You might also like

- Restrictions on franking creditsDocument1 pageRestrictions on franking creditsoddsey0713No ratings yet

- 2-3 Capital AllowancesDocument1 page2-3 Capital Allowancesoddsey0713No ratings yet

- 1-8 GST - GST Payable or ITC AvalDocument2 pages1-8 GST - GST Payable or ITC Avaloddsey0713No ratings yet

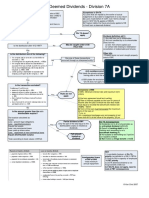

- 3-3 Div 7A Deemed Divs - VLDocument1 page3-3 Div 7A Deemed Divs - VLoddsey0713No ratings yet

- 4-3 Part IVA General AntiAvoidanceDocument1 page4-3 Part IVA General AntiAvoidanceoddsey0713No ratings yet

- ADJUSTMENTS AT FINANCIAL PERIOD ENDDocument18 pagesADJUSTMENTS AT FINANCIAL PERIOD ENDTevabless Suoived SpotlightbabeNo ratings yet

- Module 2Document12 pagesModule 2zoyaNo ratings yet

- TAX ADMINISTRATION GUIDEDocument4 pagesTAX ADMINISTRATION GUIDEwumel01No ratings yet

- GST On Property Transactions - 99 Page Research ReportDocument99 pagesGST On Property Transactions - 99 Page Research ReporttestnationNo ratings yet

- Capital Budgeting Decision - SBSDocument43 pagesCapital Budgeting Decision - SBSSahil SherasiyaNo ratings yet

- Tax Book 2016-17 - Version 1.0a USB PDFDocument372 pagesTax Book 2016-17 - Version 1.0a USB PDFemc2_mcv100% (1)

- Understanding Income TaxDocument43 pagesUnderstanding Income TaxMerediths KrisKringleNo ratings yet

- Income Taxes (IAS 12)Document15 pagesIncome Taxes (IAS 12)Mahir RahmanNo ratings yet

- Code of Ethics Part C Professional Accountants in Business 1 Jan 2011Document11 pagesCode of Ethics Part C Professional Accountants in Business 1 Jan 2011James De Torres CarilloNo ratings yet

- Smieliauskas 6e - Solutions Manual - Chapter 02Document14 pagesSmieliauskas 6e - Solutions Manual - Chapter 02scribdteaNo ratings yet

- Balance Sheet: For Year Ending June 30, 2008Document3 pagesBalance Sheet: For Year Ending June 30, 2008arazeqNo ratings yet

- CMA Handbook: Your Guide To Information and Requirements For CMA CertificationDocument13 pagesCMA Handbook: Your Guide To Information and Requirements For CMA CertificationBupe ChaliNo ratings yet

- CPA TestDocument22 pagesCPA Testdani13_335942No ratings yet

- TABL2751 2016-2 Tutorial Program FinalDocument25 pagesTABL2751 2016-2 Tutorial Program FinalAnna ChenNo ratings yet

- LifeInsRetirementValuation M15 AppraisalValues 181205Document46 pagesLifeInsRetirementValuation M15 AppraisalValues 181205Jeff JonesNo ratings yet

- VIVA Answers (Mock-2)Document12 pagesVIVA Answers (Mock-2)isuri abeykoon100% (1)

- When To Hire A Tax ProfessionalDocument7 pagesWhen To Hire A Tax ProfessionalMaimai Durano100% (1)

- SwotDocument3 pagesSwotShahebazNo ratings yet

- Start Your BusinessDocument8 pagesStart Your BusinessIqbal MOUSSANo ratings yet

- Cma Final Law Hand Written Notes - 1608742860Document2 pagesCma Final Law Hand Written Notes - 1608742860Dharshini AravamudhanNo ratings yet

- Ipcc Tax Practice Manual PDFDocument651 pagesIpcc Tax Practice Manual PDFshakshi gupta100% (1)

- Accounting Dissertations - IfRSDocument30 pagesAccounting Dissertations - IfRSgappu002No ratings yet

- Benifit Pension ObligationDocument20 pagesBenifit Pension ObligationTouseefNo ratings yet

- Assignment 2: Tracy Van Rensburg STUDENT NUMBER 59548525Document8 pagesAssignment 2: Tracy Van Rensburg STUDENT NUMBER 59548525Chris NdlovuNo ratings yet

- Taxation (Bs211)Document348 pagesTaxation (Bs211)RewardMaturureNo ratings yet

- 51 List of CA Final Law SectionsDocument35 pages51 List of CA Final Law SectionsAishwarya TiwariNo ratings yet

- 401K PlannerDocument3 pages401K Plannertf2025No ratings yet

- Fin701 Module3Document22 pagesFin701 Module3Krista CataldoNo ratings yet

- AUD Notes Chapter 2Document20 pagesAUD Notes Chapter 2janell184100% (1)

- SMA QuizDocument76 pagesSMA QuizQuỳnh ChâuNo ratings yet

- MBA104 - Almario - Parco - Chapter 1 Part 2 Individual Assignment Online Presentation 3Document25 pagesMBA104 - Almario - Parco - Chapter 1 Part 2 Individual Assignment Online Presentation 3Jesse Rielle CarasNo ratings yet

