You might also like

- Solutions Manual To Accompany FAPF - Ch14Document11 pagesSolutions Manual To Accompany FAPF - Ch14nasNo ratings yet

- Human Resource ManagementDocument69 pagesHuman Resource ManagementnasNo ratings yet

- MCQin Marginal CostingDocument5 pagesMCQin Marginal CostingnasNo ratings yet

- SwapsDocument41 pagesSwapsAnonymous 7Un6mnqJzNNo ratings yet

- SensiDocument6 pagesSensinasNo ratings yet

- Chapter 5 Non Integrated AccountsDocument52 pagesChapter 5 Non Integrated AccountsmahendrabpatelNo ratings yet

- Financial Statement Analysis: The Raw Data for InvestingDocument18 pagesFinancial Statement Analysis: The Raw Data for Investingshamapant7955100% (2)

- Financial DerivativesDocument108 pagesFinancial Derivativesramesh158No ratings yet

- Income Tax Reform IndiaDocument17 pagesIncome Tax Reform IndiaGagan SinghNo ratings yet

- Swap PDFDocument23 pagesSwap PDFshivam_dubey4004No ratings yet

- Lecture 1Document10 pagesLecture 1nasNo ratings yet

- 20077ipcc Paper7B Vol1 Cp3Document27 pages20077ipcc Paper7B Vol1 Cp3nasNo ratings yet

- Assumption of NormalityDocument27 pagesAssumption of NormalitynasNo ratings yet

- Fast Food Survey Results for Franklin Pierce CollegeDocument24 pagesFast Food Survey Results for Franklin Pierce CollegenasNo ratings yet

- Study Note - 23: Penalty & ProsecutionDocument1 pageStudy Note - 23: Penalty & ProsecutionnasNo ratings yet

- 20Document19 pages20Rashmi SinghNo ratings yet

- Bop BoliviaDocument2 pagesBop BolivianasNo ratings yet

- E Waste1Document66 pagesE Waste1nasNo ratings yet

- WEA Intro To Weather DerDocument10 pagesWEA Intro To Weather DerJugal DesaiNo ratings yet

- 06logisticregression 150930040919 Lva1 App6891Document44 pages06logisticregression 150930040919 Lva1 App6891nasNo ratings yet

- Fixed Income Buy Side, Research & Sell Side Careers: A GuideDocument13 pagesFixed Income Buy Side, Research & Sell Side Careers: A GuidenasNo ratings yet

- Discriminant Analyses SPSS - Predict Grad SuccessDocument3 pagesDiscriminant Analyses SPSS - Predict Grad SuccessBodnaras AdrianNo ratings yet

- Assumption of NormalityDocument27 pagesAssumption of NormalitynasNo ratings yet

- WEA Intro To Weather DerDocument10 pagesWEA Intro To Weather DerJugal DesaiNo ratings yet

- Security and Security Market OperationsDocument303 pagesSecurity and Security Market OperationsAdeem AshrafiNo ratings yet

- Discuss The Various Stages of Project FormulationDocument2 pagesDiscuss The Various Stages of Project Formulationrock52land76% (25)

- Project TopicsDocument21 pagesProject TopicsnasNo ratings yet

- Commercial PapersDocument13 pagesCommercial PapersnasNo ratings yet

- MCQin Marginal CostingDocument5 pagesMCQin Marginal CostingnasNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5784)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Apoptosis Poster March 20106547Document1 pageApoptosis Poster March 20106547Achmad JunaidiNo ratings yet

- Overview and Features of GST: D.P. Nagendra Kumar Director General, GST Intelligence (South)Document8 pagesOverview and Features of GST: D.P. Nagendra Kumar Director General, GST Intelligence (South)ALL YOU NEEDNo ratings yet

- CCI Restricts Auto Manufacturers' Aftermarket PracticesDocument11 pagesCCI Restricts Auto Manufacturers' Aftermarket PracticesDisha PathakNo ratings yet

- EGESIF - 14-0011 - Guidance On Audit StrategyDocument23 pagesEGESIF - 14-0011 - Guidance On Audit StrategymedsNo ratings yet

- Intergrity Management Guide (Final)Document70 pagesIntergrity Management Guide (Final)mthr25467502No ratings yet

- Principles and Practice of General Insurance ICAIDocument333 pagesPrinciples and Practice of General Insurance ICAIBilawal MNo ratings yet

