You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Digital Marketing in IndiaDocument88 pagesDigital Marketing in IndiaVivek Singh100% (1)

- Accounting of BankingDocument32 pagesAccounting of BankingVivek SinghNo ratings yet

- Export Procedure M COM IMDocument34 pagesExport Procedure M COM IMVivek SinghNo ratings yet

- Training Development Final 13-1-2014Document43 pagesTraining Development Final 13-1-2014Vivek SinghNo ratings yet

- Upload Sip Report HDFC Bank DigitizationDocument64 pagesUpload Sip Report HDFC Bank DigitizationVivek SinghNo ratings yet

- Pricing StrategiesDocument28 pagesPricing StrategiesnaraincNo ratings yet

- Merger and AcquisitionDocument49 pagesMerger and AcquisitionVivek Singh0% (1)

- Flipkart Vs Amazon India: Who Won The Indian Ecommerce Battle in 2018?Document3 pagesFlipkart Vs Amazon India: Who Won The Indian Ecommerce Battle in 2018?Vivek SinghNo ratings yet

- Finance ProjectDocument49 pagesFinance ProjectVivek SinghNo ratings yet

- Conflict ManagementDocument73 pagesConflict Managementwelcome2jungle100% (1)

- Entrepreneurship M COM PROJECTDocument34 pagesEntrepreneurship M COM PROJECTVivek Singh67% (3)

- Rural Entrepreneurship M COMDocument46 pagesRural Entrepreneurship M COMVivek SinghNo ratings yet

- PRICING MODIFY Final For Print 2-3-2014Document38 pagesPRICING MODIFY Final For Print 2-3-2014Vivek SinghNo ratings yet

- Pricing StrategieDocument38 pagesPricing StrategieVivek SinghNo ratings yet

- Marketing - Fruit YogurtDocument44 pagesMarketing - Fruit YogurtVivek SinghNo ratings yet

- Marketing Mix StartegyDocument48 pagesMarketing Mix StartegyVivek SinghNo ratings yet

- Economics QuestionsDocument2 pagesEconomics QuestionsVivek SinghNo ratings yet

- SM M ComDocument36 pagesSM M ComVivek SinghNo ratings yet

- Training Development Final 13-1-2014Document43 pagesTraining Development Final 13-1-2014Vivek SinghNo ratings yet

- Trainign and Development MTNL Semi FinalDocument44 pagesTrainign and Development MTNL Semi FinalVivek SinghNo ratings yet

- Project On NestleDocument68 pagesProject On NestleVivek Singh0% (2)

- Balance of PaymentDocument40 pagesBalance of PaymentVivek SinghNo ratings yet

- MC Donalds Supply Chain ManagementDocument15 pagesMC Donalds Supply Chain ManagementVivek Singh0% (1)

- Marketing ResearchDocument38 pagesMarketing ResearchareebahussainNo ratings yet

- McDonald Supply Chain FinallllllllDocument19 pagesMcDonald Supply Chain FinallllllllVivek Singh100% (1)

- Strategy of Dabur With Special Reference To Dabur Chyawanprash For Rural MarketDocument117 pagesStrategy of Dabur With Special Reference To Dabur Chyawanprash For Rural MarketVivek Singh100% (2)

- Brandpositioning Samsung11 130103082443 Phpapp01Document11 pagesBrandpositioning Samsung11 130103082443 Phpapp01Vivek SinghNo ratings yet

- Role of Sidbi IndexDocument1 pageRole of Sidbi IndexVivek SinghNo ratings yet

- BPO Stree ManagementOBDocument32 pagesBPO Stree ManagementOBVivek SinghNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Business Ethics ProjectDocument23 pagesBusiness Ethics ProjectGarima SinghalNo ratings yet

- KGSGDocument7 pagesKGSGAnonymous V9E1ZJtwoENo ratings yet

- Summer Bonanza TermsDocument55 pagesSummer Bonanza TermsHaresh Kumar UlaganambiNo ratings yet

- International trade guide to letters of credit and financingDocument17 pagesInternational trade guide to letters of credit and financingSumayra RahmanNo ratings yet

- Income Under The Head Capital Gains Section 45 (1) : (Charging Section)Document9 pagesIncome Under The Head Capital Gains Section 45 (1) : (Charging Section)hemantNo ratings yet

