You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- U.S. Individual Income Tax Return: Cruz 605-92-4936 Luis EDocument21 pagesU.S. Individual Income Tax Return: Cruz 605-92-4936 Luis ELui67% (3)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- PWC Oil Gas Guide 2019 PDFDocument148 pagesPWC Oil Gas Guide 2019 PDFRafael DamarNo ratings yet

- Luzon Stevedoring Corp vs. CTADocument2 pagesLuzon Stevedoring Corp vs. CTAmaximum jicaNo ratings yet

- Confirmation For Booking ID # 409849089 Check-In (Arrival)Document1 pageConfirmation For Booking ID # 409849089 Check-In (Arrival)CahyoNo ratings yet

- Writing Tips - CaeDocument16 pagesWriting Tips - CaeRachael FranklinNo ratings yet

- Administrative Law - Smart NotesDocument65 pagesAdministrative Law - Smart NotesAchyut TewariNo ratings yet

- Request For Proposals: Jalkhad (SNJ) Road (KM 12+000 To 49+000) Length: 37 KM"Document1 pageRequest For Proposals: Jalkhad (SNJ) Road (KM 12+000 To 49+000) Length: 37 KM"Munir HussainNo ratings yet

- INCOMEDocument12 pagesINCOMEaviralmittuNo ratings yet

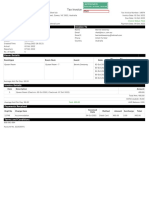

- Invoice Apartmentsglenisla 14874Document1 pageInvoice Apartmentsglenisla 14874Ronnie HatiNo ratings yet

- Economics and Business EnvironmentDocument70 pagesEconomics and Business Environmentm agarwalNo ratings yet

- Rift Valley University Hawassa Campus Master of Business Administration Program Assignment On Human Resource ManagementDocument12 pagesRift Valley University Hawassa Campus Master of Business Administration Program Assignment On Human Resource ManagementHACHALU FAYENo ratings yet

- IT Calculation Sheet (2013-14) - Word 2007 FormatDocument9 pagesIT Calculation Sheet (2013-14) - Word 2007 FormatMuthur Ramasamy KuppusamyNo ratings yet

- M&S 2023 Annual ReportDocument236 pagesM&S 2023 Annual ReportMANo ratings yet

- Consti Law Art VI ReviewerDocument8 pagesConsti Law Art VI ReviewerKhenz MistalNo ratings yet

- Daily US Treasury Statement 4/12/11Document2 pagesDaily US Treasury Statement 4/12/11Darla DawaldNo ratings yet

- 2modules 1 and 2 - Taxation 1Document6 pages2modules 1 and 2 - Taxation 1Gerard Relucio OroNo ratings yet

- Public CHAPTER 4Document15 pagesPublic CHAPTER 4embiale ayaluNo ratings yet

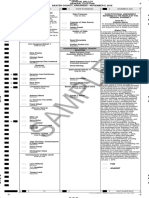

- Sample: Official Ballot General Election Baxter County, Arkansas - November 6, 2018Document2 pagesSample: Official Ballot General Election Baxter County, Arkansas - November 6, 2018Sonny ElliottNo ratings yet

- FTN211466605255Document2 pagesFTN211466605255Varu NayanNo ratings yet

- EVA Financial Management at Godrej Consumer Products LTDDocument28 pagesEVA Financial Management at Godrej Consumer Products LTDRahul SaraogiNo ratings yet

- Output Vat Zero-Rated Sales ch8Document3 pagesOutput Vat Zero-Rated Sales ch8Marionne GNo ratings yet

- Ingersoll Rand Onboard Power Vhp40rmh Operation Maintenance Manual 2012Document23 pagesIngersoll Rand Onboard Power Vhp40rmh Operation Maintenance Manual 2012mistythompson020399sdz100% (28)

- G.R. No. 158540 PDFDocument43 pagesG.R. No. 158540 PDFMariz PatanaoNo ratings yet

- Dividends and The Dividend ExemptionDocument1 pageDividends and The Dividend ExemptionSunny KirpalaniNo ratings yet

- Elasticity and InelasticityDocument2 pagesElasticity and InelasticityKarl BrattNo ratings yet

- Examples Transfer PricingDocument15 pagesExamples Transfer PricingRajat RathNo ratings yet

- SITXGLC001 AnswersDocument5 pagesSITXGLC001 AnswersShivam Anand ShuklaNo ratings yet

- Book CaseDocument11 pagesBook CaseW HWNo ratings yet

- Abxxxxxxxd q4 2022-23Document4 pagesAbxxxxxxxd q4 2022-23pchak.sbiNo ratings yet