You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Combo Debt Dispute LetterDocument4 pagesCombo Debt Dispute Letterfgtrulin91% (47)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Revolving Credit AgreementDocument2 pagesRevolving Credit AgreementRocketLawyerNo ratings yet

- Your Rewards: Bmo Cashback MastercardDocument5 pagesYour Rewards: Bmo Cashback Mastercardhananahmad114No ratings yet

- Bank Statement Template 4 - TemplateLabDocument1 pageBank Statement Template 4 - TemplateLabStart AmazonNo ratings yet

- Maybank MalaysiaDocument8 pagesMaybank MalaysiaChg Fang Jia Ji75% (8)

- Internet Banking and Mobile Banking - Safe and Secure BankingDocument99 pagesInternet Banking and Mobile Banking - Safe and Secure BankingRehanCoolestBoy0% (1)

- Abm Basic DocumentsDocument6 pagesAbm Basic DocumentsAmimah Balt GuroNo ratings yet

- Display PDFDocument3 pagesDisplay PDFMartin SabahNo ratings yet

- Geojit Financial Services LTD.,: Pay Slip - July 2019Document1 pageGeojit Financial Services LTD.,: Pay Slip - July 2019sanjit deyNo ratings yet

- Project Report On E-BankingDocument60 pagesProject Report On E-BankingAshis karmakar100% (3)

- BRPD-15 (Re-Sheduling)Document8 pagesBRPD-15 (Re-Sheduling)Superb AdnanNo ratings yet

- Case 13Document12 pagesCase 13Superb AdnanNo ratings yet

- 08 Chapter 3Document53 pages08 Chapter 3Superb AdnanNo ratings yet

- Chapter 17 - Industry, Page 1 of 4Document4 pagesChapter 17 - Industry, Page 1 of 4Superb AdnanNo ratings yet

- Introduction of Faysal BankDocument7 pagesIntroduction of Faysal BankAroosa nazNo ratings yet

- CCD - Other Channels V5.1Document2 pagesCCD - Other Channels V5.1Pranay ShitoleNo ratings yet

- Current Developments in EconomyDocument193 pagesCurrent Developments in EconomygandhingNo ratings yet

- Syria: Goods Documents Required Customs Prescriptions RemarksDocument4 pagesSyria: Goods Documents Required Customs Prescriptions RemarksKelz YouknowmynameNo ratings yet

- Existence 2Document2 pagesExistence 2Demar Ancog100% (1)

- ARM Versus Fixed-Rate Mortgage Comparison: Amount of LoanDocument3 pagesARM Versus Fixed-Rate Mortgage Comparison: Amount of LoanDery YanwarNo ratings yet

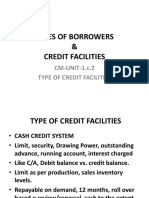

- CM Unit 1.c.2 TYPES of Credit FacilitiesDocument8 pagesCM Unit 1.c.2 TYPES of Credit Facilitiesabdullahi shafiuNo ratings yet

- Life Underwriting RiskDocument49 pagesLife Underwriting RiskDiana MitroiNo ratings yet

- State Bank of Travancore Recruitment 2013 1030 Peon Posts Apply OnlineDocument6 pagesState Bank of Travancore Recruitment 2013 1030 Peon Posts Apply OnlinemalaarunNo ratings yet

- Faisal Bank HRM SystemsDocument31 pagesFaisal Bank HRM SystemsShoaib HasanNo ratings yet

- The Role of Computer in Enhancing BankingDocument10 pagesThe Role of Computer in Enhancing Bankinghibbuh100% (1)

- Badio, Aripah - Commrevdigest PDFDocument121 pagesBadio, Aripah - Commrevdigest PDFEpah SBNo ratings yet

- RBC SpreadsheetSupplementDocument5 pagesRBC SpreadsheetSupplementAkash46No ratings yet

- Bajaj Allianz ProjectDocument57 pagesBajaj Allianz ProjectNischithNo ratings yet

- Cooperative SocietyDocument5 pagesCooperative SocietyGuruprasad PatelNo ratings yet

- Quantum GravityDocument2 pagesQuantum GravitySubhodeep BanerjeeNo ratings yet

- KOTAK CORRECTIONfiDocument75 pagesKOTAK CORRECTIONfiNicy JoyNo ratings yet

- Importance of A Trial BalanceDocument1 pageImportance of A Trial Balancedanookyere100% (3)

- GR 109666, Republic of The PhilippinesDocument9 pagesGR 109666, Republic of The PhilippinesIan Lemuel CahindeNo ratings yet

- Internship Report On Generel Banking Activities of Exim BankDocument57 pagesInternship Report On Generel Banking Activities of Exim BankMorshedul Hasan100% (2)