You might also like

- PRESENTATION - ERE - Tactics For Investors To Drive ROIDocument7 pagesPRESENTATION - ERE - Tactics For Investors To Drive ROIO'Connor AssociateNo ratings yet

- Hcad Business Personal Property FaqDocument2 pagesHcad Business Personal Property FaqO'Connor AssociateNo ratings yet

- How To Apply For A Homestead ExemptionDocument6 pagesHow To Apply For A Homestead ExemptionO'Connor AssociateNo ratings yet

- Why O'Connor For Property Tax Reduction?Document7 pagesWhy O'Connor For Property Tax Reduction?O'Connor AssociateNo ratings yet

- Cap Rate Rate ReportDocument207 pagesCap Rate Rate ReportO'Connor Associate0% (1)

- 3 Ways To Reduce Your Commercial Property Taxes With Cost SegregationDocument7 pages3 Ways To Reduce Your Commercial Property Taxes With Cost SegregationO'Connor AssociateNo ratings yet

- The IRS Guidelines For Non-Load Bearing WallsDocument5 pagesThe IRS Guidelines For Non-Load Bearing WallsO'Connor AssociateNo ratings yet

- House Flipping - A New Way of IncomeDocument6 pagesHouse Flipping - A New Way of IncomeO'Connor AssociateNo ratings yet

- Steps To Protest in Harris CountyDocument7 pagesSteps To Protest in Harris CountyO'Connor AssociateNo ratings yet

- Tax Benefits For Home OwnersDocument7 pagesTax Benefits For Home OwnersO'Connor AssociateNo ratings yet

- Top 3 Methods of Valuing Personal PropertyDocument7 pagesTop 3 Methods of Valuing Personal PropertyO'Connor AssociateNo ratings yet

- Property Assessment Appeal To The County Board of EqualizationDocument4 pagesProperty Assessment Appeal To The County Board of EqualizationO'Connor AssociateNo ratings yet

- How Can Cost Segregation Help Minimize Your Tax BurdenDocument6 pagesHow Can Cost Segregation Help Minimize Your Tax BurdenO'Connor AssociateNo ratings yet

- PRESENTATION - OCA - The Thinning Line of Rental Collection in April - 2020Document6 pagesPRESENTATION - OCA - The Thinning Line of Rental Collection in April - 2020O'Connor AssociateNo ratings yet

- 25+ Reasons You SHOULD Protest Your HIGH PROPERTY TAXESDocument8 pages25+ Reasons You SHOULD Protest Your HIGH PROPERTY TAXESO'Connor AssociateNo ratings yet

- Wisconsin Municipal AssessorsDocument48 pagesWisconsin Municipal AssessorsO'Connor AssociateNo ratings yet

- GeorgiaCertificationProgram2017 2018Document2 pagesGeorgiaCertificationProgram2017 2018O'Connor AssociateNo ratings yet

- Hcad Business Personal Property FaqDocument2 pagesHcad Business Personal Property FaqO'Connor AssociateNo ratings yet

- Austin Property Taxpayer Remedies 2017Document1 pageAustin Property Taxpayer Remedies 2017O'Connor AssociateNo ratings yet

- Lincoln Institute of Land Policy's Comparison of 2016 Property TaxesDocument108 pagesLincoln Institute of Land Policy's Comparison of 2016 Property TaxescrainsnewyorkNo ratings yet

- Texas Real Estate InspectorDocument25 pagesTexas Real Estate InspectorO'Connor AssociateNo ratings yet

- Tax DeferralDocument1 pageTax DeferralO'Connor AssociateNo ratings yet

- Commercial Real Estate International Business TrendsDocument21 pagesCommercial Real Estate International Business TrendsNational Association of REALTORS®100% (2)

- Dallascad - Propertytaxoverview2017Document30 pagesDallascad - Propertytaxoverview2017O'Connor AssociateNo ratings yet

- Williamson Cad 2017 Rendition General InformationDocument2 pagesWilliamson Cad 2017 Rendition General InformationO'Connor AssociateNo ratings yet

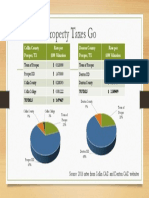

- Where The Property Taxes GoDocument1 pageWhere The Property Taxes GoO'Connor AssociateNo ratings yet

- Dallas Central Appraisal District 2017 2018Document30 pagesDallas Central Appraisal District 2017 2018O'Connor AssociateNo ratings yet

