You might also like

- In The United States District Court For The Northern District of Illinois Eastern DivisionDocument13 pagesIn The United States District Court For The Northern District of Illinois Eastern DivisionForeclosure FraudNo ratings yet

- Class Action V Invitation HomesDocument17 pagesClass Action V Invitation HomesForeclosure Fraud100% (4)

- Statement Bank March Delavid Distributor LLC A2cb2f38f9Document10 pagesStatement Bank March Delavid Distributor LLC A2cb2f38f9Madelyn Vasquez100% (1)

- LPS Mortgage Monitor May 2010 FinalDocument30 pagesLPS Mortgage Monitor May 2010 FinalForeclosure FraudNo ratings yet

- Credit Scoring: Beyond The NumbersDocument34 pagesCredit Scoring: Beyond The NumbersramssravaniNo ratings yet

- 072420-Commercial Mortgage Market Monitor June 2020Document58 pages072420-Commercial Mortgage Market Monitor June 2020KyleNo ratings yet

- Macro Prudential MemoDocument10 pagesMacro Prudential Memoumidjon.abdullaev8161No ratings yet

- Fortnightly Banking Update: Deposit Growth Moderated But Bank Credit Growth Moderates Even MoreDocument3 pagesFortnightly Banking Update: Deposit Growth Moderated But Bank Credit Growth Moderates Even Morekumar ganeshNo ratings yet

- Banking and ManagementDocument9 pagesBanking and ManagementDevlent OmondiNo ratings yet

- Lender 1cqhdubbv - 478333Document45 pagesLender 1cqhdubbv - 478333DGLNo ratings yet

- Foreclosure Slowdown The Road AheadDocument7 pagesForeclosure Slowdown The Road AheaddrifferNo ratings yet

- MALAYSIA MONETARY UPDATEDocument6 pagesMALAYSIA MONETARY UPDATEChellene ChngNo ratings yet

- Presentation On CGTMSE and Upcoming OpportunitiesDocument16 pagesPresentation On CGTMSE and Upcoming OpportunitiesAkshay JainNo ratings yet

- Indicative Annualized Rates On Deposits W.E .F - 01 .01.2022 To 31 .03.2022Document4 pagesIndicative Annualized Rates On Deposits W.E .F - 01 .01.2022 To 31 .03.2022Afaq YousafNo ratings yet

- Household Debt and Credit: Quarterly Report OnDocument38 pagesHousehold Debt and Credit: Quarterly Report Onrichardck50No ratings yet

- Monetary Authority of Singapore - Interest Rates of Banks and Finance CompaniesDocument4 pagesMonetary Authority of Singapore - Interest Rates of Banks and Finance CompaniesMunif MuhammadNo ratings yet

- HANOI UNIVERSITY REPORTDocument8 pagesHANOI UNIVERSITY REPORTQuynh Ngoc DangNo ratings yet

- 2022 Global Outlook The Success and Excesses Resulting From Mp3 PoliciesDocument10 pages2022 Global Outlook The Success and Excesses Resulting From Mp3 PoliciesDEV FreelancerNo ratings yet

- Bank Management ProjectDocument20 pagesBank Management ProjectK M Tanveer AhmedNo ratings yet

- Highlights of Monitary Policy 2020Document15 pagesHighlights of Monitary Policy 2020Raushan KumarNo ratings yet

- Choose The Correct Answer From The Given Four Alternatives:: Not Attempt!!!! Public Provident FundDocument11 pagesChoose The Correct Answer From The Given Four Alternatives:: Not Attempt!!!! Public Provident FundHari BabuNo ratings yet

- Sizing The Impact of The Banking Crisis On The Broader EconomyDocument8 pagesSizing The Impact of The Banking Crisis On The Broader EconomyAlen SaricNo ratings yet

- Mercer-Capital Bank Valuation AKG PDFDocument60 pagesMercer-Capital Bank Valuation AKG PDFDesmond Dujon HenryNo ratings yet

- Banking: CHAPTER A: Brief About The Indian Banking SectorDocument63 pagesBanking: CHAPTER A: Brief About The Indian Banking SectorDevang ParabNo ratings yet

- Key Rates Market Briefs: Average 10-Year Treasury vs. 30-Day LIBORDocument1 pageKey Rates Market Briefs: Average 10-Year Treasury vs. 30-Day LIBORapi-33843559No ratings yet

- Nestle India LTD.: ON Financial Statement Analysis ofDocument24 pagesNestle India LTD.: ON Financial Statement Analysis ofAparna SharmaNo ratings yet