- PCFI v. National Telecommunications Commission G.R. No. L-63318 August 18, 1984Document9 pagesPCFI v. National Telecommunications Commission G.R. No. L-63318 August 18, 1984jake31No ratings yet

- Code of ConductDocument5 pagesCode of ConductAyaz MeerNo ratings yet

- Report To California Gambling Control Commission Regarding Lake Elsinore Casino.Document21 pagesReport To California Gambling Control Commission Regarding Lake Elsinore Casino.The Press-Enterprise / pressenterprise.comNo ratings yet

- Eric Sunada Letter To Planning Commission On Zoning of Lowe's ProjectDocument9 pagesEric Sunada Letter To Planning Commission On Zoning of Lowe's ProjectAnonymous 56qRCzJRNo ratings yet

- Wpi - Waterfront Philippines Inc - Sec Form Definitive Information Statement - 20october2020Document353 pagesWpi - Waterfront Philippines Inc - Sec Form Definitive Information Statement - 20october2020dawijawof awofnafawNo ratings yet

- Control of Radioactive Substances: HSE Information SheetDocument4 pagesControl of Radioactive Substances: HSE Information Sheetsamer alrawashdehNo ratings yet

- Ally Trust Deposits ApplicationDocument5 pagesAlly Trust Deposits ApplicationARTHUR MILLERNo ratings yet

- Corporate Governance and Value Creation - Private Equity StyleDocument9 pagesCorporate Governance and Value Creation - Private Equity StylemokitiNo ratings yet

- Act 386 Irrigation Areas Act 1953Document20 pagesAct 386 Irrigation Areas Act 1953Adam Haida & CoNo ratings yet

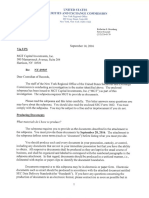

- SEC Subpoena MGT Capital September 2016Document14 pagesSEC Subpoena MGT Capital September 2016Teri Buhl100% (1)

- Notice: Commission Decision To Review, Etc.: Certain Endoscopic Probes For Use in Argon Plasma Coagulation SystemsDocument1 pageNotice: Commission Decision To Review, Etc.: Certain Endoscopic Probes For Use in Argon Plasma Coagulation SystemsJustia.comNo ratings yet

- Felix Capability OverviewDocument12 pagesFelix Capability OverviewGagan GahlotNo ratings yet

- The Financial Intelligence Centre Act No. 38 of 2001 - A Guideline For Legal Practitioners and Legal PracticesDocument12 pagesThe Financial Intelligence Centre Act No. 38 of 2001 - A Guideline For Legal Practitioners and Legal Practicesjenna.amber000No ratings yet

- Bangladesh University of Professionals: Mirpur Cantonment, DhakaDocument3 pagesBangladesh University of Professionals: Mirpur Cantonment, DhakaSinhaj NoorNo ratings yet

- PDF DownloadDocument20 pagesPDF DownloadMD AZHARNo ratings yet

- 118 Pre-Qualification For Supply and Delivery of Fresh Fruits and VegetablesDocument33 pages118 Pre-Qualification For Supply and Delivery of Fresh Fruits and Vegetablesapi-257725116No ratings yet

- OBLICON ReviewerDocument150 pagesOBLICON ReviewerblimjucoNo ratings yet

- General Guidelines On Leave ApplicationsDocument2 pagesGeneral Guidelines On Leave ApplicationsJanking Madriaga I100% (7)

- Requirements For Registering Your BusinessDocument30 pagesRequirements For Registering Your BusinessHarry100% (1)

- Register with AMFIDocument3 pagesRegister with AMFIDeepak Iyer Deepu0% (1)

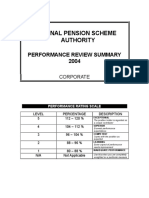

- National Pension Scheme Authority: Performance Review Summary 2004Document7 pagesNational Pension Scheme Authority: Performance Review Summary 2004peter mulilaNo ratings yet

- Code of Ethis and Ethical Standars of OfficersDocument8 pagesCode of Ethis and Ethical Standars of OfficersShiryll Bantayan RupaNo ratings yet

- Bharat Diamond Bourse Membership EligibilityDocument12 pagesBharat Diamond Bourse Membership EligibilitytusharNo ratings yet

- COSHH: Control of Substances Hazardous To HealthDocument4 pagesCOSHH: Control of Substances Hazardous To HealthmahyarbNo ratings yet