You might also like

- Newtech Advant Business Plan9 PDFDocument38 pagesNewtech Advant Business Plan9 PDFdanookyereNo ratings yet

- Basic Financial Econometrics PDFDocument167 pagesBasic Financial Econometrics PDFdanookyereNo ratings yet

- MKTG Res CUSTOMER DELIGHT IN HOSPITALITY INDUSTRYDocument51 pagesMKTG Res CUSTOMER DELIGHT IN HOSPITALITY INDUSTRYdanookyereNo ratings yet

- Theories in Marketing StrategyDocument4 pagesTheories in Marketing StrategydanookyereNo ratings yet

- Daniel's Draft PresentationDocument21 pagesDaniel's Draft PresentationdanookyereNo ratings yet

- Inventory ControlDocument9 pagesInventory ControldanookyereNo ratings yet

- Customer Satisfaction Theories PDFDocument34 pagesCustomer Satisfaction Theories PDFdanookyereNo ratings yet

- CFE-CMStatistics 2017 Conference AbstractsDocument272 pagesCFE-CMStatistics 2017 Conference AbstractsdanookyereNo ratings yet

- Models and Theories of Customer SatisfactionDocument31 pagesModels and Theories of Customer SatisfactiondanookyereNo ratings yet

- Customer Satisfaction Theories PDFDocument34 pagesCustomer Satisfaction Theories PDFdanookyereNo ratings yet

- Joshua 1:9: Bible Quotations For The Bible Reading MarathonDocument5 pagesJoshua 1:9: Bible Quotations For The Bible Reading MarathondanookyereNo ratings yet

- Customer Satisfaction Theories PDFDocument34 pagesCustomer Satisfaction Theories PDFdanookyereNo ratings yet

- The Role of Communication in Marketing StrategiesDocument4 pagesThe Role of Communication in Marketing StrategiesdanookyereNo ratings yet

- Impact of Price Changes on Buying DecisionsDocument2 pagesImpact of Price Changes on Buying DecisionsdanookyereNo ratings yet

- Accounting For Cash FlowDocument2 pagesAccounting For Cash FlowdanookyereNo ratings yet

- The Role of Communication in Marketing StrategiesDocument4 pagesThe Role of Communication in Marketing StrategiesdanookyereNo ratings yet

- Accounting For DepreciationDocument28 pagesAccounting For DepreciationdanookyereNo ratings yet

- The Role of Communication in Marketing StrategiesDocument4 pagesThe Role of Communication in Marketing StrategiesdanookyereNo ratings yet

- 2011 M ClassDocument22 pages2011 M ClassdanookyereNo ratings yet

- Impact of Price Changes on Buying DecisionsDocument2 pagesImpact of Price Changes on Buying DecisionsdanookyereNo ratings yet

- Importance of A Trial BalanceDocument1 pageImportance of A Trial Balancedanookyere100% (3)

- The Role of Communication in Marketing StrategiesDocument4 pagesThe Role of Communication in Marketing StrategiesdanookyereNo ratings yet

- Importance of A Trial BalanceDocument1 pageImportance of A Trial Balancedanookyere100% (3)

- Parenting) 10 Tips To Healthy Eating and Physical Activity For KidsDocument5 pagesParenting) 10 Tips To Healthy Eating and Physical Activity For KidssteriandediuNo ratings yet

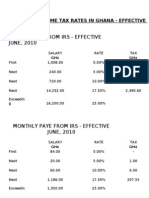

- Personal Income Tax Rates in GhanaDocument2 pagesPersonal Income Tax Rates in GhanadanookyereNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- CL Ka and SolutionsDocument4 pagesCL Ka and SolutionsInvisible CionNo ratings yet

- Reinsurance Contract Nature and Original Insured InterestDocument2 pagesReinsurance Contract Nature and Original Insured InterestFlorena CayundaNo ratings yet

- Ichimoku Trader - SignalsDocument6 pagesIchimoku Trader - Signalsviswaa.anupindiNo ratings yet

