You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Geography Cba PowerpointDocument10 pagesGeography Cba Powerpointapi-489088076No ratings yet

- Internet Intranet ExtranetDocument28 pagesInternet Intranet ExtranetAmeya Patil100% (1)

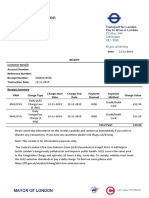

- Transport For London Pay To Drive in London: PO Box 344 Darlington Dl1 9qe TFL - Gov.uk/drivingDocument1 pageTransport For London Pay To Drive in London: PO Box 344 Darlington Dl1 9qe TFL - Gov.uk/drivingDanyy MaciucNo ratings yet

- Case Study ToshibaDocument6 pagesCase Study ToshibaRachelle100% (1)

- Jannal Malar Sujatha Original PDFDocument164 pagesJannal Malar Sujatha Original PDFRajagopalanNo ratings yet

- Guide To Enhance Your Accounting Software To Be GST Compliant (200716)Document96 pagesGuide To Enhance Your Accounting Software To Be GST Compliant (200716)RajagopalanNo ratings yet

- Notes 1Document48 pagesNotes 1Kalyan BoraNo ratings yet

- Guide To Enhance Your Accounting Software To Be GST Compliant (200716)Document96 pagesGuide To Enhance Your Accounting Software To Be GST Compliant (200716)RajagopalanNo ratings yet

- Persuasion 101Document19 pagesPersuasion 101gnmantel0% (1)

- 8 e Daft Chapter 01Document29 pages8 e Daft Chapter 01GabNo ratings yet

- Mcqs Ethics and CSR)Document9 pagesMcqs Ethics and CSR)Maida TanweerNo ratings yet

- Dell Online - Case AnalysisDocument5 pagesDell Online - Case AnalysisMohit Agarwal0% (1)

- BIR Form 2307Document20 pagesBIR Form 2307Lean Isidro0% (1)

- Unit I Lesson Ii Roles of A TeacherDocument7 pagesUnit I Lesson Ii Roles of A TeacherEvergreens SalongaNo ratings yet

- 2010 LeftySpeed Oms en 0Document29 pages2010 LeftySpeed Oms en 0Discord ShadowNo ratings yet

- Risk Management GuidanceDocument9 pagesRisk Management GuidanceHelen GouseNo ratings yet

- Windows XP, Vista, 7, 8, 10 MSDN Download (Untouched)Document5 pagesWindows XP, Vista, 7, 8, 10 MSDN Download (Untouched)Sheen QuintoNo ratings yet

- For Visual Studio User'S Manual: Motoplus SDKDocument85 pagesFor Visual Studio User'S Manual: Motoplus SDKMihail AvramovNo ratings yet

- WFP Situation Report On Fire in The Rohingya Refugee Camp (23.03.2021)Document2 pagesWFP Situation Report On Fire in The Rohingya Refugee Camp (23.03.2021)Wahyu RamdhanNo ratings yet

- Disaster Management in Schools: Status ReportDocument28 pagesDisaster Management in Schools: Status ReportRamalingam VaradarajuluNo ratings yet

- 5d814c4d6437b300fd0e227a - Scorch Product Sheet 512GB PDFDocument1 page5d814c4d6437b300fd0e227a - Scorch Product Sheet 512GB PDFBobby B. BrownNo ratings yet

- Notes in Train Law PDFDocument11 pagesNotes in Train Law PDFJanica Lobas100% (1)

- BMR - Lab ManualDocument23 pagesBMR - Lab ManualMohana PrasathNo ratings yet

- Microeconomics Theory and Applications 12th Edition Browning Solutions ManualDocument5 pagesMicroeconomics Theory and Applications 12th Edition Browning Solutions Manualhauesperanzad0ybz100% (26)

- Assignment No. 1: Semester Fall 2021 Data Warehousing - CS614Document3 pagesAssignment No. 1: Semester Fall 2021 Data Warehousing - CS614Hamza Khan AbduhuNo ratings yet

- Chap 4 Safety Managment SystemDocument46 pagesChap 4 Safety Managment SystemABU BEBEK AhmNo ratings yet

- Cable 3/4 Sleeve Sweater: by Lisa RichardsonDocument3 pagesCable 3/4 Sleeve Sweater: by Lisa RichardsonAlejandra Martínez MartínezNo ratings yet

- Thesis-Android-Based Health-Care Management System: July 2016Document66 pagesThesis-Android-Based Health-Care Management System: July 2016Noor Md GolamNo ratings yet

- Gr7 3rd PeriodicalDocument2 pagesGr7 3rd PeriodicalElle GonzagaNo ratings yet

- 20091216-153551-APC Smart-UPS 1500VA USB SUA1500IDocument4 pages20091216-153551-APC Smart-UPS 1500VA USB SUA1500Ifietola1No ratings yet

- BA5411 ProjectGuidelines - 2020 PDFDocument46 pagesBA5411 ProjectGuidelines - 2020 PDFMonisha ReddyNo ratings yet

- Which Among The Following Statement Is INCORRECTDocument7 pagesWhich Among The Following Statement Is INCORRECTJyoti SinghNo ratings yet

- Unix Training ContentDocument5 pagesUnix Training ContentsathishkumarNo ratings yet

- Annex B Brochure Vector and ScorpionDocument4 pagesAnnex B Brochure Vector and ScorpionomarhanandehNo ratings yet