- Audit Practices ManualDocument354 pagesAudit Practices ManualRaif QelaNo ratings yet

- Section A: Multiple Choice Questions - Single Option: This Section Has 70 Questions Worth 1 Mark Each (Total of 70 Marks)Document24 pagesSection A: Multiple Choice Questions - Single Option: This Section Has 70 Questions Worth 1 Mark Each (Total of 70 Marks)Kenny HoNo ratings yet

- SBR Study Support Guide: Plan Prepare PassDocument27 pagesSBR Study Support Guide: Plan Prepare PassNitesh RawatNo ratings yet

- F7 Technical ArticlesDocument121 pagesF7 Technical ArticlesNicquain0% (1)

- BEC Study Guide 4-19-2013Document220 pagesBEC Study Guide 4-19-2013Valerie Readhimer100% (1)

- Exp Fia-Ffm NotesDocument51 pagesExp Fia-Ffm Notesati19100% (1)

- Additional Deferred Tax Examples.2Document3 pagesAdditional Deferred Tax Examples.2milton1986100% (1)

- Aud NotesDocument75 pagesAud NotesClaire O'BrienNo ratings yet

- Auditors' responsibilities and ethicsDocument12 pagesAuditors' responsibilities and ethicsscribdtea100% (1)

- Part 3 - Understanding Financial Statements and ReportsDocument7 pagesPart 3 - Understanding Financial Statements and ReportsJeanrey AlcantaraNo ratings yet

- Acca SBR 691 698 PDFDocument8 pagesAcca SBR 691 698 PDFYudheesh P 1822082No ratings yet

- MBA104 - Almario - Parco - Chapter 1 Part 2 Individual Assignment Online Presentation 1Document23 pagesMBA104 - Almario - Parco - Chapter 1 Part 2 Individual Assignment Online Presentation 1Jesse Rielle CarasNo ratings yet

- US CMA MCQ QuestionsDocument5 pagesUS CMA MCQ QuestionsSachin Kandloor0% (1)

- What Is The Indirect MethodDocument3 pagesWhat Is The Indirect MethodHsin Wua ChiNo ratings yet

- William WongDocument3 pagesWilliam WongKashif Mehmood0% (1)

- Lsbf-Mock Answer f8Document15 pagesLsbf-Mock Answer f8emmadavisonsNo ratings yet

- 04 Working Capital Management and Corporate GovernanceDocument26 pages04 Working Capital Management and Corporate GovernanceKrutika NandanNo ratings yet

- Income TaxDocument109 pagesIncome TaxDaksh KohliNo ratings yet

- Cma TemplateDocument25 pagesCma TemplateSavoir PenNo ratings yet

- CFA Investment Foundations - Module 1 (CFA Institute) (Z-Library)Document39 pagesCFA Investment Foundations - Module 1 (CFA Institute) (Z-Library)gmofneweraNo ratings yet

- Fringe Benefit Tax (FBT)Document35 pagesFringe Benefit Tax (FBT)SanjayNo ratings yet

- ACCT604 Week 7 Lecture SlidesDocument29 pagesACCT604 Week 7 Lecture SlidesBuddika PrasannaNo ratings yet

- CIR v. SOJ & PAGCOR: Final Withholding Tax on Fringe BenefitsDocument4 pagesCIR v. SOJ & PAGCOR: Final Withholding Tax on Fringe BenefitsIan Villafuerte100% (1)

- 1-4 Deductions FlowchartDocument2 pages1-4 Deductions Flowchartoddsey0713No ratings yet

- 3-3 Company LossesDocument1 page3-3 Company Lossesoddsey0713No ratings yet

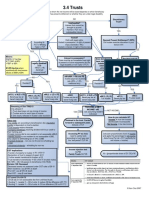

- 3-4 TrustsDocument1 page3-4 Trustsoddsey0713No ratings yet

- 1-3 Assessable IncomeDocument2 pages1-3 Assessable Incomeoddsey0713No ratings yet

- 3 5 PartnershipsDocument1 page3 5 Partnershipsoddsey0713No ratings yet

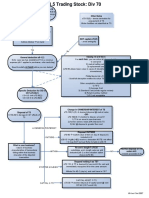

- 1-5 Trading StockDocument1 page1-5 Trading Stockoddsey0713No ratings yet

- 2-4,5 Capital WorksDocument1 page2-4,5 Capital Worksoddsey0713No ratings yet

- Creating Effective Ads PPT 4 MGMTDocument22 pagesCreating Effective Ads PPT 4 MGMToddsey0713No ratings yet

- Executing-The-Creative Design Elements and Layout Styles With ADS As ExamplesDocument47 pagesExecuting-The-Creative Design Elements and Layout Styles With ADS As Examplesoddsey0713No ratings yet

- T5 Chapters 4 and 8 Solutions To The Essential ActivitiesDocument18 pagesT5 Chapters 4 and 8 Solutions To The Essential Activitiesoddsey0713No ratings yet

- Case Summaries 1 193Document54 pagesCase Summaries 1 193oddsey0713100% (1)