- ACC 450 - Chapter No. 02 - Professional Standards - Auditing & Assurance Services - UpdatedDocument34 pagesACC 450 - Chapter No. 02 - Professional Standards - Auditing & Assurance Services - Updatedfrozan s naderiNo ratings yet

- Insolvency LawDocument14 pagesInsolvency LawShailesh KumarNo ratings yet

- Investment Management Analysis: Your Company NameDocument70 pagesInvestment Management Analysis: Your Company NameJojoMagnoNo ratings yet

- Application For Opening An Account Under ''Sukanya Samriddhi Account'' FORM-1Document3 pagesApplication For Opening An Account Under ''Sukanya Samriddhi Account'' FORM-1shobsundar1No ratings yet

- D-045 - Engagement Letter For Compilation of Financial Forcast or ProjectionDocument3 pagesD-045 - Engagement Letter For Compilation of Financial Forcast or ProjectionLuis Enrique Altamar Ramos100% (2)

- A Study On Analysis of Cash ManagementDocument73 pagesA Study On Analysis of Cash ManagementchetanNo ratings yet

- Final Version WeWork Article HBS HeaderDocument25 pagesFinal Version WeWork Article HBS HeaderDuc Beo100% (1)

- Chapter 5 MishkinDocument21 pagesChapter 5 MishkinLejla HodzicNo ratings yet

- 2026 SyllabusDocument28 pages2026 Syllabussatkargulia601No ratings yet

- Aac Blocks QuotationDocument1 pageAac Blocks Quotationar.ikpanganibanNo ratings yet

- Cost Sheet FormatDocument5 pagesCost Sheet Formatvicky3230No ratings yet

- Quiz Test 2 KMB FM 05Document1 pageQuiz Test 2 KMB FM 05Vivek Singh RanaNo ratings yet

- ConsiderDocument284 pagesConsiderGhulam NabiNo ratings yet

- Republic of Austria Investor Information PDFDocument48 pagesRepublic of Austria Investor Information PDFMi JpNo ratings yet

- FAC121 - Direct Tax - Assignment 2 - Income From SalaryDocument4 pagesFAC121 - Direct Tax - Assignment 2 - Income From SalaryDeepak DhimanNo ratings yet

- Income Tax CalculatorDocument5 pagesIncome Tax CalculatorTanmay DeshpandeNo ratings yet

- PreferenceSharesDocument1 pagePreferenceSharesTiso Blackstar GroupNo ratings yet

- Notice of Annual General Meeting: Sunil Hitech Engineers LimitedDocument70 pagesNotice of Annual General Meeting: Sunil Hitech Engineers LimitedGaurang MehtaNo ratings yet

- The Impact of E-Banking - Research Report - Without HyphotesisDocument79 pagesThe Impact of E-Banking - Research Report - Without HyphotesisSarfaraz Karim100% (1)

- Educational Institution Tax Exemption CaseDocument1 pageEducational Institution Tax Exemption Casenil qawNo ratings yet

- INV2001082Document1 pageINV2001082Bisi AgomoNo ratings yet

- Httpspartners - edelweiss.insbViewViewSBData# 2Document1 pageHttpspartners - edelweiss.insbViewViewSBData# 2JitendraBhartiNo ratings yet

- Closing Your Savings Account FormDocument1 pageClosing Your Savings Account FormtafseerahmedNo ratings yet

- ECO 531 Chapter 1 Introduction to Money, Banking & Financial MarketsDocument8 pagesECO 531 Chapter 1 Introduction to Money, Banking & Financial MarketsNurul Aina IzzatiNo ratings yet

- N26 StatementDocument4 pagesN26 StatementCris TsauNo ratings yet

- ACCA F7 Revision Mock June 2013 QUESTIONS Version 4 FINAL at 25 March 2013 PDFDocument11 pagesACCA F7 Revision Mock June 2013 QUESTIONS Version 4 FINAL at 25 March 2013 PDFPiyal HossainNo ratings yet

- Ch08 ReceivablesDocument42 pagesCh08 ReceivablesGelyn CruzNo ratings yet