You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Productivity and QMDocument78 pagesProductivity and QMDhananjay SharmaNo ratings yet

- The Ethics of Marketing and Public RelationsDocument34 pagesThe Ethics of Marketing and Public RelationsDhananjay SharmaNo ratings yet

- The Price of Copyright ViolationDocument21 pagesThe Price of Copyright ViolationDhananjay SharmaNo ratings yet

- Ob13 10Document17 pagesOb13 10Nazish Afzal Sohail BhuttaNo ratings yet

- HRM Notes Chapter 1 IntroductionDocument51 pagesHRM Notes Chapter 1 IntroductionDhananjay SharmaNo ratings yet

- Success Count Actor All TimeDocument13 pagesSuccess Count Actor All TimeDhananjay SharmaNo ratings yet

- Trade Policy ExplainedDocument43 pagesTrade Policy ExplainedDhananjay SharmaNo ratings yet

- Social SecurityDocument8 pagesSocial SecurityDhananjay SharmaNo ratings yet

- Basic NetworkingDocument6 pagesBasic Networkingapi-3728785No ratings yet

- Career Planning and Development: IntroductionDocument16 pagesCareer Planning and Development: Introductionsonu1296No ratings yet

- WarehousingDocument25 pagesWarehousingDhananjay SharmaNo ratings yet

- HRM NotesDocument70 pagesHRM NotesDhananjay Sharma100% (1)

- HRM NotesDocument63 pagesHRM NotesDhananjay Sharma100% (1)

- Productivity Quality Management Notes What Method StudyDocument9 pagesProductivity Quality Management Notes What Method StudyDhananjay SharmaNo ratings yet

- Trends and Challenges in the Globalisation of the Banking SectorDocument9 pagesTrends and Challenges in the Globalisation of the Banking SectorDhananjay SharmaNo ratings yet

- Productivity Quality Management Notes What QualityDocument6 pagesProductivity Quality Management Notes What QualityDhananjay SharmaNo ratings yet

- Credit Ratings Agencies in IndiaDocument2 pagesCredit Ratings Agencies in IndiaDhananjay SharmaNo ratings yet

- Productivity Quality Management NotesDocument3 pagesProductivity Quality Management NotesDhananjay SharmaNo ratings yet

- Dress CodeDocument3 pagesDress CodeSaji DevassyNo ratings yet

- Preparing To Meet MediaDocument11 pagesPreparing To Meet MediaDhananjay SharmaNo ratings yet

- Chap 13 - How PR Supports Marketing Mix & Relationship BuildingDocument15 pagesChap 13 - How PR Supports Marketing Mix & Relationship BuildingDhananjay SharmaNo ratings yet

- 100 Marks Project On Export Procedure and Documentation Finally CompletedDocument132 pages100 Marks Project On Export Procedure and Documentation Finally Completedsaeesagar72% (43)

- Concept of PRDocument11 pagesConcept of PRamit_singhalNo ratings yet

- Public RelationsDocument2 pagesPublic RelationsDhananjay SharmaNo ratings yet

- Marketing cooperatives optimize farm salesDocument11 pagesMarketing cooperatives optimize farm salesxtremebirajNo ratings yet

- Corporate Social Responsibility Versus Corporate CitizenshipDocument11 pagesCorporate Social Responsibility Versus Corporate CitizenshipDhananjay SharmaNo ratings yet

- Export DocumentationDocument10 pagesExport DocumentationCharu ModiNo ratings yet

- Marketing Co OperativeDocument7 pagesMarketing Co OperativeDhananjay SharmaNo ratings yet

- Problems & Remedies of Co-Operative MarketingDocument3 pagesProblems & Remedies of Co-Operative MarketingDhananjay SharmaNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- VILLALVA V RCBC BankDocument1 pageVILLALVA V RCBC BankNino Kim AyubanNo ratings yet

- Reserve Bank of Fiji exchange control loan repayment applicationDocument3 pagesReserve Bank of Fiji exchange control loan repayment applicationroybendengNo ratings yet

- 1 The Nature, Purpose and Scope of AuditingDocument12 pages1 The Nature, Purpose and Scope of Auditingyebegashet100% (1)

- Day 1 (Sole Trader Final Account)Document7 pagesDay 1 (Sole Trader Final Account)Han Thi Win KoNo ratings yet