- Morgan Stanley First Quarter 2019 Earnings Results: Morgan Stanley Reports Net Revenues of $10.3 Billion and EPS of $1.39Document9 pagesMorgan Stanley First Quarter 2019 Earnings Results: Morgan Stanley Reports Net Revenues of $10.3 Billion and EPS of $1.39Valter SilveiraNo ratings yet

- Trade Finance: GuideDocument36 pagesTrade Finance: Guidesujitranair100% (1)

- Estatement20230706 000233440Document3 pagesEstatement20230706 000233440Mia NahilaNo ratings yet

- Four Pillars of Finance and Phil Financial System OverviewDocument29 pagesFour Pillars of Finance and Phil Financial System OverviewGrant Marco Mariano90% (10)

- Teofisto Guingona vs. City Fiscal of ManilaDocument2 pagesTeofisto Guingona vs. City Fiscal of ManilaVienie Ramirez Badang100% (1)

- Habib and Padayachee - 2000 - Economic Policy and Power Relations in South AfricaDocument19 pagesHabib and Padayachee - 2000 - Economic Policy and Power Relations in South AfricaBasanda Nondlazi100% (1)

- Instructor Manual For Financial Managerial Accounting 16th Sixteenth Edition by Jan R Williams Sue F Haka Mark S Bettner Joseph V CarcelloDocument14 pagesInstructor Manual For Financial Managerial Accounting 16th Sixteenth Edition by Jan R Williams Sue F Haka Mark S Bettner Joseph V CarcelloLindaCruzykeaz100% (80)

- Your Strawman (Legal Fiction)Document31 pagesYour Strawman (Legal Fiction)Karl_23100% (4)

- CDRD Revised Tariff Guide 2020Document11 pagesCDRD Revised Tariff Guide 2020Atlas Microfinance LtdNo ratings yet

- Economic and Financial Crimes CommissionDocument3 pagesEconomic and Financial Crimes CommissionPascal EgbendaNo ratings yet

- Mail From ANisDocument3 pagesMail From ANissantolaseNo ratings yet

- Form 3CBDocument12 pagesForm 3CBpriya sharmaNo ratings yet

- Sewale Bitew PDFDocument84 pagesSewale Bitew PDFTILAHUNNo ratings yet

- 7 Agricultural FinanceDocument24 pages7 Agricultural FinanceNEERAJA UNNINo ratings yet

- Thomson Reuters Knowledge to Act OverviewDocument19 pagesThomson Reuters Knowledge to Act OverviewSashi DandamudiNo ratings yet

- Ds Team D Group ProjectDocument57 pagesDs Team D Group ProjectRenuka Badhoria (HRM 21-23)No ratings yet

- BBP Document Dufil - TRM - Module - As-Is v21052021Document53 pagesBBP Document Dufil - TRM - Module - As-Is v21052021RaviNo ratings yet

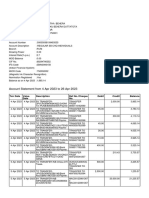

- Account statement from 4 Apr 2023 to 26 Apr 2023Document7 pagesAccount statement from 4 Apr 2023 to 26 Apr 2023BIKRAM KUMAR BEHERANo ratings yet

- First Consolidated BankDocument3 pagesFirst Consolidated BankMichael John LunaNo ratings yet

- Teacher's Handout MoneyDocument5 pagesTeacher's Handout MoneyannNo ratings yet

- Important Simple Interest Practice Questions for Bank ExamsDocument15 pagesImportant Simple Interest Practice Questions for Bank ExamsKothapalli VinayNo ratings yet

- ICICI Prudential ProjectDocument52 pagesICICI Prudential Projectapi-3830923100% (13)

- Terms and Conditions EToroDocument42 pagesTerms and Conditions EToroZhess BugNo ratings yet

- Analysis of Frauds in Indian Banking SectorDocument4 pagesAnalysis of Frauds in Indian Banking SectorEditor IJTSRD100% (1)

- 2020 113 Taxmann Com 36 SAT Mumbai 10 10 2019Document23 pages2020 113 Taxmann Com 36 SAT Mumbai 10 10 2019Sejal LahotiNo ratings yet