- W C A D: Ise Ounty Ppraisal IstrictDocument43 pagesW C A D: Ise Ounty Ppraisal IstrictO'Connor AssociateNo ratings yet

- 2016 Annual Report TravisCADDocument41 pages2016 Annual Report TravisCADO'Connor AssociateNo ratings yet

- Montgomery County Exemption AnalysisDocument19 pagesMontgomery County Exemption AnalysisO'Connor AssociateNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- CBO Oil and Gas White Paper - The Billion US$ Oil Business + 2013 Marginal Fields Sale Special Report + Full Oil Sector ValuationDocument96 pagesCBO Oil and Gas White Paper - The Billion US$ Oil Business + 2013 Marginal Fields Sale Special Report + Full Oil Sector ValuationD. AtanuNo ratings yet

- FM Study Notes ZellDocument185 pagesFM Study Notes Zell5561 ROSHAN K PATELNo ratings yet

- Exercise ProblemsDocument6 pagesExercise ProblemsDianna Rose Vico100% (1)

- Ijfs 07 00018 With CoverDocument14 pagesIjfs 07 00018 With CoverSultonmurod ZokhidovNo ratings yet

- Classified AdvertisementDocument5 pagesClassified AdvertisementshivanshuNo ratings yet

- Funskool Case Study - Group 3Document7 pagesFunskool Case Study - Group 3Megha MarwariNo ratings yet

- BDO UITFs 2017 PDFDocument4 pagesBDO UITFs 2017 PDFfheruNo ratings yet

- Draft 1 UpadatedDocument38 pagesDraft 1 UpadatedMjean Gonzales GargarNo ratings yet

- 1.3 Interest Rates and Price Volatility (Oct 28) PDFDocument58 pages1.3 Interest Rates and Price Volatility (Oct 28) PDFRedNo ratings yet

- Kimball International case studyDocument4 pagesKimball International case studyVedantBhasinNo ratings yet

- Jetta A5 January 2010Document10 pagesJetta A5 January 2010billydump100% (1)

- Cost of Preferred Stock and Common StockDocument20 pagesCost of Preferred Stock and Common StockPrincess Marie BaldoNo ratings yet

- Beverage Trends AnalysisDocument49 pagesBeverage Trends AnalysisCarlosNo ratings yet

- External Analysis Draft 1Document6 pagesExternal Analysis Draft 1Benjiemar QuirogaNo ratings yet

- Western India Plywood LTDDocument14 pagesWestern India Plywood LTDRafshad mahamood100% (1)

- Case Study-Chinese Negotiation Training On Sales PriceDocument2 pagesCase Study-Chinese Negotiation Training On Sales PriceTilak Salian100% (1)

- SBR Specimen Exam Illustrative Answers PDFDocument14 pagesSBR Specimen Exam Illustrative Answers PDFmi_owextoNo ratings yet

- MasterDataObjects DetailsDocument84 pagesMasterDataObjects Detailsvipparlas100% (1)

- Cost12eppt 18Document29 pagesCost12eppt 18Maika J. PudaderaNo ratings yet

- Maths Chapter 1Document18 pagesMaths Chapter 1Abrha636100% (3)

- Aava ProjectDocument32 pagesAava Projectyogesh0794No ratings yet

- Spouses Zalamea vs. CA PDFDocument15 pagesSpouses Zalamea vs. CA PDFAira Mae LayloNo ratings yet

- Ey - Report - Ipo Q1 2019Document37 pagesEy - Report - Ipo Q1 2019JimmyNo ratings yet

- Cheat Sheet For AccountingDocument4 pagesCheat Sheet For AccountingshihuiNo ratings yet

- F2-02 Sources of DataDocument14 pagesF2-02 Sources of DatavictorpasauNo ratings yet

- ISS22 ShababiDocument36 pagesISS22 ShababiAderito Raimundo MazuzeNo ratings yet

- Masaryk Towers Coop LotteryDocument1 pageMasaryk Towers Coop LotteryThe Lo-DownNo ratings yet

- Questions For MicroeconomicsDocument5 pagesQuestions For MicroeconomicsOliver TalipNo ratings yet

- Financial Markets and Institutions 10th Edition Madura Test BankDocument14 pagesFinancial Markets and Institutions 10th Edition Madura Test Bankmolossesreverse2ypgp7100% (22)

- 7 Pager ContractDocument7 pages7 Pager Contractstar shiningNo ratings yet