You might also like

- Glycemic Index Foundation GI PregnancyDocument2 pagesGlycemic Index Foundation GI PregnancyAnonymous D1h2pKNo ratings yet

- Basis of Design 25000 ReservoirDocument3 pagesBasis of Design 25000 ReservoirAnonymous D1h2pKNo ratings yet

- LLUB StockDocument8 pagesLLUB StockAnonymous D1h2pKNo ratings yet

- April Seasonal Promotion 2020 PDFDocument26 pagesApril Seasonal Promotion 2020 PDFAnonymous D1h2pKNo ratings yet

- Design and Analysis of Clear Water Reservoir-3961Document15 pagesDesign and Analysis of Clear Water Reservoir-3961rrpenolio0% (1)

- Pu Epoxy GroutsDocument6 pagesPu Epoxy GroutsAnonymous D1h2pKNo ratings yet

- GeoTechnical FormulasDocument34 pagesGeoTechnical FormulasTptaylor100% (3)

- Inflation in ColomboDocument27 pagesInflation in ColomboAnonymous D1h2pKNo ratings yet

- Hydrology NotesDocument136 pagesHydrology NotesKaushal KumarNo ratings yet

- Water and Environment EngineeringDocument5 pagesWater and Environment EngineeringAnonymous D1h2pKNo ratings yet

- Right Way of PITDocument16 pagesRight Way of PITAnonymous D1h2pKNo ratings yet

- PT IntroductionDocument35 pagesPT IntroductionAnonymous D1h2pKNo ratings yet

- Column DesignDocument60 pagesColumn DesignAnonymous D1h2pKNo ratings yet

- RC Floor OpeningsDocument6 pagesRC Floor OpeningsAnonymous D1h2pKNo ratings yet

- An Interesting Article About Preliminary SizingDocument5 pagesAn Interesting Article About Preliminary SizingAnonymous D1h2pKNo ratings yet

- Lecture 4 Slabs - Oct 12 - EndDocument131 pagesLecture 4 Slabs - Oct 12 - EndajayNo ratings yet

- FREYSSIBAR prestressing system overviewDocument12 pagesFREYSSIBAR prestressing system overviewFelix Untalan Ebilane JrNo ratings yet

- SLC Vs MLC NAND and The Impact of Technology ScalingDocument10 pagesSLC Vs MLC NAND and The Impact of Technology ScalingAnonymous D1h2pKNo ratings yet

- Tensile Stress - 0.2mm Crack Width - G35 & G40Document1 pageTensile Stress - 0.2mm Crack Width - G35 & G40Anonymous D1h2pKNo ratings yet

- Pres 230Document43 pagesPres 230Runner09No ratings yet

- MESPL Structural Engineering Job PositionsDocument2 pagesMESPL Structural Engineering Job PositionsAnonymous D1h2pKNo ratings yet

- FREYSSIBAR prestressing system overviewDocument12 pagesFREYSSIBAR prestressing system overviewFelix Untalan Ebilane JrNo ratings yet

- Thaipei 101 - Earthquake LoadingDocument69 pagesThaipei 101 - Earthquake LoadingAnonymous D1h2pKNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5784)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- NFJPIA Online Preboard Exam Tax UnformattedDocument22 pagesNFJPIA Online Preboard Exam Tax UnformattedYietNo ratings yet

- CA Ann Rita Linson KDocument2 pagesCA Ann Rita Linson Kdeepaktt7No ratings yet

- Solution Manual For Financial Management Theory and Practice Third Canadian EditionDocument36 pagesSolution Manual For Financial Management Theory and Practice Third Canadian Editionejecthalibutudoh0100% (30)

- Fabm 21Document6 pagesFabm 21kristelNo ratings yet

- HEIRS OF JESUS S. YUJUICO, MARIETTA V. YUJUICO AND DR. NICOLAS VALISNO, SR., RespondentsDocument17 pagesHEIRS OF JESUS S. YUJUICO, MARIETTA V. YUJUICO AND DR. NICOLAS VALISNO, SR., RespondentsVanzNo ratings yet