- 2010 February HFCDocument13 pages2010 February HFCAmol MahajanNo ratings yet

- New Approaches To SME Finance Using Bank Account Information (Big Data)Document19 pagesNew Approaches To SME Finance Using Bank Account Information (Big Data)ADBI EventsNo ratings yet

- Deep Learning For Mortgage RiskDocument75 pagesDeep Learning For Mortgage Risk劉軒宇No ratings yet

- Household Debt and Credit: Quarterly Report OnDocument38 pagesHousehold Debt and Credit: Quarterly Report OnTsvetan KintisheffNo ratings yet

- Financial Risk ManagementDocument30 pagesFinancial Risk ManagementVarun Kumar ChalotraNo ratings yet

- Afr Session 1Document154 pagesAfr Session 1holden.mortaxeNo ratings yet

- Global Payments 2016Document44 pagesGlobal Payments 2016Sayali SinghiNo ratings yet

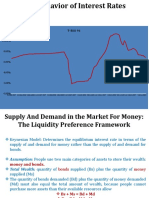

- F-309 CH 05 Behavior of Interest RatesDocument14 pagesF-309 CH 05 Behavior of Interest RatesSaikat SahaNo ratings yet

- Resource 20221117092754 WSC - Case - ClassDocument51 pagesResource 20221117092754 WSC - Case - ClassRajat OnzNo ratings yet

- Mridul Tiwari - Mridul Tiwari - PGPGM03 - 13 - IE - FMDocument4 pagesMridul Tiwari - Mridul Tiwari - PGPGM03 - 13 - IE - FMekta agarwalNo ratings yet

- Case 2Document2 pagesCase 2hamza hamzaNo ratings yet

- March-June 2021 Market OutlookDocument42 pagesMarch-June 2021 Market OutlookRam PrasadNo ratings yet

- Mortgage Delinquency Rates: Mba Commercial/MultifamilyDocument10 pagesMortgage Delinquency Rates: Mba Commercial/MultifamilyZerohedgeNo ratings yet

- TCBS Vietnam Investment Channels Update 3M2023Document14 pagesTCBS Vietnam Investment Channels Update 3M2023ÁnhTâmNo ratings yet

- I. Views On The EconomyDocument3 pagesI. Views On The EconomyThanh NguyenNo ratings yet

- Microequities Deep Value Microcap Fund March 2011 UpdateDocument1 pageMicroequities Deep Value Microcap Fund March 2011 UpdateMicroequities Pty LtdNo ratings yet

- JPM Default RecoveryDocument19 pagesJPM Default Recoverymarmaud2754No ratings yet

- Evaluating Consumer Loans: William Chittenden Edited and Updated The Powerpoint Slides For This EditionDocument61 pagesEvaluating Consumer Loans: William Chittenden Edited and Updated The Powerpoint Slides For This Edition分享区No ratings yet

- Ey Australia Audit Inspection Report 2021Document6 pagesEy Australia Audit Inspection Report 2021melodysze210593No ratings yet

- RealPoint CMBS Methodology DisclosureDocument19 pagesRealPoint CMBS Methodology DisclosureCarneadesNo ratings yet

- Debt Dynamics: Speech Given by Ben BroadbentDocument20 pagesDebt Dynamics: Speech Given by Ben BroadbentHao WangNo ratings yet

- Group Members:: Comparison Between Bank AL Habib & Habib Metro BankDocument13 pagesGroup Members:: Comparison Between Bank AL Habib & Habib Metro BankAbbas AliNo ratings yet

- BCG India Economic Monitor Dec 2020Document42 pagesBCG India Economic Monitor Dec 2020akashNo ratings yet

- 2009 October Rbi PolicyDocument8 pages2009 October Rbi PolicysammyNo ratings yet

- Understanding The Recent Monetary Policy and What It Entails For The Nigerian Economy - Ugochukwu AnthonyDocument10 pagesUnderstanding The Recent Monetary Policy and What It Entails For The Nigerian Economy - Ugochukwu Anthonyabdulbasitabdulazeez30No ratings yet

- Financial Institutions Management - Solutions - Chap008Document19 pagesFinancial Institutions Management - Solutions - Chap008duncan01234No ratings yet

- Apollo Outlook for US Regional Banks 1707758510Document147 pagesApollo Outlook for US Regional Banks 1707758510Saul VillarrealNo ratings yet

- Weekly Economic & Financial Commentary 15julyDocument13 pagesWeekly Economic & Financial Commentary 15julyErick Abraham MarlissaNo ratings yet

- Monetary: TrendsDocument20 pagesMonetary: Trendsapi-25887578No ratings yet

- Liquidity FundDocument3 pagesLiquidity Fundtangkc09No ratings yet

- Fca B SiddharthDocument12 pagesFca B SiddharthSiddharth SangtaniNo ratings yet

- Weekly Economic & Financial Commentary 14octDocument13 pagesWeekly Economic & Financial Commentary 14octErick Abraham MarlissaNo ratings yet

