVISORY SERVICES BREAKEVENDocument46 pagesMANAGEMENT ADVISORY SERVICES BREAKEVENJoy Bernadette GruesoNo ratings yet

- Wiley Auditing Reviewer MockboardDocument21 pagesWiley Auditing Reviewer MockboardAmir Macarongon100% (1)

- Mas Test BankDocument23 pagesMas Test BankFrancine Holler100% (1)

- AT Q1 Pre-Week - MAY 2019Document17 pagesAT Q1 Pre-Week - MAY 2019Aj Pacaldo100% (3)

- CDD - Semi Finals Examination - Auditing TheoryDocument14 pagesCDD - Semi Finals Examination - Auditing TheoryFeelingerang MAYoraNo ratings yet

- Audit Sampling MCQsDocument8 pagesAudit Sampling MCQsChelsy SantosNo ratings yet

- Final ExamDocument59 pagesFinal ExamME ValleserNo ratings yet

- Z 2Document12 pagesZ 2Helios HexNo ratings yet

- Q1 - Philippine Accountancy Act of 2004, Code of EthicsDocument10 pagesQ1 - Philippine Accountancy Act of 2004, Code of EthicsPrankyJellyNo ratings yet

- Z 1Document12 pagesZ 1Helios HexNo ratings yet

- Philippine Accountancy Act of 2004 (RA 9298Document4 pagesPhilippine Accountancy Act of 2004 (RA 9298Anna ParciaNo ratings yet

- ATQ1SCBD2Document11 pagesATQ1SCBD2Helios HexNo ratings yet

- Philippine Government Agencies and Professional OrganizationsDocument6 pagesPhilippine Government Agencies and Professional OrganizationsjuennaguecoNo ratings yet

- Answer Key Assignment For Chapter 3Document8 pagesAnswer Key Assignment For Chapter 3John Lester DungcaNo ratings yet

- At Quizzer 2 Profl Practice of Acctg 2SAY1920 PDFDocument12 pagesAt Quizzer 2 Profl Practice of Acctg 2SAY1920 PDFMina MyouiNo ratings yet

- At Reviewer PT 1Document18 pagesAt Reviewer PT 1lender kent alicanteNo ratings yet

- PH Accountancy Act of 2004 (RA9298) - Code of EthicsDocument8 pagesPH Accountancy Act of 2004 (RA9298) - Code of EthicsHaks MashtiNo ratings yet

- AUDIT 2019 - CompilationDocument73 pagesAUDIT 2019 - CompilationKriztle Kate GelogoNo ratings yet

- Semi Answered Aud TheoryDocument11 pagesSemi Answered Aud TheoryAbdulmajed Unda MimbantasNo ratings yet

- Logo Here Auditing Theory Philippine Accountancy Act of 2004Document35 pagesLogo Here Auditing Theory Philippine Accountancy Act of 2004KathleenCusipagNo ratings yet

- AT Quizzer 2 - Profl Practice of Acctg - Summer 2020 PDFDocument12 pagesAT Quizzer 2 - Profl Practice of Acctg - Summer 2020 PDFJohn Carlo CruzNo ratings yet

- CPA's Professional Responsibilities and Ethics under RA 9298Document4 pagesCPA's Professional Responsibilities and Ethics under RA 9298elle868No ratings yet

- Philippine Accountancy Act of 2004Document6 pagesPhilippine Accountancy Act of 2004jeromyNo ratings yet

- PUP Taguig CPA Licensure Exam ReviewDocument10 pagesPUP Taguig CPA Licensure Exam ReviewAbraham Mayo MakakuaNo ratings yet

- SCBDATQ2Document10 pagesSCBDATQ2Helios HexNo ratings yet

- Auditing Theory QuizDocument7 pagesAuditing Theory QuizKIM RAGANo ratings yet

- Summative Assessment-IntactDocument5 pagesSummative Assessment-IntactNhel AlvaroNo ratings yet

- Auditing Practice QuestionsDocument49 pagesAuditing Practice QuestionsBeaNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: 2016 EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: 2016 EditionNo ratings yet

- Multiple Choice - Problems 1Document5 pagesMultiple Choice - Problems 1KatKat Olarte100% (1)

- Chapter 1 - TBTDocument10 pagesChapter 1 - TBTKatKat OlarteNo ratings yet

- Chapter 5 - TBTDocument8 pagesChapter 5 - TBTKatKat Olarte100% (2)

- Conceptual FrameworkDocument65 pagesConceptual FrameworkKatKat OlarteNo ratings yet

- Chapter 7 - TBTDocument14 pagesChapter 7 - TBTKatKat Olarte0% (3)

- CHAPTER 13A - Transfer and Business TaxDocument20 pagesCHAPTER 13A - Transfer and Business TaxKatKat Olarte80% (5)

- Chapter 10 - TBTDocument11 pagesChapter 10 - TBTKatKat Olarte100% (4)