- BSLR Del 1600447723 1 1Document1 pageBSLR Del 1600447723 1 1AdityaNo ratings yet

- Bachelor of Administration (Hons) in Islamic Finance: Waqf EBB30503Document15 pagesBachelor of Administration (Hons) in Islamic Finance: Waqf EBB30503irfan sururiNo ratings yet

- AA Chapter2Document6 pagesAA Chapter2Nikki GarciaNo ratings yet

- The Punjab Agricultural Income Tax Act 1997 - 0Document9 pagesThe Punjab Agricultural Income Tax Act 1997 - 0Zaid JavaidNo ratings yet

- Unit Vii (Family Business)Document19 pagesUnit Vii (Family Business)Saddam HussainNo ratings yet

- The Sales of Goods Act, Cap.214 R.E 2002Document37 pagesThe Sales of Goods Act, Cap.214 R.E 2002Baraka FrancisNo ratings yet

- Desired Energy PolicyDocument37 pagesDesired Energy PolicyRajiv RanjanNo ratings yet

- Seneca College Course FIP 504-NAA Assignment #1 Case StudyDocument2 pagesSeneca College Course FIP 504-NAA Assignment #1 Case StudySrushti RajNo ratings yet

- AlienationsDocument25 pagesAlienationsAnam KhanNo ratings yet

- FinancePRO Issue1 DecDocument36 pagesFinancePRO Issue1 DecWin GungadinNo ratings yet

- Blockchain Technology Application For Value-Added Tax SystemsDocument27 pagesBlockchain Technology Application For Value-Added Tax SystemsGeysa Pratama EriatNo ratings yet

- Udhemy CourcesDocument1 pageUdhemy CourcesRam Sri100% (1)

- Taxation of Cooperatives and Other CorporatesDocument8 pagesTaxation of Cooperatives and Other CorporatesTriila manillaNo ratings yet

- Solved The Following Information Is For Rainbow National Bank Interest IncomeDocument1 pageSolved The Following Information Is For Rainbow National Bank Interest IncomeM Bilal SaleemNo ratings yet

- Philippines Supreme Court rules on tax deduction for US citizensDocument92 pagesPhilippines Supreme Court rules on tax deduction for US citizens001nooneNo ratings yet

- Reinventing Conservation EasementsDocument44 pagesReinventing Conservation EasementsLincoln Institute of Land PolicyNo ratings yet

- Schedule of Rates (SOR) Tender No. Agl/231/Steel Valves/04-17Document1 pageSchedule of Rates (SOR) Tender No. Agl/231/Steel Valves/04-17Tejash NayakNo ratings yet

- Tamer Mahmoud IBSS IB-modifed 2 PDFDocument21 pagesTamer Mahmoud IBSS IB-modifed 2 PDFTamer AbuelmagdNo ratings yet

- The FYP ReviewDocument47 pagesThe FYP ReviewfypjournalNo ratings yet

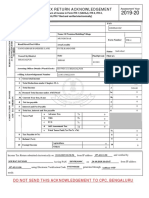

- Indian Income Tax Return Acknowledgement for AY 2019-20Document1 pageIndian Income Tax Return Acknowledgement for AY 2019-20Sourav KumarNo ratings yet

- Bangladesh's Expatriation Process and ChallengesDocument4 pagesBangladesh's Expatriation Process and ChallengesPrithibi IshrakNo ratings yet

- Authority To InvestDocument3 pagesAuthority To InvestThemba MaviNo ratings yet

- Pay Slip Records for Tuition Centre StaffDocument12 pagesPay Slip Records for Tuition Centre StaffThana BalanNo ratings yet

- TeresaZhou (US Tax Resume 06.01. 2015) CADocument3 pagesTeresaZhou (US Tax Resume 06.01. 2015) CALin ZhouNo ratings yet

- Bir RMC No. 97-2021: Philippine Tax Perspective On Social Media InfluencersDocument6 pagesBir RMC No. 97-2021: Philippine Tax Perspective On Social Media InfluencersIvan AnaboNo ratings yet