- Weekly Economic & Financial Commentary 10novDocument12 pagesWeekly Economic & Financial Commentary 10novErick Abraham MarlissaNo ratings yet

- Foreclosure Prevention & Refinance Report: Federal Property Manager'S Report Second Quarter 2021Document50 pagesForeclosure Prevention & Refinance Report: Federal Property Manager'S Report Second Quarter 2021Foreclosure FraudNo ratings yet

- Alabama Association of Realtors, Et Al.,: ApplicantsDocument52 pagesAlabama Association of Realtors, Et Al.,: ApplicantsForeclosure FraudNo ratings yet

- Hyper Vac AnyDocument41 pagesHyper Vac AnyForeclosure FraudNo ratings yet

- Alabama Association of Realtors, Et Al.,: ApplicantsDocument19 pagesAlabama Association of Realtors, Et Al.,: ApplicantsForeclosure FraudNo ratings yet

- ResponseDocument27 pagesResponseForeclosure FraudNo ratings yet

- State of New York: The People of The State of New York, Represented in Senate and Assem-Bly, Do Enact As FollowsDocument2 pagesState of New York: The People of The State of New York, Represented in Senate and Assem-Bly, Do Enact As FollowsForeclosure FraudNo ratings yet

- Harvard Jchs Covid Impact Landlords Survey de La Campa 2021Document50 pagesHarvard Jchs Covid Impact Landlords Survey de La Campa 2021Foreclosure FraudNo ratings yet

- SCOTUS Docket No. 21A23Document16 pagesSCOTUS Docket No. 21A23Chris GeidnerNo ratings yet

- Response in OppositionDocument36 pagesResponse in OppositionForeclosure FraudNo ratings yet

- Fhfa Hud Mou - 8122021Document13 pagesFhfa Hud Mou - 8122021Foreclosure FraudNo ratings yet

- Sixth Circuit Rent MoratoriumDocument13 pagesSixth Circuit Rent Moratoriumstreiff at redstateNo ratings yet

- Eviction and Crime: A Neighborhood Analysis in PhiladelphiaDocument26 pagesEviction and Crime: A Neighborhood Analysis in PhiladelphiaForeclosure FraudNo ratings yet

- Et Al. Plaintiffs-Appellees v. Et Al. Defendants-AppellantsDocument18 pagesEt Al. Plaintiffs-Appellees v. Et Al. Defendants-AppellantsForeclosure FraudNo ratings yet

- Complaint CD Cal La Eviction MoratoriumDocument27 pagesComplaint CD Cal La Eviction MoratoriumForeclosure Fraud100% (1)

- 8.11.2021 Letter To President Biden Opposing Eviction MoratoriumDocument5 pages8.11.2021 Letter To President Biden Opposing Eviction MoratoriumForeclosure FraudNo ratings yet

- Not For Publication Without The Approval of The Appellate DivisionDocument9 pagesNot For Publication Without The Approval of The Appellate DivisionForeclosure FraudNo ratings yet

- Ny Tenant Scot Us RLG 081221Document5 pagesNy Tenant Scot Us RLG 081221Foreclosure FraudNo ratings yet

- Et Al.,: in The United States District Court For The District of ColumbiaDocument8 pagesEt Al.,: in The United States District Court For The District of ColumbiaRHTNo ratings yet

- Eviction MoratoriumDocument20 pagesEviction MoratoriumZerohedgeNo ratings yet

- MFPO AlbertelliDocument13 pagesMFPO AlbertelliForeclosure Fraud100% (3)

- D C O A O T S O F: Merlande Richard and Elie RichardDocument5 pagesD C O A O T S O F: Merlande Richard and Elie RichardDinSFLANo ratings yet

- 11th Circuit JacksonDocument51 pages11th Circuit JacksonForeclosure FraudNo ratings yet

- No. 2D16-273Document5 pagesNo. 2D16-273Foreclosure FraudNo ratings yet

- Bills 115s2155enrDocument73 pagesBills 115s2155enrForeclosure FraudNo ratings yet

- Out Reach: The High Cost of HousingDocument284 pagesOut Reach: The High Cost of HousingForeclosure Fraud100% (1)

- D C O A O T S O F: Caryn Hall Yost-RudgeDocument6 pagesD C O A O T S O F: Caryn Hall Yost-RudgeForeclosure Fraud100% (1)

- Jackson v. Bank of AmericaDocument50 pagesJackson v. Bank of AmericaForeclosure Fraud100% (2)