- Multiple Choice Problems on Estate TaxationDocument9 pagesMultiple Choice Problems on Estate TaxationKatKat Olarte67% (3)

- Multiple-Choice Problems on Business TaxationDocument6 pagesMultiple-Choice Problems on Business TaxationKatKat Olarte0% (1)

- BASF Catalysts - Leveraging Innovation to Serve Growing MarketsDocument18 pagesBASF Catalysts - Leveraging Innovation to Serve Growing Marketsccnew3000No ratings yet

- Excel calendarDocument28 pagesExcel calendarThanh LêNo ratings yet

- Some Thoughts On The Failure of Silicon Valley Bank 3-12-2023Document4 pagesSome Thoughts On The Failure of Silicon Valley Bank 3-12-2023Subash NehruNo ratings yet

- GBS750 Assignment 1Document7 pagesGBS750 Assignment 1Kasimba MwandilaNo ratings yet

- Paris Region Facts and Figures. 2020 EditionDocument44 pagesParis Region Facts and Figures. 2020 EditionJerson ValenciaNo ratings yet

- SBI Life Insurance receipt for Rs. 100,000 premium paymentDocument1 pageSBI Life Insurance receipt for Rs. 100,000 premium paymentmanish sharmaNo ratings yet

- Pre-Feasibility Report for Kempegowda International Airport ExpansionDocument103 pagesPre-Feasibility Report for Kempegowda International Airport Expansionprerana anuNo ratings yet

- Chapter 3 PlanningDocument29 pagesChapter 3 PlanningDagm alemayehuNo ratings yet

- AbstrakDocument7 pagesAbstrakAldy SolawatNo ratings yet

- 7 Stages or Steps Involved in Marketing Research ProcessDocument8 pages7 Stages or Steps Involved in Marketing Research Processaltaf_catsNo ratings yet

- Weekly: Join in Our Telegram Channel - T.Me/Equity99Document6 pagesWeekly: Join in Our Telegram Channel - T.Me/Equity99Hitendra PanchalNo ratings yet

- Naamm Stair Manual FinalDocument126 pagesNaamm Stair Manual FinalAhmed BdairNo ratings yet

- MAS Reviewer: Key Financial FormulasDocument6 pagesMAS Reviewer: Key Financial FormulasAnna AldaveNo ratings yet

- Chapter 02 - Rosenbloom 8edDocument28 pagesChapter 02 - Rosenbloom 8edAlyssa BasilioNo ratings yet

- Alpha Graphics CompanyDocument2 pagesAlpha Graphics CompanyMira FebriasariNo ratings yet

- Topic 3 Long-Term Construction Contracts ModuleDocument20 pagesTopic 3 Long-Term Construction Contracts ModuleMaricel Ann BaccayNo ratings yet

- Nct-Rex Inspired ThemeDocument11 pagesNct-Rex Inspired ThemeFania SafitriNo ratings yet

- Transport Economics Individual Assignemnt FinalDocument6 pagesTransport Economics Individual Assignemnt FinalBlessing MapokaNo ratings yet

- Modern Data Strategy 1664949335Document39 pagesModern Data Strategy 1664949335Dao NguyenNo ratings yet

- Marketing Plan Energypac FinalDocument39 pagesMarketing Plan Energypac FinalMmr MishuNo ratings yet

- Comprof PT. Indo Kida PlatingDocument16 pagesComprof PT. Indo Kida PlatingAreIf Cron BmxStreetNo ratings yet

- IFRS 11 and 12 CPD September 2013Document64 pagesIFRS 11 and 12 CPD September 2013Nicolaus CopernicusNo ratings yet

- Essay 2Document18 pagesEssay 2Yee ting laiNo ratings yet

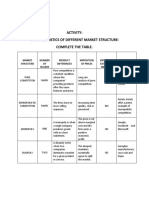

- Characteristics of Different Market Structures TableDocument2 pagesCharacteristics of Different Market Structures TableJustine PadohilaoNo ratings yet

- Uploads - Notes - Btech - 4sem - It - DBMS FRONT PAGE LAB MANUALDocument3 pagesUploads - Notes - Btech - 4sem - It - DBMS FRONT PAGE LAB MANUALKushNo ratings yet

- Research Project On Kross CycleDocument18 pagesResearch Project On Kross CycleRAJAN SINGHNo ratings yet

- Explanatory Notes For AEO SAQDocument74 pagesExplanatory Notes For AEO SAQthrowaway12544234No ratings yet

- The Waldorf Hilton Hotel Job Offered Contract LetterDocument3 pagesThe Waldorf Hilton Hotel Job Offered Contract LetterHIsham Ali100% (2)

- Axe Deodorant Marketing-2Document10 pagesAxe Deodorant Marketing-2moshin qureshiNo ratings yet

- Canara - Epassbook - 2023-10-10 202024.654466Document49 pagesCanara - Epassbook - 2023-10-10 202024.654466Kamal Hossain MondalNo ratings yet