- Cash Flow Statement 2019 HL Question Worked SolutionDocument5 pagesCash Flow Statement 2019 HL Question Worked SolutionConor MurphyNo ratings yet

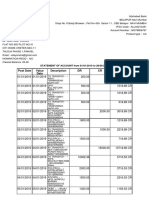

- TransNum Jun 28 100629Document24 pagesTransNum Jun 28 100629Udayraj VarmaNo ratings yet

- Chapter 4 - Concept Questions and ExercisesDocument5 pagesChapter 4 - Concept Questions and ExercisesTranh Meow MeowNo ratings yet

- Indian Post Office - Redefining DistributionDocument10 pagesIndian Post Office - Redefining DistributionBushalNo ratings yet

- Final Accounts: Formats Business Name Statement of Financial Position As On - Assets: Non-Current AssetsDocument35 pagesFinal Accounts: Formats Business Name Statement of Financial Position As On - Assets: Non-Current AssetsHammad KhalidNo ratings yet

- Internship Report of Nepal Bank Limited OveralllDocument7 pagesInternship Report of Nepal Bank Limited OverallldingautamNo ratings yet

- Natwarlal & CompanyDocument17 pagesNatwarlal & Companysunil jadhavNo ratings yet

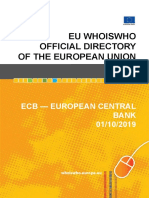

- Eu Whoiswho Official Directory of The European Union: Ecb - European Central Bank 01/10/2019Document11 pagesEu Whoiswho Official Directory of The European Union: Ecb - European Central Bank 01/10/2019stefi4kaNo ratings yet

- Fast Path NavigationsDocument8 pagesFast Path Navigationsakshay sasidhar100% (1)

- Fino Payments Bank Limted RHPDocument338 pagesFino Payments Bank Limted RHPkesavan91No ratings yet

- CLD - BAO3404 TUTORIAL GUIDE WordDocument49 pagesCLD - BAO3404 TUTORIAL GUIDE WordShi MingNo ratings yet

- B124 - 19J - TMA 01 - Guidance NotesDocument13 pagesB124 - 19J - TMA 01 - Guidance NotesFlavio Leal JovchelevitchNo ratings yet

- Form 12BBDocument3 pagesForm 12BBAnonymous Gg6z0u9IBzNo ratings yet

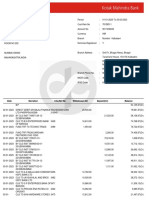

- RDInstallment Report 01!06!2023Document1 pageRDInstallment Report 01!06!2023PRADEEP KUMARNo ratings yet

- RETIREMENT WORK SHEET SOLUTIONS FOR ACCOUNTANCY GRADE 12Document5 pagesRETIREMENT WORK SHEET SOLUTIONS FOR ACCOUNTANCY GRADE 12priya longaniNo ratings yet

- 431 FinalDocument6 pages431 FinalfNo ratings yet

- Compound Interest Calculator: 30 ExercisesDocument4 pagesCompound Interest Calculator: 30 ExercisesDilina De SilvaNo ratings yet

- GFS 2001 Manual-Basic ConceptsDocument40 pagesGFS 2001 Manual-Basic ConceptsProfessor Tarun DasNo ratings yet

- Accounting For Notes ReceivablesDocument4 pagesAccounting For Notes ReceivablesYeon TanNo ratings yet

- Bank ReconciliationDocument12 pagesBank ReconciliationJieniel ShanielNo ratings yet

- Tanny Cabrera Company Cash BudgetDocument5 pagesTanny Cabrera Company Cash BudgetLysss EpssssNo ratings yet

- Jinkie Filecima M. Roa-AGENCY-Diversify-09082019125734 PDFDocument7 pagesJinkie Filecima M. Roa-AGENCY-Diversify-09082019125734 PDFKarl LandritoNo ratings yet

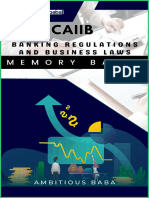

- Memory BasedDocument12 pagesMemory BasedHari RajNo ratings yet

- Books of AccountsDocument13 pagesBooks of AccountsKeith Elisa OlivaNo ratings yet

- 2.1 Mandate For Limited CompanyDocument2 pages2.1 Mandate For Limited CompanyangkalabawNo ratings yet

- Shifting BranchDocument39 pagesShifting Branchaniket_kulal29No ratings yet