- Robo Witness DestroyedDocument8 pagesRobo Witness DestroyedForeclosure Fraud100% (4)

- Part 01 - CH 03-Computing The TaxDocument51 pagesPart 01 - CH 03-Computing The TaxwdlzfrzNo ratings yet

- Reading 2 KeyDocument4 pagesReading 2 KeyNguyễn Văn NguyênNo ratings yet

- Summer Dhamaka AprilDocument21 pagesSummer Dhamaka AprilPapia ChandaNo ratings yet

- Benefits of Post Office Savings AccountsDocument7 pagesBenefits of Post Office Savings Accounts2K22/BAE/79 KESHAV GARGNo ratings yet

- Sadaf StatementDocument37 pagesSadaf StatementadilfaqiNo ratings yet

- Moi Midterm Reviewer Module 1 2 PDFDocument7 pagesMoi Midterm Reviewer Module 1 2 PDFBanana QNo ratings yet

- ACC208 Sem 2 2021Document3 pagesACC208 Sem 2 202120220354No ratings yet

- State Tax FormDocument2 pagesState Tax FormRon SchingsNo ratings yet

- Pledge, MortgageDocument9 pagesPledge, MortgageAmie Jane MirandaNo ratings yet

- Personal Management - Teddy (Worksheet - Typed Copy) 2-4-23Document12 pagesPersonal Management - Teddy (Worksheet - Typed Copy) 2-4-23tedNo ratings yet

- Official Form 309A (For Individuals or Joint Debtors) : Order and Notice of Chapter 7 Bankruptcy Case 01/19Document3 pagesOfficial Form 309A (For Individuals or Joint Debtors) : Order and Notice of Chapter 7 Bankruptcy Case 01/19Anonymous Te6DQINo ratings yet

- Debt Reduction Calculator - Pay Off Debts Faster With This Free Online ToolDocument4 pagesDebt Reduction Calculator - Pay Off Debts Faster With This Free Online ToolLittlebeeNo ratings yet

- Benefit Illu1212Document3 pagesBenefit Illu1212parikshitNo ratings yet

- MCB BankDocument9 pagesMCB Bankmama naveedNo ratings yet

- Iwan Pratama: IDR 2,418,071.32 IDR 2,575,789.00Document2 pagesIwan Pratama: IDR 2,418,071.32 IDR 2,575,789.00iwan pratamaNo ratings yet

- Format CBFT - Pagos ExteriorDocument9 pagesFormat CBFT - Pagos ExteriorCarlos PasosNo ratings yet

- Ordinary and Deferred Annuity Sample ProblemsDocument8 pagesOrdinary and Deferred Annuity Sample ProblemsErvin Russel RoñaNo ratings yet

- E-Auction Sale of Assets for Sunlight ExtrusionDocument1 pageE-Auction Sale of Assets for Sunlight ExtrusionVishalNo ratings yet

- Power of Commissioner Penalties PDFDocument14 pagesPower of Commissioner Penalties PDFKomal JaiswalNo ratings yet

- Macroeconomics Canada in The Global Environment Canadian 9th Edition Parkin Solutions Manual Full DownloadDocument18 pagesMacroeconomics Canada in The Global Environment Canadian 9th Edition Parkin Solutions Manual Full Downloadlisawilliamsqcojzynfrw100% (36)

- Form D Form of Application For Commutation On Pension Without Medical Examination 20210224121358Document2 pagesForm D Form of Application For Commutation On Pension Without Medical Examination 20210224121358Raman KatariaNo ratings yet

- Official Payslip: Department of EducationDocument1 pageOfficial Payslip: Department of EducationCamillo Kopa100% (1)

- 49m Dr.gabriel_29may2020 EffendyDocument5 pages49m Dr.gabriel_29may2020 EffendyFaith Wave driveNo ratings yet

- Estmt - 2023 08 29Document8 pagesEstmt - 2023 08 29andreasarahi2011No ratings yet

- Npa ProjectDocument67 pagesNpa ProjectYemmiganur townNo ratings yet

- e-StatementBRImo 025901001131564 Jan2024 20240302 153141Document23 pagese-StatementBRImo 025901001131564 Jan2024 20240302 153141haerulamri554No ratings yet

- W-2 Wage Reconciliation: This Form Details Your Final 2019 Payroll EarningsDocument2 pagesW-2 Wage Reconciliation: This Form Details Your Final 2019 Payroll EarningsChantale0% (1)

- Ibs Ipoh Main, Jsis 1 30/09/22Document3 pagesIbs Ipoh Main, Jsis 1 30/09/22JGL MOTORNo ratings yet

- Sample Midterm QuestionDocument3 pagesSample Midterm QuestionAleema RokaiyaNo ratings yet