You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5782)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Seph Lawless Foreclosure - Joseph MelendezDocument44 pagesSeph Lawless Foreclosure - Joseph Melendezseph lawlessNo ratings yet

- Liquidity Adjustment FacilityDocument1 pageLiquidity Adjustment FacilityPrernaSharma100% (1)

- Indian Accounting Standards OverviewDocument12 pagesIndian Accounting Standards OverviewREHANRAJNo ratings yet

- Straumann enDocument26 pagesStraumann enyeochunhongNo ratings yet

- Business Finance-Q3-Week-1-2Document5 pagesBusiness Finance-Q3-Week-1-2Axerob BmNo ratings yet

- Detailed Solutions To Problem 5Document3 pagesDetailed Solutions To Problem 5Maria AngelicaNo ratings yet

- Literature ReviewDocument5 pagesLiterature ReviewGourab MondalNo ratings yet

- TXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceDocument4 pagesTXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceJaseem MonuNo ratings yet

- Credit Ratings Provide Insight Into Financial StrengthDocument6 pagesCredit Ratings Provide Insight Into Financial StrengthvishNo ratings yet

- Anderton SICAV Launches New High Income Investment Fund. Gamma Capital Markets Acts As Investment Manager.Document5 pagesAnderton SICAV Launches New High Income Investment Fund. Gamma Capital Markets Acts As Investment Manager.PR.comNo ratings yet

- SHF Order FormDocument2 pagesSHF Order FormFernando PlansNo ratings yet

- Cryptocurrency Comparison QuestionsDocument8 pagesCryptocurrency Comparison Questionshaze blazeNo ratings yet

- METROPOLITAN BANK AND TRUST COMPANY vs. MARINA B. CUSTODIODocument2 pagesMETROPOLITAN BANK AND TRUST COMPANY vs. MARINA B. CUSTODIOKayee KatNo ratings yet

- UntitledDocument5 pagesUntitledKristine dela CruzNo ratings yet

- Tax Invoice: Billing Address Installation Address Invoice DetailsDocument1 pageTax Invoice: Billing Address Installation Address Invoice DetailsKuladeep Naidu PatibandlaNo ratings yet

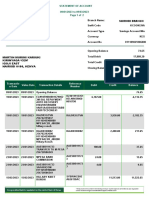

- Martin Murimi KariukiDocument2 pagesMartin Murimi KariukiKameneja LeeNo ratings yet

- DSCR Tutorial: Understanding the Debt Service Coverage RatioDocument2 pagesDSCR Tutorial: Understanding the Debt Service Coverage RatioArun Pasi100% (1)

- Statements 7344Document4 pagesStatements 7344Валентина ШвечиковаNo ratings yet

- Compound Interest Problems With Detailed SolutionsDocument11 pagesCompound Interest Problems With Detailed SolutionsJerle Mae ParondoNo ratings yet

- HW2 ch12bDocument10 pagesHW2 ch12bBAurNo ratings yet

- Financial Ratios OsborneDocument27 pagesFinancial Ratios Osbornemitsonu100% (1)

- Cash For SeatworkDocument3 pagesCash For SeatworkMika MolinaNo ratings yet

- Petroflo Trading Company: Cash Payment VoucherDocument10 pagesPetroflo Trading Company: Cash Payment Vouchermuhammad ihtishamNo ratings yet

- UntitledDocument65 pagesUntitledmario.mariniNo ratings yet

- Targeting Presentation Nov' 07Document15 pagesTargeting Presentation Nov' 07Shashank SahuNo ratings yet

- ITC Group Company ProfileDocument19 pagesITC Group Company ProfileNeel ThobhaniNo ratings yet

- Sem Plang Merchandising Periodic Problem With AnswersDocument21 pagesSem Plang Merchandising Periodic Problem With Answerscole sprouse100% (1)

- Equity Trading and Demat Account Opening FormDocument19 pagesEquity Trading and Demat Account Opening FormJAYSURYA YASHVANT100% (1)

- MATERIALDocument23 pagesMATERIALPocari OnceNo ratings yet

- Zimsec - Nov - 2016 - Ms 3Document9 pagesZimsec - Nov - 2016 - Ms 3Wesley KisiNo ratings yet