You might also like

- This Presentation Prepared by Marwan Al QaddoumiDocument45 pagesThis Presentation Prepared by Marwan Al QaddoumiMohamed AbodabashNo ratings yet

- Training Need IdentificationDocument2 pagesTraining Need IdentificationMohamed AbodabashNo ratings yet

- ROADMAP First EditionDocument32 pagesROADMAP First EditionMohamed AbodabashNo ratings yet

- IATA - Information - Paper - On FPL2012 PDFDocument31 pagesIATA - Information - Paper - On FPL2012 PDFMohamed AbodabashNo ratings yet

- Rnav PrinciplesDocument20 pagesRnav PrinciplesMohamed AbodabashNo ratings yet

- GIS For AIMDocument23 pagesGIS For AIMMohamed AbodabashNo ratings yet

- Rnav PrinciplesDocument20 pagesRnav PrinciplesMohamed AbodabashNo ratings yet

- Manual On Air Traffic Forecasting: Doc 8991 AT/722/3Document98 pagesManual On Air Traffic Forecasting: Doc 8991 AT/722/3Mohamed AbodabashNo ratings yet

- 840310Document29 pages840310Mohamed AbodabashNo ratings yet

- GIS For TransportationDocument4 pagesGIS For TransportationMohamed AbodabashNo ratings yet

- MID FPP S. Data House PrespectiveDocument21 pagesMID FPP S. Data House PrespectiveMohamed AbodabashNo ratings yet

- Chap 07Document73 pagesChap 07Mohamed AbodabashNo ratings yet

- EE6900 Flight Management Systems: "Databases"Document56 pagesEE6900 Flight Management Systems: "Databases"Mohamed AbodabashNo ratings yet

- Airports in Cities and RegionsDocument192 pagesAirports in Cities and RegionsMarlar Shwe100% (2)

- Caso Aeropuerto PronosticoDocument24 pagesCaso Aeropuerto Pronosticoafmv1089No ratings yet

- AirportCities TheEvolutionDocument4 pagesAirportCities TheEvolutionRafael Franco100% (1)

- Airport Mapping DatabasesDocument8 pagesAirport Mapping DatabasesMohamed AbodabashNo ratings yet

- Conducting Aero StudyDocument4 pagesConducting Aero StudyMohamed AbodabashNo ratings yet

- Airport System DevelopmentDocument259 pagesAirport System DevelopmentMohamed AbodabashNo ratings yet

- ACRP SMS GuidebookDocument177 pagesACRP SMS Guidebooksherio9No ratings yet

- Airfield Capacity 04 BWDocument14 pagesAirfield Capacity 04 BWBoriana ValkovaNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- cl1 AerDocument4 pagescl1 AerrafallaferNo ratings yet

- Air Astra NafisDocument4 pagesAir Astra NafisNafis SadikNo ratings yet

- SG Cover New Template 2014Document36 pagesSG Cover New Template 2014Santhanam ChandrasekaranNo ratings yet

- How Tata Built India - Two Centuries of Indian Business - mp4Document4 pagesHow Tata Built India - Two Centuries of Indian Business - mp4NISHANT395No ratings yet

- CH08 VAT On ImportationDocument35 pagesCH08 VAT On Importationwilma olivoNo ratings yet

- Terms and Conditions of Carriage enDocument32 pagesTerms and Conditions of Carriage enMuhammad AsifNo ratings yet

- Journal of Air Transport Management: Paolo Beria, Hans-Martin Niemeier, Karsten FröhlichDocument6 pagesJournal of Air Transport Management: Paolo Beria, Hans-Martin Niemeier, Karsten FröhlichFrancesco GiuntaNo ratings yet

- BCBP Implementation Guidev4 Jun2009 PDFDocument134 pagesBCBP Implementation Guidev4 Jun2009 PDFCsaba NagyNo ratings yet

- Syllabus (Intro - Transportation)Document12 pagesSyllabus (Intro - Transportation)marieNo ratings yet

- Philippine Airlines - WikipediaDocument23 pagesPhilippine Airlines - WikipediaJohn Matthew Callanta100% (1)

- Gopesh Obalappa Pilot ResumeDocument3 pagesGopesh Obalappa Pilot ResumeGopesh ObalappaNo ratings yet

- Strengths of Kingfisher: Executive SummaryDocument3 pagesStrengths of Kingfisher: Executive SummaryKavitha kavithaNo ratings yet

- Passengers' Perspective of Philippine Airlines Within Nueva EcijaDocument15 pagesPassengers' Perspective of Philippine Airlines Within Nueva EcijaPoonam KilaniyaNo ratings yet

- Alfredo Manay V Cebu Air Inc DigestDocument2 pagesAlfredo Manay V Cebu Air Inc DigestRaff GonzalesNo ratings yet

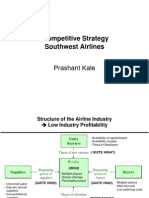

- Competitive Strategy Southwest Airlines: Prashant KaleDocument8 pagesCompetitive Strategy Southwest Airlines: Prashant KaleJose KelleyNo ratings yet

- ADVENT'19 Encipher: Case It To Ace It: The Commerce Society - Kirori Mal CollegeDocument3 pagesADVENT'19 Encipher: Case It To Ace It: The Commerce Society - Kirori Mal CollegeParth ChawlaNo ratings yet

- Cxannual Result enDocument34 pagesCxannual Result endescent3dNo ratings yet

- Vice President Director Operations Aviation in New York NY Resume William ClineDocument2 pagesVice President Director Operations Aviation in New York NY Resume William ClineWilliamCline2No ratings yet

- British Airways Strategic PlanDocument49 pagesBritish Airways Strategic PlanVu Ngoc Quy93% (61)

- Stakeholder Model Answers Business IBDocument1 pageStakeholder Model Answers Business IBberenika netíkováNo ratings yet

- Case Electrolux and EmiratesDocument4 pagesCase Electrolux and EmiratesAveiro PattyNo ratings yet

- Delta Airlines PresentationDocument28 pagesDelta Airlines Presentationjdhillon106No ratings yet

- Presented To: Presented By:: Sir Asif Iqbal Taqdees Tahir Muhammad Shahid Nasir Saleem Syed Haider Ali Omair AhsanDocument16 pagesPresented To: Presented By:: Sir Asif Iqbal Taqdees Tahir Muhammad Shahid Nasir Saleem Syed Haider Ali Omair AhsanShoaibJawadNo ratings yet

- USAF - Cost Index FlyingDocument51 pagesUSAF - Cost Index FlyingpepegoesdigitalNo ratings yet

- Thomas Cook BankruptiesDocument11 pagesThomas Cook BankruptiesRakesh RaiNo ratings yet

- Scenario Planning at British Airways PDFDocument10 pagesScenario Planning at British Airways PDFCherry NanaNo ratings yet

- Air Cargo Final Project CcompltedDocument11 pagesAir Cargo Final Project Ccompltedwahaj100% (1)

- Bae Case StudyDocument4 pagesBae Case StudyKashis SinghNo ratings yet

- Emirates Airlines ThesisDocument8 pagesEmirates Airlines Thesissheenacrouchmurfreesboro100% (2)

- Jet AirwaysDocument31 pagesJet AirwaysVipul ShettyNo ratings yet