- T7 Chapter 6 Solutions To The Essential ActivitiesDocument26 pagesT7 Chapter 6 Solutions To The Essential Activitiesoddsey0713No ratings yet

- T6 Chapter 5 Solutions To The Essential ActivitiesDocument12 pagesT6 Chapter 5 Solutions To The Essential Activitiesoddsey0713No ratings yet

- T8 Chapters 9 and 7 Solutions To The Essential ActivitiesDocument12 pagesT8 Chapters 9 and 7 Solutions To The Essential Activitiesoddsey0713No ratings yet

- 2006 Planning EvalDocument33 pages2006 Planning EvalSanjay SahooNo ratings yet

- Summer Training Report On Talent AcquisitionDocument56 pagesSummer Training Report On Talent AcquisitionFun2ushhNo ratings yet

- Axial DCF Business Valuation Calculator GuideDocument4 pagesAxial DCF Business Valuation Calculator GuideUdit AgrawalNo ratings yet

- Form A2: AnnexDocument8 pagesForm A2: Annexi dint knowNo ratings yet

- Order in The Matter of Pancard Clubs LimitedDocument84 pagesOrder in The Matter of Pancard Clubs LimitedShyam SunderNo ratings yet

- Beyond Vertical Integration The Rise of The Value-Adding PartnershipDocument17 pagesBeyond Vertical Integration The Rise of The Value-Adding Partnershipsumeet_goelNo ratings yet

- MoneyDocument2 pagesMoney09-Nguyễn Hữu Phú BìnhNo ratings yet

- 2022 Logistics 05 Chap 08 PlanningRes CapaMgmt Part 1Document37 pages2022 Logistics 05 Chap 08 PlanningRes CapaMgmt Part 1Chíi KiệttNo ratings yet

- Introduction and Company Profile: Retail in IndiaDocument60 pagesIntroduction and Company Profile: Retail in IndiaAbhinav Bansal0% (1)

- Assignment 1: NPV and IRR, Mutually Exclusive Projects: Net Present Value 1,930,110.40 2,251,795.46Document3 pagesAssignment 1: NPV and IRR, Mutually Exclusive Projects: Net Present Value 1,930,110.40 2,251,795.46Giselle MartinezNo ratings yet

- Working Capital Management of Nepal TelecomDocument135 pagesWorking Capital Management of Nepal TelecomGehendraSubedi70% (10)

- Accounting for Legal FirmsDocument23 pagesAccounting for Legal FirmsARVIN RAJNo ratings yet

- Market SegmentationDocument21 pagesMarket SegmentationMian Mujeeb RehmanNo ratings yet

- 20 Accounting Changes and Error CorrectionsDocument17 pages20 Accounting Changes and Error CorrectionsKyll MarcosNo ratings yet

- Fire in A Bangladesh Garment FactoryDocument6 pagesFire in A Bangladesh Garment FactoryRaquelNo ratings yet

- Regulatory Framework For Hospitality Industry in Nigeria 3Document35 pagesRegulatory Framework For Hospitality Industry in Nigeria 3munzali67% (3)

- Download ebook Economics For Business Pdf full chapter pdfDocument60 pagesDownload ebook Economics For Business Pdf full chapter pdfcurtis.williams851100% (21)

- Weeks 3 & 4Document46 pagesWeeks 3 & 4NursultanNo ratings yet

- Niti Aayog PDFDocument4 pagesNiti Aayog PDFUppamjot Singh100% (1)

- Managing Organizational Change at Campbell and Bailyn's Boston OfficeDocument12 pagesManaging Organizational Change at Campbell and Bailyn's Boston OfficeBorne KillereNo ratings yet

- Executive Master in Health AdministrationDocument3 pagesExecutive Master in Health Administrationapi-87967494No ratings yet

- Fundamentals of AccountingDocument56 pagesFundamentals of AccountingFiza IrfanNo ratings yet

- Traders CodeDocument7 pagesTraders CodeHarshal Kumar ShahNo ratings yet

- Clutch Auto PDFDocument52 pagesClutch Auto PDFHarshvardhan KothariNo ratings yet

- Oswal Woolen MillsDocument76 pagesOswal Woolen MillsMohit kolliNo ratings yet

- 22 Immutable Laws of Marketing SummaryDocument2 pages22 Immutable Laws of Marketing SummaryWahid T. YahyahNo ratings yet

- Using APV: Advantages Over WACCDocument2 pagesUsing APV: Advantages Over WACCMortal_AqNo ratings yet

- Department of Labor: DekalbDocument58 pagesDepartment of Labor: DekalbUSA_DepartmentOfLabor50% (2)

- Jio Fiber Tax Invoice TemplateDocument5 pagesJio Fiber Tax Invoice TemplatehhhhNo ratings yet

- How Businesses Have Adapted Their Corporate Social Responsibility Amidst the PandemicDocument7 pagesHow Businesses Have Adapted Their Corporate Social Responsibility Amidst the PandemicJapsay Francisco GranadaNo ratings yet

- Difference Between Delegation and DecentralizationDocument4 pagesDifference Between Delegation and Decentralizationjatinder99No ratings yet